@FinnStockinger I share my real-time alert (entry & exit points) on WhatsApp, free to join ✅

➡️Copy search input Reply “2026” to WhatsApp: 17026042303

Here’s the link :wa.me/17026042303/?t…

English

Fiun StcoKlnger

53 posts

$RMBS: The Silent Architect of the AI Orchestration Layer I feel like $RMBS is still flying under the radar. Aside from @damnang2 , I’ve seen very few people covering it, yet the stock has quietly ripped +50% over the last month. Yesterday’s $INTC results acted as a massive wake-up call. The market is finally realizing that the AI race isn't just about raw GPU power, it’s about the CPU and the Interconnect orchestration that keeps the entire system from bottlenecking. Rambus is the essential player you need to watch. Here is why: 1⃣The CPU Comeback As server architectures evolve, the burden is shifting back to the CPU for complex data management. Rambus provides the critical RCD (Registering Clock Driver) chips that allow these CPUs to talk to memory without signal degradation. No Rambus = No high-speed CPU performance. 2⃣Mastering Data Orchestration AI is a logistical nightmare. Rambus’s CXL technology is the "conductor" of the data orchestra. It enables memory pooling, allowing data to flow seamlessly between processors and RAM. They aren't just moving bits; they are orchestrating the entire flow of the modern data center. 3⃣ The "Infrastructure Tax" With 80% gross margins and a massive IP portfolio, RMBS has evolved from a patent play into a silicon powerhouse. Every time a provider scales their CPU capacity or memory density, Rambus collects their royalty. It's a direct tax on data volume. 4⃣Financial Fortress Zero debt and a massive cash pile. In a market seeking safety without sacrificing AI exposure, RMBS offers a rare combo of explosive growth and a rock-solid balance sheet. ⬇️The Reality Check: We are seeing a massive +10% spike in pre-market as I write this. The market is clearly front-running the Q1 earnings (due Monday, April 27). While a 50% monthly run usually screams "overbought," the current price action suggests we are witnessing a fundamental re-rating. Investors are no longer valuing $RMBS as a legacy patent firm, but as an AI infrastructure essential. With $INTC results highlighting the shift toward CPU-led orchestration, the "overhead" might just be the new floor. The Verdict: If the CPU is the brain, Rambus is the nervous system. The "Interconnect" era is officially here. Are you chasing the breakout, or waiting for a retest of support? Let’s discuss. 👇

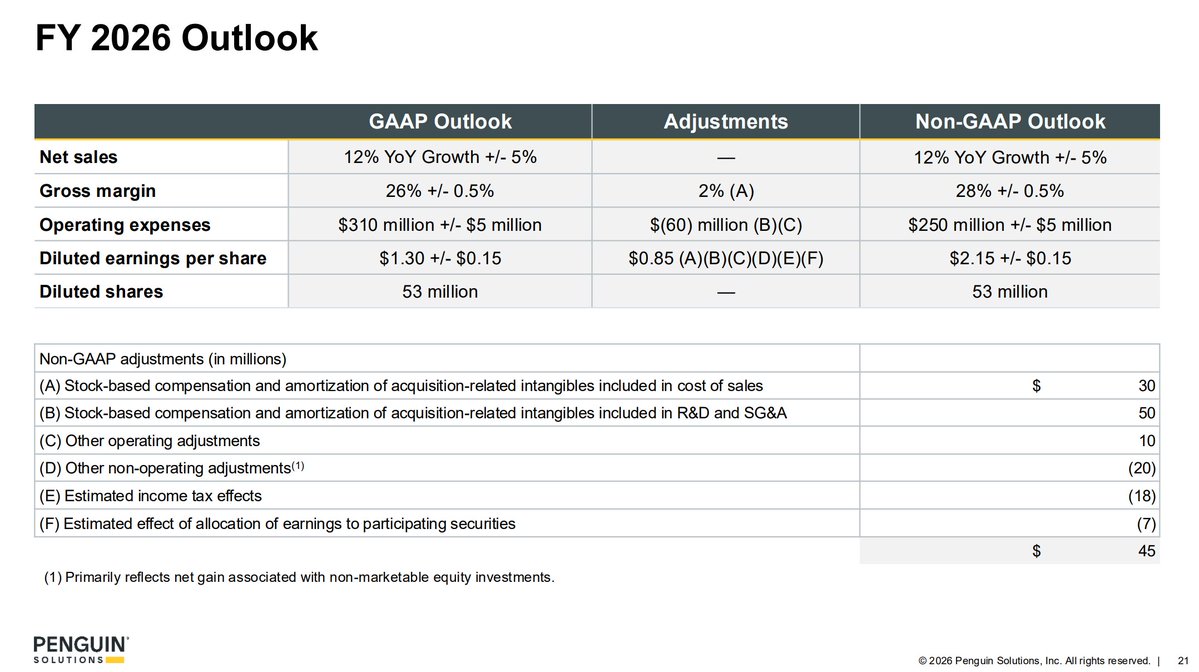

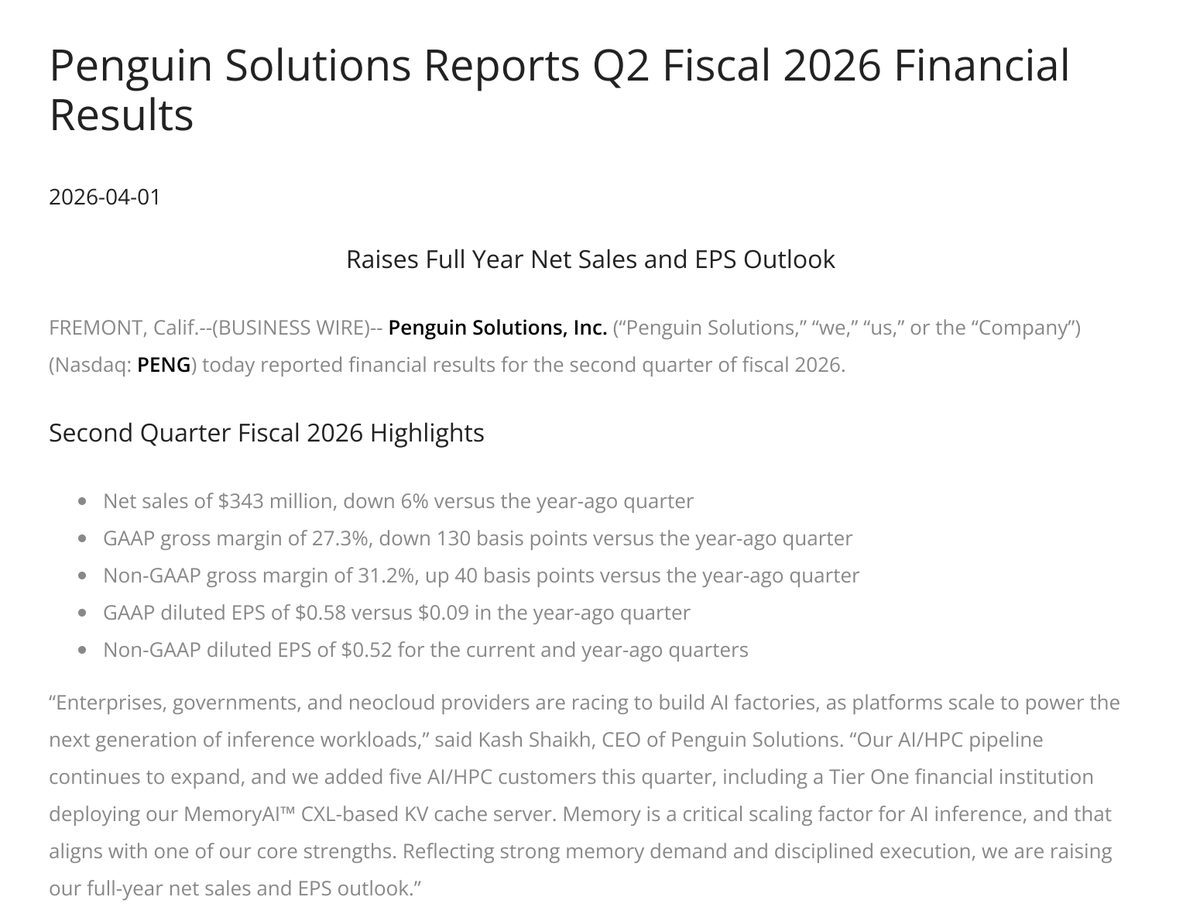

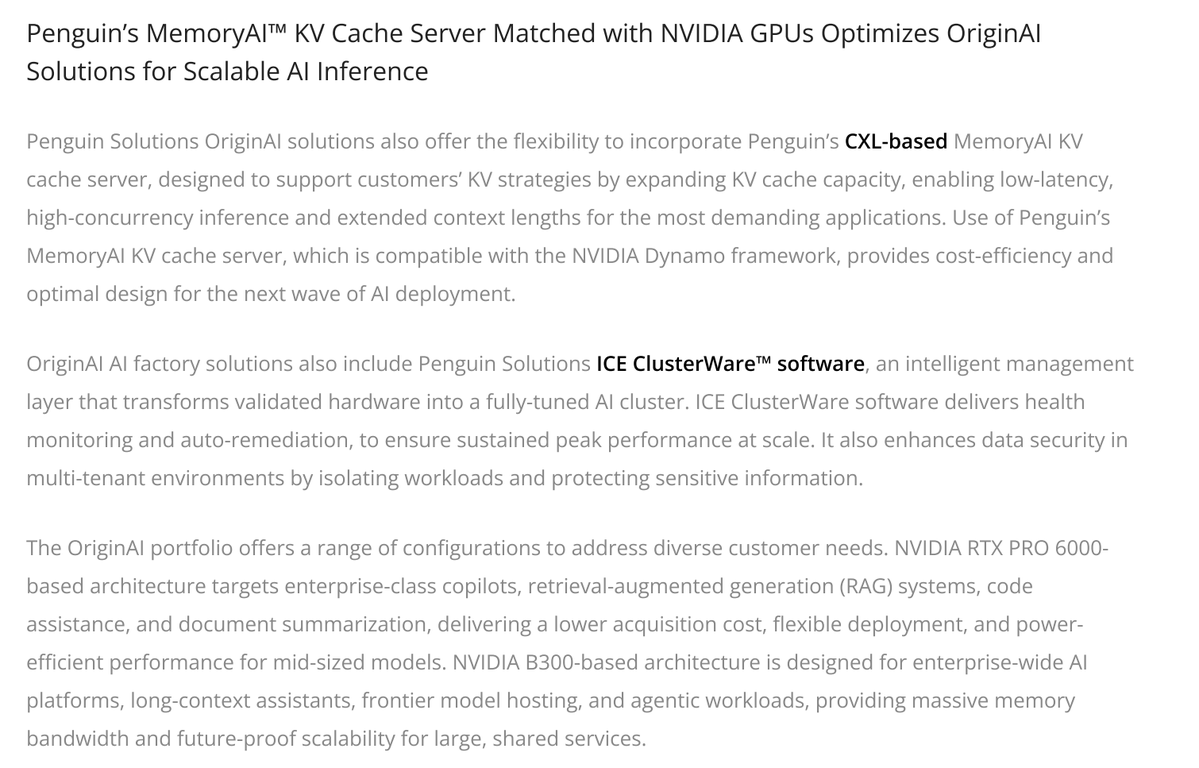

5 Under-the-Radar Rockets Poised to Ride the AI "Memory Wall" The market is obsessed with "Compute," but it’s ignoring the fact that the smartest AI on Earth is currently starving to death. While everyone is chasing the same crowded trades, I’ve identified 5 "under-the-radar" rockets that are solving the ultimate bottleneck. Here is why the "Memory Wall" is where the real Alpha is hiding in March 2026. We need to realize that the current Von Neumann architecture is surrendering to LLMs. If the processor is a Formula 1 engine, memory is currently the tiny straw we’re trying to refuel it through while driving at 300 km/h. Here are 3 deep-dives shaping the market right now: 1️⃣ Data Locality is the New Currency: In AI model training, 90% of energy is wasted just... moving data between chips. Not on the actual computation. This is why any company shortening the physical distance between the byte and the transistor (HBM, CXL, Chiplets) basically has a license to print money. 2️⃣ HBM Cannibalization is Real: According to the latest Q1 2026 reports, DRAM and NAND spot prices have surged by 80-90%. Producing one HBM4 die consumes 3x more wafer capacity than standard DDR5. The result? Giants like Samsung and Hynix are "abandoning" the PC and Auto markets. Whoever has physical inventory on the shelf now dictates the margin. 3️⃣ CXL 3.0 as a Game Changer: Instead of buying ultra-expensive RAM for every individual server, we are entering the era of Memory Pooling. This allows servers to "borrow" memory dynamically. The companies controlling this protocol are the new Gatekeepers of the data center. Where to find Alpha when the market is already "heated"? Here are the 5 tickers I’ve shortlisted for deep analysis: 👇 1️⃣ $CRSR (Corsair Gaming) – Inventory Arbitrage A classic play on supply-side "short squeeze." Corsair entered 2026 with a massive stockpile of DRAM contracted at 2025 prices. With current spot prices up nearly 90%, their margins on DDR5 modules are pure arbitrage. Their recent $50M buyback and record Q4 margins (up to 35% in components) suggest management sees the windfall coming. 2️⃣ $PENG (Penguin Solutions) – The CXL Architects A pivotal player in breaking the "Memory Wall." At GTC last week (March 2026), they unveiled MemoryAI™ an 11TB CXL-based KV Cache server. They are solving the bottleneck at the systems level, not just the component level. Still trading at an attractive forward P/E (~10-12x) despite near 100% EPS growth projections. 3️⃣ $NLST (Netlist) – The Legal Bottleneck DDR5 and HBM cannot scale without LRDIMM technology, which Netlist patented years ago. On Feb 23, 2026, the CAFC (Appeals Court) upheld their key '314 patent against Micron for the third time. With a massive trial against Samsung scheduled for April, we are approaching a "Binary Event" that could trigger billion-dollar licensing settlements. 4️⃣ $RMBS (Rambus) – IP Monopoly They don't build fabs; they design the data superhighways. They just announced the industry-first HBM4E controllers (4.1 TB/s!). With 80%+ gross margins, Rambus profits from every increase in transfer speed without risking a single dollar on physical manufacturing or inventory. 5️⃣ $SANM (Sanmina / Viking Tech) – Edge AI Defense Owner of the Viking Technology brand. Their new Viking Edge series is exactly what the industry needs: ultra-dense, custom memory produced locally in the US. In an era of deglobalization and Asian supply chain fragility, their "Made in USA" specialty memory is a massive strategic moat. Bottom Line: The memory wall isn't a one-quarter blip - it’s a structural shift that is only beginning to be priced in. I wanted to ask - what are your thoughts on these? Perhaps some of you are deeper into these names and can save me a few hours of due diligence?

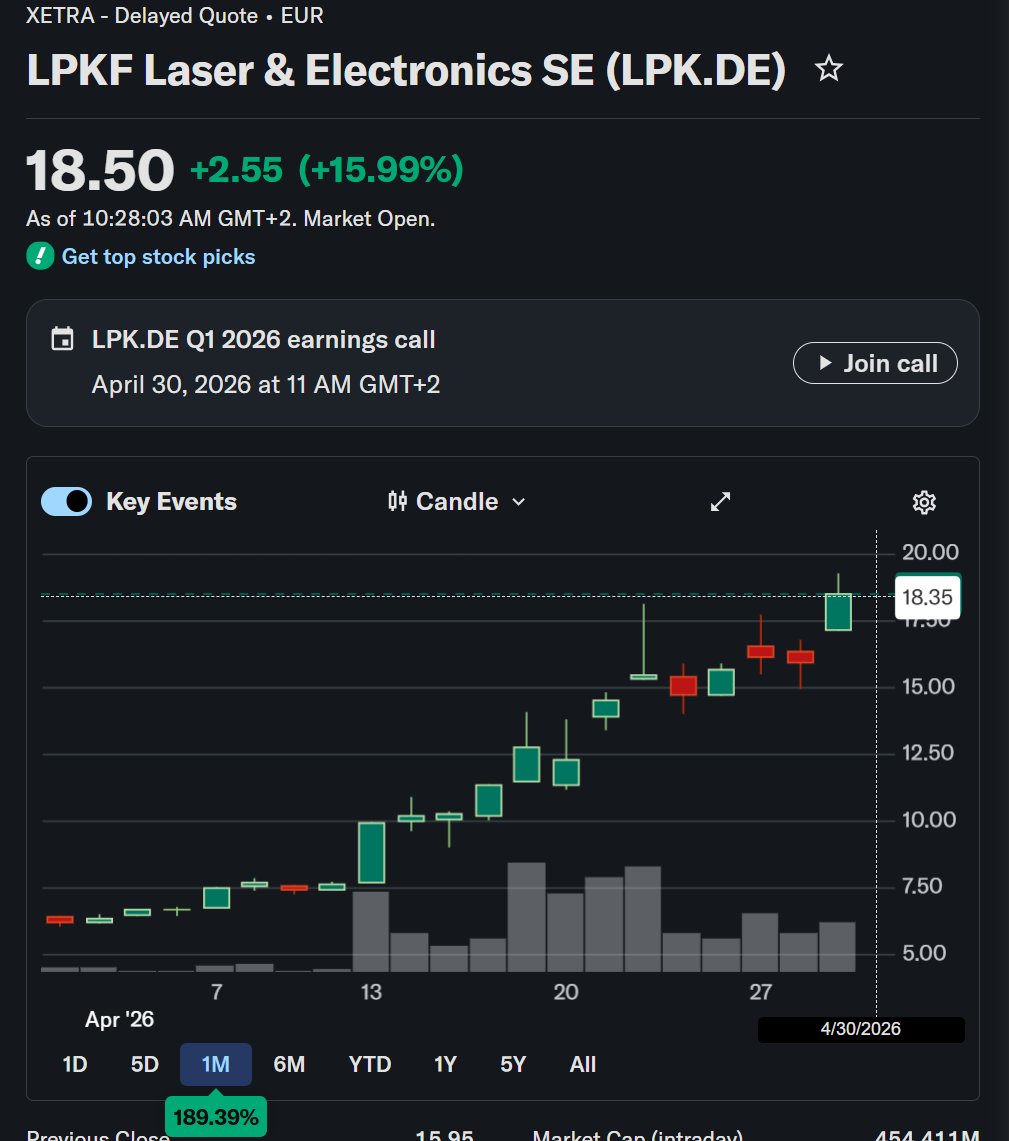

$LPKF: Beyond the Hype – How I Spot the Next Bottleneck I’ve already written plenty about $LPKF as a company, but today I want to share the "how" rather than the "what." How did I find a stock that ran from €7 to over €17 in just 1.5 months (+150%)? 1⃣The Methodology: Solving for the Bottleneck While the masses were focused on Indium Phosphide (InP) shortages, I was already asking: "What comes next?" * The InP Bottleneck: Led me to $IQE (~600%) and $AIXA (100%). The Laser Alternative: Led me to $SIVE (+800%). But I kept digging. As we move toward 1.6T standards, the semiconductor supply chain is hitting a wall. I believe Glass Substrates are the next revolution. 2⃣Why $LPKF? Glass substrates solve massive thermal and signaling issues, but they have one fatal flaw: cracking during production. This is where TGV (Through Glass Via) comes in. $LPKF’s LIDE (Laser Induced Deep Etching) technology is currently the only proven method to handle this process at scale without compromising the glass. It is the definition of a technical bottleneck. 3⃣Realistic Timelines vs. Market Madness Let’s be real: full High-Volume Manufacturing (HVM) for glass substrates likely won’t hit until 2028, with major machine orders starting in 2027. (I hope so). The current price action is absolute madness - I didn't expect a 150% move this quickly. However, I’m not going to stand on the sidelines when the thesis starts playing out. 4⃣Conviction and Concentration As @MarkosAAIG noted yesterday: "Not every bottleneck or constraint is investable. You really need to understand that." I don't buy every company I mention. I prefer a concentrated portfolio. I started a small position in $LPKF at €7, and because I had done my homework, I was ready to add at €8.50 and €10 as the momentum confirmed my thesis. I didn’t have to "check" what the company did when it started moving - I was already prepared. 5⃣The Strategy Moving Forward Two months ago, I didn't think $LPKF was a "put your entire life savings on it" play. It was a calculated bet on a specific technical constraint. My advice? Always ask yourself: Why am I investing in this specific company? How long can I realistically afford to hold this?