ทวีตที่ปักหมุด

📘 PayProtocol White Paper V10 (Rebranded)

We are thrilled to release our latest White Paper V10 (Rebranded), presenting the next stage of the blockchain-based payment infrastructure.

This updated white paper outlines our vision for structural innovation across the ecosystem —

emphasizing PayChain, Stablecoin Infrastructure, P2F (Pay-to-Finance), and the $PCI Token Economy as the core pillars.

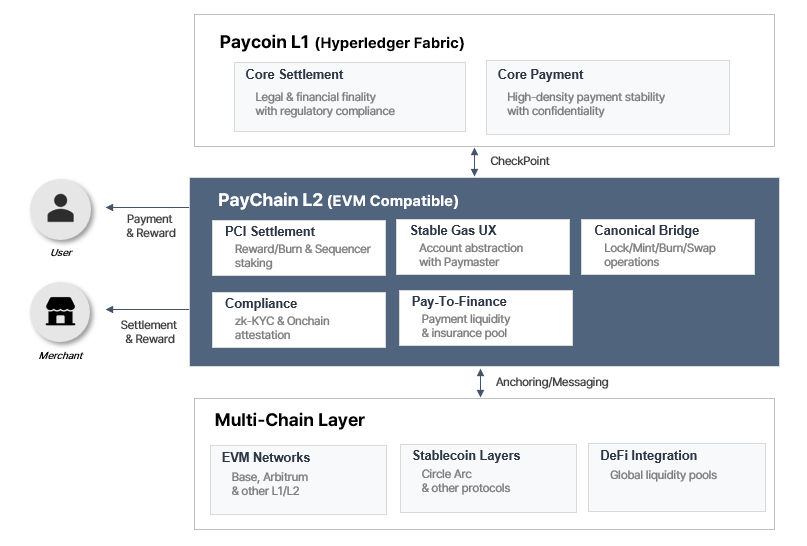

🌐 PayChain, Expanding the Global Payment System

PayChain is a purpose-built chain designed to fundamentally expand payment and settlement infrastructure. It introduces a two-layer structure that bridges traditional systems with a blockchain-based global network.

- Paycoin L1: Hyperledger-based mainnet providing legal finality and regulatory compliance

- PayChain L2: EVM-based extension layer enabling global settlement, liquidity management, and stablecoin operations

PayChain serves as a dedicated blockchain for payments, providing convenience to both users and merchants while supporting regulation-friendly Web3 transactions.

Key Features

- Gas Abstraction: Allows users to execute transactions without holding a native token (e.g., ETH).

Transactions are automatically sponsored through an Account Abstraction-based Paymaster, enabling a simplified, gas-agnostic user experience.

- Performance & Finality: Delivers instant soft finality for user transactions, with financial and legal finality guaranteed through periodic L1 checkpoints.

- Governance: Core parameters such as gas fees, incentives, and burn ratios are managed via on-chain governance, with delegation mechanisms expanding community participation.

- Interoperability: PayChain supports a multi-chain environment via Cross-chain Messaging, ensuring seamless connectivity with external networks.

We aim to establish a secure and open global blockchain payment infrastructure through the combined operation of PayChain and the Paycoin mainnet.

💵 Stablecoin Platform, A Trusted Hub for Global Settlement

Built atop PayChain, the PayProtocol Stablecoin Platform serves as a global hub for fiat-backed stablecoin settlement. It connects multiple stablecoin systems and ensures transparent, compliant transaction flows.

Core Components:

- Cross-chain Messaging & Anchoring: Synchronizes mint/burn/settlement events across chains to prevent duplication.

- Multi-chain Oracle: Verifies exchange rates, circulation, and data consistency across multiple networks.

- Gas Sponsorship: Enables designated sponsors to cover transaction fees on behalf of users, providing an optimal UX.

- Compliance Framework: Enforces on-chain KYC-based transaction control for regulatory alignment.

Through this architecture, we aim to enable a stablecoin-based, real-world payment ecosystem that bridges traditional finance and Web3.

💰 P2F (Pay-to-Finance) — Combining Payments and Financial Activity

P2F is PayProtocol’s newly designed Web3-native payment model, merging DeFi mechanisms with traditional payment flows. It enhances the value of payments by transforming every transaction into a yield-generating financial action.

Process Overview:

- Payment & Deposit: User payment assets are automatically deposited into a liquidity pool.

- Liquidity Utilization: Funds remain in the pool and generate interest until settlement.

- Settlement Request: Merchants can request settlement at any chosen time, with rewards varying by liquidity pool status and duration.

- Reward Distribution: Yield generated within the pool is distributed among users, merchants, and the protocol.

P2F seamlessly integrates with existing PayProtocol payment infrastructure. Merchants can adopt P2F without additional onboarding complexity, while users maintain the same familiar payment experience.

🔥 PCI Burn & Circulation Model — Building a Sustainable Value Cycle

The latest white paper introduces a new burn and distribution model for the $PCI token, aimed at ensuring sustainable value creation within the ecosystem.

1. PCI Burn Model

A portion of transaction fees from payments and transfers will be burned, ensuring that network activity directly contributes to the asset’s long-term value.

- 50% of payment transaction fees are burned

- 50% of transfer transaction fees are burned

2. PCI Circulation & Lockup Model

The $PCI token’s distribution model has been restructured to establish a transparent and predictable operating framework.

- Foundation Holdings: 844 million $PCI locked (100%)

- Scheduled Unlock: 28.8 million $PCI (3.4% of holdings) to be unlocked over two years

All $PCI lockup and release schedules are transparently executed on Arbitrum, with real-time data available on the official PayProtocol website.

Read PayProtocol White Paper V10 (Rebranded)

👉 payprotocol.io/white-paper

English