@BlackPantherCap In addition, thank you very much @BlackPantherCap for you effort and sharing your story behind it. I appreciate when people share their thoughts and be transparent.

Day 170/365.

Me and my daughter made a deal almost a year ago. Post every single day for 365 days. See if we could hit 50,000 followers together.

We’re almost there. Wtf.

195 days left and we’re basically already at the number that was supposed to take the whole year.

I showed her a photo of a stadium with 50,000 people in it yesterday. She just stared at it. Properly blew her mind.

So I’m extending the goal. 75,000.

Let’s see if that’s even possible… honestly, I don’t know. 50,000 felt unlikely too, until it didn’t. This one’s a bigger gap, and I don’t have a plan for it beyond just doing the work and seeing what happens.

If anything I’ve written has ever actually helped you, I want you to know I notice. Not saying that as a line. Every milestone so far happened because someone who didn’t have to share it, did.

If you’ve gotten something out of this, that’s the moment to repost it, or send it to the one person who’d actually use it.

When we hit:

50,000: full deep dive on the 4 positions I’m most bullish on long-term. No holding back.

75,000: I genuinely don’t know yet. This wasn’t part of the plan. So tell me. What would actually help you? Stock strategy, portfolio construction, position sizing… name it. Enough people want the same thing, that’s what gets built.

Comment below. I’m reading all of them.

A heartfelt, thank you.

-BP

$IREN $NBIS $CIFR $PL $RKLB $ASTS $ONDS $PNG.V $AAOI $OUST

@restingpoint@wolfgangkasper VUL is extracting out of thermal water and using it to generate power and heat.

In addition they refine lithium chloride and have their development plant up and running since 04/2024 and the refinery since 01/25. Main plant is up to 24.000 tonne currently under construction.

@Wingtrade101@wolfgangkasper I am unsure what vul does, but $lib.v is extracting lithium today out of 28 ppm brines in the Permian Basin. They've delivered 1 tonne and have produced a lot more, with their first 1000 tonne facility in production by year end.

Just started a core position in one of the most potentially lucrative, unknown, lithium carbonate extraction startups. I now only hold 3 stocks!

$LIB / $VLTLF — LibertyStream

What it is: a ~US$200M micro-cap producing lithium carbonate from Permian oilfield brine in Texas. Instead of mining or evaporation ponds, it uses proprietary ion-exchange Direct Lithium Extraction (DLE) on the salty ‘produced water’ that oil & gas operators already pull up and have to dispose of. No competition in this aspect.

How it operates: asset-light. Rather than owning wells or building greenfield plants, it bolts modular extraction + on-site refining units onto a partner’s existing water infrastructure. Namely, Select Water Solutions (NYSE: WTTR), under a definitive build-out agreement. Select handles pretreatment and site logistics; LibertyStream brings the tech and takes the lithium. That cuts capex, permitting burden, and time-to-production. This enables greater profitability.

How it makes money: it sells lithium carbonate (technical + battery grade) under purchase orders and, going forward, multi-year offtake agreements. Select takes a per-tonne royalty. FIRST U.S. purchase order landed in 2026; a 600 tpa offtake term sheet (from a 1,000 tpa facility) is the first contracted demand. Not to mention the applications for multiple government grants and $LIB has a strong case for many.. We can see up to 3-4 facilities by end of 2027.

The model’s edge and the projection: ‘prove one modular unit, then copy-paste it.’ Facility 1 (~1,000 tpa) targets year-end 2026 commissioning. From there the plan is to replicate across Select’s Midland Basin sites and eventually the Bakken. Company-cited opex is ~$6,200/t (incl. royalties) against ~$25k/t lithium - but note that’s an anticipated figure at first-site scale, not yet proven commercially. Opex can come down significantly over time.

The trend it’s riding: the U.S. is heavily import-dependent for refined lithium (China dominates processing), demand is growing with EVs + grid storage, and Washington is pushing hard on domestic critical minerals. A Texas-incorporated, U.S.-producing lithium company sits right in that lane. Look at US demand/supply curve for lithium.

Growth catalysts to watch: definitive offtake signing, Facility 1 commissioning, a targeted NASDAQ uplisting (late ’26/early ’27), and Bakken expansion via state-grant funding. Huge growth is coming IMO.

The honest risks: it’s pre-commercial, costs at scale are unproven, dilution is POTENTIALLY (CEO seems to be looking for a non-dilutive path from yesterdays presentation) coming, the inventor-CTO and co-founder both departed in 2025 (raising IP questions), and there’s active promotion around the name. High risk, high reward.

Under-covered, genuinely interesting. DYOR. Not financial advice.

For those who know about this stock feel free to comment anything I may have missed (alot). 😂

-🐺

libertystream.com/investors

@mkfilko From your statement I read, that nevertheless you are invested in some of them. But I assume something less than 1% of your portfolio for each of them, right?

SPAC Opinions ($BCAR, $ATII, $SPKL, $IPFX)

Many of you have suggested SPACs to me over the past few weeks and I have taken some time to look into them. Here is my opinion on $BCAR, $ATII, $SPKL and $IPFX.

> $BCAR is taking Exascale Labs public, a GPU cloud / NeoCloud play. Same business as $BRUN (and $WLAC), just much earlier. Merging at ~$500M equity value on $7M FY2025 revenue and ~16% gross margin. The “$300M+ pipeline” is qualified opportunities, not signed backlog like BRUN’s $1.45B. So the whole thesis is execution. If they convert that pipeline and scale, I would not be surprised if they emerge a winner. Most bullish on this one. S4 has already been filed and the numbers look pretty decent.

> $ATII is Forge Nano, atomic layer deposition for chips and batteries. I like the company. But the deal values them near $1.3B EV on $14.5M FY2025 revenue. That number only works if Phase 2 ($460M to $1B+ revenue) lands. Their own deck cannot guarantee Phase 2 timelines or execution, and that is what the valuation leans on. Too rich for my taste until they prove the ramp. I will be watching this closely from the sidelines.

> $SPKL is taking ZincFive public, nickel zinc batteries for data center power. ~$752M EV on $66.9M 2025 revenue (doubled YoY) and an $81M backlog. Tech is promising. But per their deck they are still gross margin negative, which reminds me a lot of $EOSE. Still too early for me.

> $IPFX is taking Quantum Space public, maneuverable spacecraft for defense, run by ex NASA chief Jim Bridenstine. $1.2B valuation. The catch: Ranger has not flown yet, first launch slipped to mid 2027, and 2026 cash burn is ~$69M. They are reaching for $LUNR style numbers while the product is still on the ground. Also very early for me.

I don’t have large positions in any of these. Just my 2c. Let me know your thoughts in the comments!

- Leki the investing monkey 🙊

It is very clear what gets rewarded on X.

Attach a ticker and everyone pays attention.

No ticker, no obvious trade, no immediate money to follow, and the room gets quieter.

That is the junk food vs healthy food problem.

Stock picks are easy to consume.

Frameworks are harder.

But frameworks are what actually compound.

The ticker may make you money once.

The right way of thinking can make you money for the rest of your life.

There’s a “teach a man to fish” lesson in here somewhere.

Unfortunately, fish get more impressions than fishing lessons.

Properly analyzing a company takes hours.

I do it for free.

But I'm only interested in ones with 5x potential.

→ Like this post if you want me to analyze one

→ Drop your ticker in the comments

Starting with the most requested.

Which one do you think could 5x?

$VELO has run hard into the SpaceX IPO.

Day 1 of the SpaceX series - $SATS tomorrow.

SpaceX holds an $8M IP licence on Velo3D's tech ($5M licence + $3M support), and Velo3D's printers have made Raptor engine parts.

Q1'26 gross margin inflected to +17.2%, from −73.6% the quarter before. Revenue +48% YoY. Debt cut ~70%. The operational story is improving independently of SpaceX.

Some concerns include $18M operating cash burn in Q1, going-concern flag intact, and a stock priced for a SpaceX windfall that the filings don't yet size. The $50M April raise bought runway, but isn't buying certainty.

So the question isn't "is VELO a SpaceX supplier" - it is one. It's whether the turnaround can be continued in a tough financial environment.

6.6k words in probably the most comprehensive breakdown of the company on X. Read below.

$VELO $SPCX

UBS global research just put numbers on AI data center power semis.

Here's a list of tickers they named specifically

> Leaders: Infineon $IFX (Buy), $TXN

> Incumbents: Renesas 6723.T, $ADI

> Power stages / VRM: Monolithic $MPWR, Vicor $VICR

> Wide band gap on the 800V shift: $NVTS, $STM, ROHM 6963.T, $ON

> Smaller / laggard exposure: $POWI , $DIOD, $AOSL

> PSU system level: Delta 2308.TW, Lite-On 2301.TW

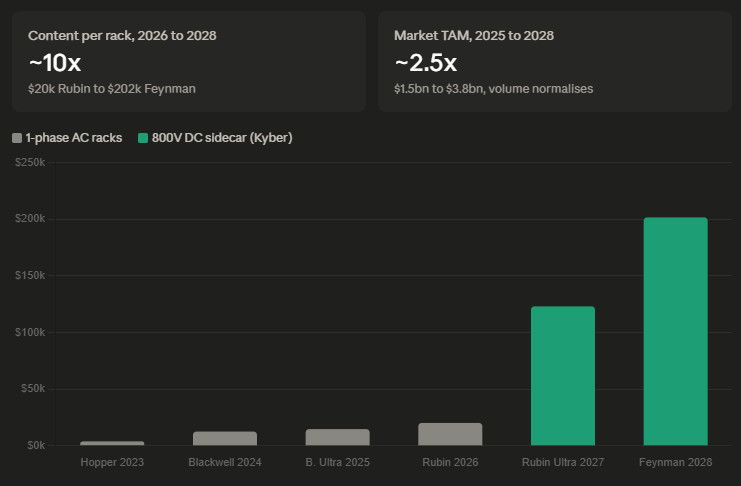

Content per rack is exploding:

Hopper 23': $3.9k

Blackwell 24': $12.6k

Rubin 26': $20.2k

Rubin Ultra 27': $123k

Feynman 28': $202k

50x (FIFTY) in 5 years. Driver is the 800V DC shift forcing GaN/SiC across the stack, not unit volume.

But UBS's own model implies 30GW+ of 2026 capacity adds vs 10-15GW consensus.

Infineon's guide alone implies 40GW+. That is double.

They predict the TAM $1.5BN 25' will jump to $3.8BN by 28'

So chat, are there any power-semi plays not listed that you recommend I take a look at?

The goal should be to find the next $NBIS, $ONDS, $ASTS, $RKLB, $SIVE, $AAOI, $AXTI and whatever went up more than 1,000% in 12-24 months.

What are your next big bets?

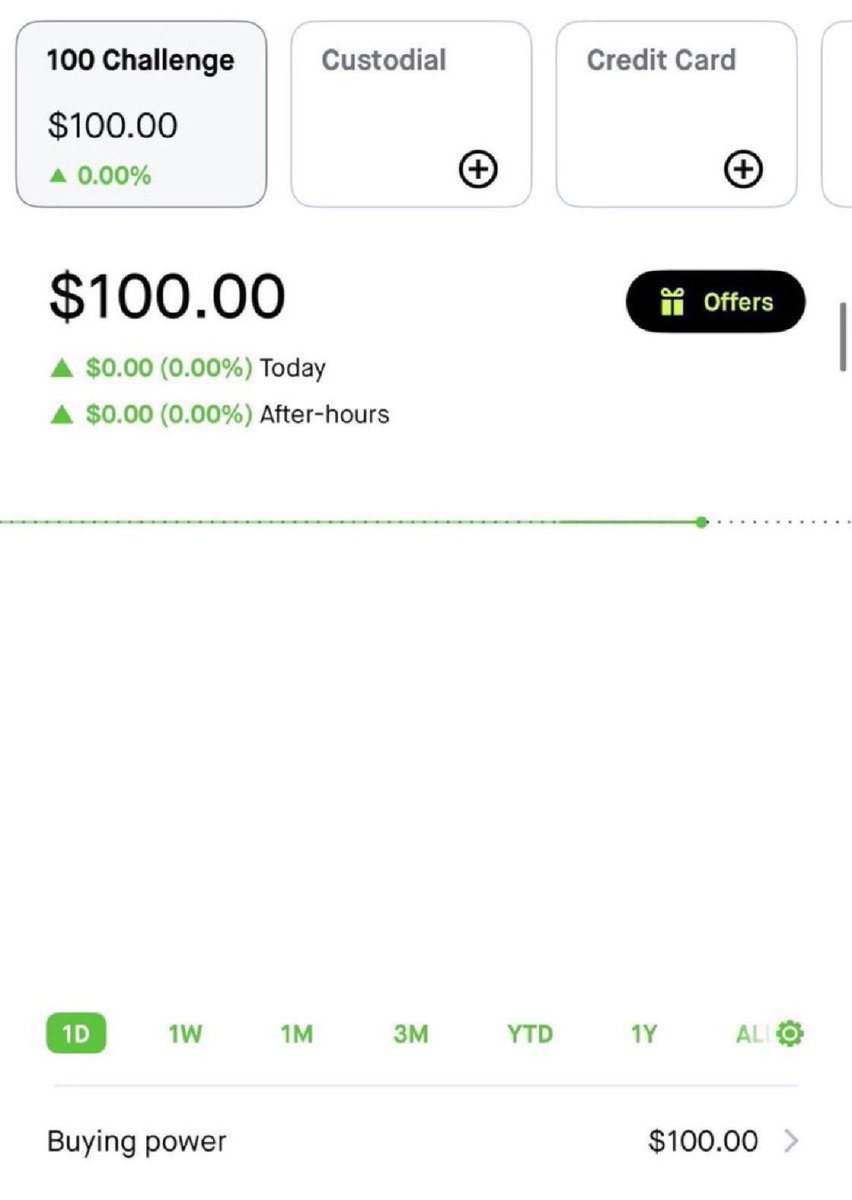

Due to ultra high demand

I’m restarting the $100 to $10,000 challenge.

I want everyone to have a fair shot at this.

Last time it took me about 5 days, will try to do it faster this time.

If you want to follow along, comment below to join

Going to lock comments in 24 hours