Ashton Invests@Ashton_1nvests

I wouldn’t be surprised at all if healthcare ends up leading in 2026.

While everyone has been focused on AI and mega-cap tech, healthcare has quietly been resetting. Valuations have compressed. Sentiment is weak. Expectations are low.

That’s usually where leadership starts.

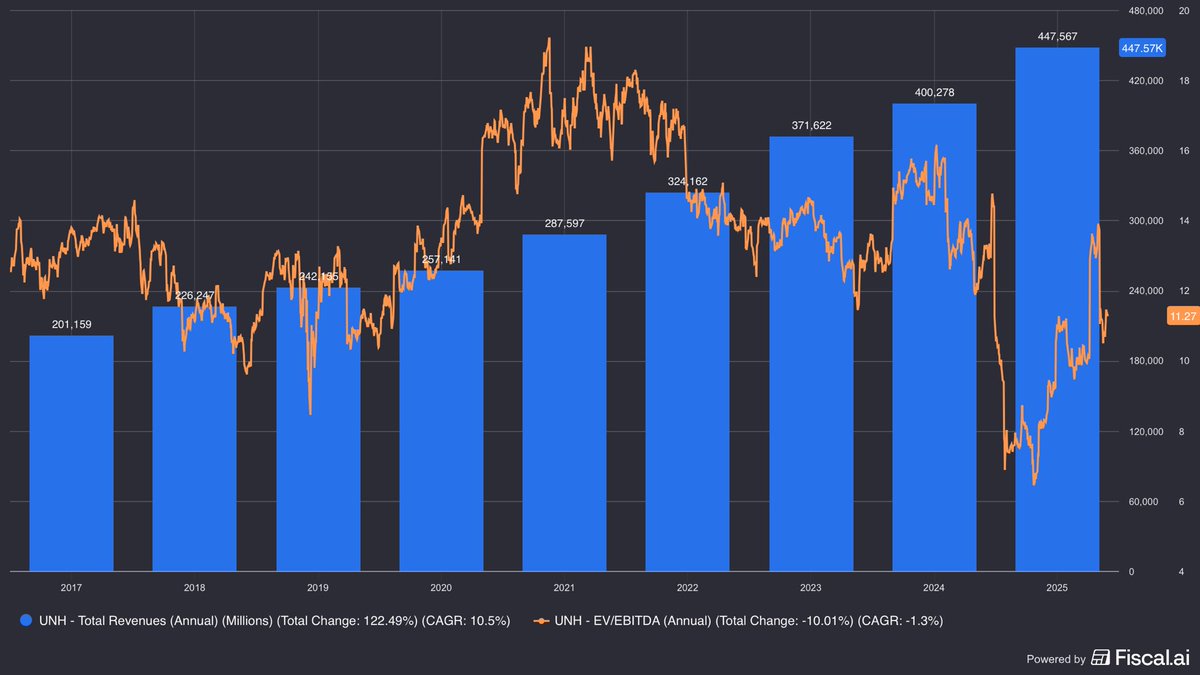

$UNH and $OSCR in particular look interesting to me.

$UNH is a cash-flow machine with scale, data, and diversification across insurance and care delivery. It’s not flashy, but it compounds.

$OSCR is higher beta, but it’s building a tech-driven insurance model in a massive market. If execution continues and margins improve, the upside could surprise people.

Both are positioned well long term.

If capital rotates out of crowded trades and into overlooked sectors, healthcare could have a big year.

Sometimes the best opportunities aren’t the loudest ones.