ทวีตที่ปักหมุด

rftd

16.7K posts

rftd

@rftd09

|| DC: rftd || Artist || supportive @ethos_network @rialoHQ

เข้าร่วม Aralık 2021

3K กำลังติดตาม3.2K ผู้ติดตาม

Web3'te "spam" devri bitti, "emek" devri başladı. Rialo Türkiye ekosisteminde kimin gerçekten "Araştırmacı" olduğunu görme vakti.

1-30 Nisan boyunca X'i kaliteli içeriklerle domine ediyoruz. Kriterimiz basit: Sayı değil, ETKİ.

🔹 Özgünlük

🔹 Kalite

🔹 Stratejik Derinlik

Sadece timeline dolduranlar değil, Rialo’nun teknik gücünü (REX, RWA, Async) en iyi anlatanlar ayrışacak.

Rialo Türkiye ailesine girmek için en iyi avantajlardan biri daha .

Rialo büyük hesaplari değil, topluluğu değer veren gerçek topluluk üyelerini istiyor ❤🔥

Türkçe

Hello @RialoHQ community!

This week showed strong engagement across global and regional channels. Based on contributions, onboarding support, meaningful conversations and consistency these members stood out.

Thanks for your amazing efforts! Keep it up,you could be next on wall

English

Rialoda haftanın lideri olmak inanılmaz hissettiriyor ve bunu abilerim ve ablalarım olmadan asla yapamazdım herkese çok teşekkür ederim şimdi rialo için daha çok çalışma vakti grialo

Türkçe

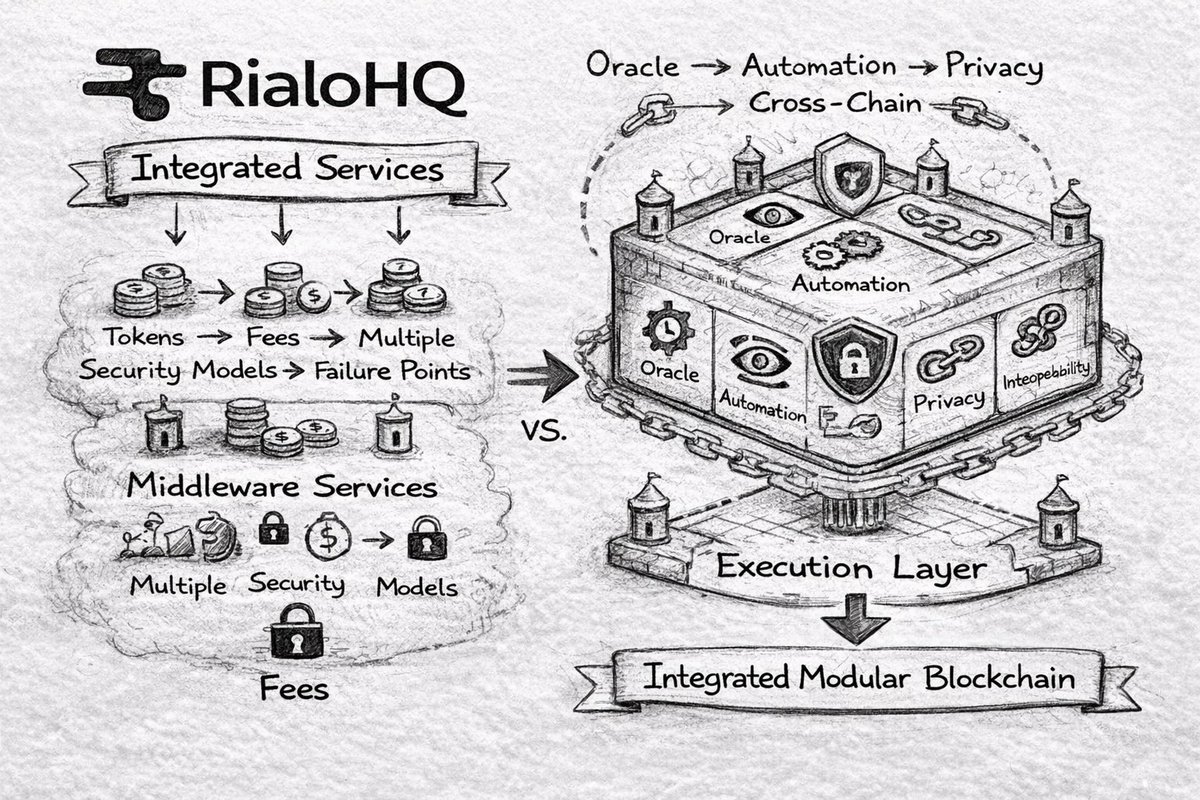

DeFi’de bir uygulama geliştiriyorsun diyelim.

Oracle lazım, Chainlink entegre ediyorsun. Otomasyon lazım, Gelato ya da Chainlink Automation ekleyorsun. Privacy lazım, ayrı bir çözüm. Cross-chain lazım, başka bir köprü. Her katman ayrı ücret, ayrı token, ayrı güven modeli, ayrı başarısızlık noktası.

Buna double marginalization diyorlar. Her middleware kendi payını alıyor, sen de her birini ayrı ayrı entegre etmek, finanse etmek, izlemek zorunda kalıyorsun. Uygulaman büyüdükçe bu yük katlanıyor.

Rialo’nun sorusu şu: bu katmanlar neden chain dışında?

Supermodularity ekonomide şunu anlatır bileşenler birleşince toplam değer, parçaların toplamından büyük olur. Rialo bunu mimari prensip olarak alıyor. Oracle, otomasyon, privacy, interoperability bunları ayrı middleware olarak değil, execution layer’ın içine entegre ediyor.

Pratik fark ne? Liquidation için Chainlink’e ücret ödemiyorsun,@RialoHQ ’nun native oracle’ı var. Scheduled execution için Gelato çalıştırmıyorsun, reactive transactions zaten chain içinde. Her biri ayrı token tutmak zorunda değilsin, Stake-for-Service tüm bu servisleri tek akışla finanse ediyor.

Ama asıl mesele güven modeli. Her dış entegrasyon ayrı bir “bu da çalışıyor olsun” bağımlılığı. Rialo’da tüm bu logic consensus içinde validator ne görürse kullanıcı da onu görür, ayrı bir servis ayakta olsun diye dua etmiyorsun.

Modular blockchain narrative’i son birkaç yıldır hâkim. “Her şeyi ayır, optimize et” dendi. Rialo farklı bir iddia ortaya atıyor: doğru şeyleri entegre edersen hem daha ucuz hem daha güvenilir hem daha güçlü bir sistem çıkar.

Türkçe

Herkese iyi akşamlar @RialoHQ bu paylaşımından çıkarımlarım şu şekilde ;

Rialo’nun son paylaşımlarını incelerken tüketici kredileri konusunda önemli bir dönüşümden bahsettiklerini gördüm.

Uzun yıllardır kredi sistemleri büyük ölçüde FICO Score gibi kredi puanlarına dayanıyordu. Ancak artık bazı platformlar kredi değerlendirmesinde daha farklı verileri de kullanmaya başladı.

Örneğin SoFi ve Cash App gibi uygulamalar eğitim geçmişi, iş durumu, gelir akışı ve kullanıcı davranışları gibi verileri de dikkate alabiliyor.

Anladığım kadarıyla Rialo bu yaklaşımı blockchain altyapısı ile birleştirmeyi hedefliyor.

Yani gerçek dünyadaki veriler ile onchain kredi sistemleri birbirine bağlanacak.

Böylece kredi değerlendirmesi yalnızca kredi puanlarına değil, daha geniş veri setlerine dayanabilecek.

Rialo’nun üzerinde çalıştığı modelin, kredi değerlendirmesinden kredi yönetimine kadar birçok süreci blockchain üzerinde bir araya getiren daha kapsamlı bir kredi altyapısı oluşturmayı amaçladığını düşünüyorum.

@itachee_x @RialoTR @slymnogunc @goodhypeonly0

Rialo@RialoHQ

The $1.7T+ US unsecured consumer credit market is starting to move beyond credit scores alone. For decades, lenders mostly relied on systems like FICO to decide who should get a loan, how much they should get, and at what rate. That is changing: newer lending systems, including those used by @SoFi and @CashApp, use signals ranging from education and employment history to cash flow and platform-specific behavior to make those decisions. The next step is to upgrade the lending stack and move key components onchain. Rialo makes this possible by connecting onchain credit systems to real-world data, providing infrastructure to automate servicing workflows onchain, and enabling seamless tokenization of real-world assets, including private credit and consumer loans. That opens up three opportunities: - Richer credit assessment: Lenders can use alternative signals to determine creditworthiness by tapping into real-world data through Rialo. - Efficient servicing: Lenders can run loan management and repayment workflows on Rialo’s transparent, programmable blockchain rails, reducing overhead and improving transparency. - Loan packaging: Lenders can tokenize loans and bundle them into risk-weighted vintages, or loan pools organized by risk profile, with clearer visibility into risk and performance. The opportunity for lenders is not just to make better loans. It is to use infrastructure that enables them to assess, service, and package loans in a single integrated system. Get Real about credit. Get Rialo.

Türkçe

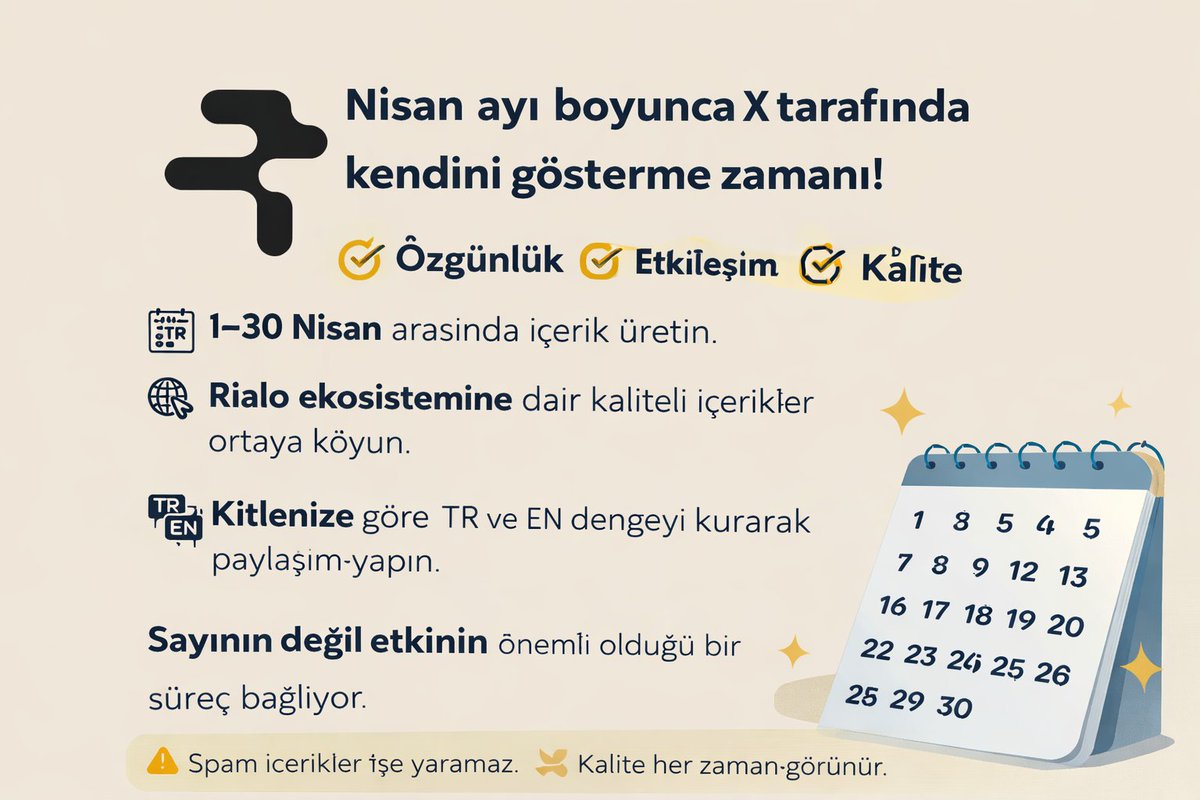

Nisan ayı boyunca X tarafında biraz farklı bir sürece giriyoruz. Amaç basit: gerçekten üreten, emek veren ve fark yaratan insanları net şekilde ortaya çıkarmak.

1–30 Nisan arasında içerik üretimi odakta olacak. Rialo’nun resmi paylaşımları, Builder Hub, Shark Tank ve genel olarak ekosistem üzerine içerikler üretebilirsiniz. Daha önce yapılmış paylaşımlardan referans almak serbest ama kopyalamak değil, üzerine koymak önemli.

Dil konusu tamamen size bağlı. Kitleniz Türk ağırlıklıysa Türkçe ilerleyin, araya İngilizce de serpiştirin. Önemli olan anlaşılmak ve etki bırakmak.

Burada kritik olan şey sayı değil, kalite.

10 tane sıradan içerik yerine 1 tane gerçekten iyi içerik her zaman daha değerlidir.

Değerlendirme 3 şeye bakacak:

👉 Özgünlük

👉 Etkileşim

👉 Kalite

Spam içeriklerin hiçbir karşılığı yok. AI kullanabilirsiniz ama ruhu olmayan, özensiz içerikler sizi geriye götürür. Burada gerçekten emek görmek istiyoruz.

Timeline’ı doldurmak sizi öne çıkarmaz. Ama sürekli iyi işler çıkaranlar zaten kendini belli eder. Çünkü kalite gizlenmez.

Bu süreci sadece bir “etkinlik” gibi değil, kendinizi gösterebileceğiniz bir alan olarak görün. Üreten, katkı sağlayan ve topluluğu ileri taşıyan herkes doğal olarak ayrışacak.

Ben kendi tarafımda başladım. Siz de başlayın.

Bu ay gerçekten kimin bu işin içinde olduğunu göreceğiz.

@RialoHQ @RialoTR @slymnogunc @goodhypeonly0

Special forces $XAGE@Oguzhangezen_

Rialo son dönemde attığı adımlarla aslında neyi hedeflediğini daha net göstermeye başladı. Bu sadece “yeni özellik ekledik” tarzı klasik bir ilerleme değil, daha çok altyapıyı sağlamlaştırarak büyümeyi seçen bir yaklaşım. Öncelikle alfa sürecinin başlaması önemli bir kırılma noktası. Çünkü bu, teoride anlatılan sistemin artık gerçek kullanıcılarla test edilmeye başlandığını gösteriyor. Yani işler kağıt üstünden çıkıp gerçek deneyime dönüşüyor. Web3 entegrasyonu tarafında atılan adımlar da dikkat çekici. Cüzdan bağlantıları, NFT yapısı gibi unsurlar sadece ek özellik değil; platformun Web3 ile gerçekten uyumlu bir ekosistem kurmak istediğinin göstergesi. Bunun yanında yatırım alınması, projenin sadece teknik değil finansal olarak da desteklendiğini gösteriyor. Bu tarz destekler genelde uzun vadeli planların olduğuna işaret eder. Airdrop etkinliği ise topluluğu sürecin içine dahil etme hamlesi. Yani sadece “ürün yapalım” değil, aynı zamanda kullanıcıyı da büyümenin bir parçası haline getirme çabası var. Yeni özelliklerin test edilmesi ve pazarlama tarafının büyütülmesi de bu sürecin devamı gibi. Bir yandan ürün gelişiyor, diğer yandan görünürlük artırılıyor. Kısacası Rialo şu an hype kovalamaktan çok, adım adım sağlam bir yapı kurmaya odaklanmış gibi duruyor. Gürültüden uzak ama istikrarlı bir ilerleme var uzun vadede asıl farkı yaratan da genelde bu oluyor. @RialoTR @RialoHQ @slymnogunc @goodhypeonly0

Türkçe

The $1.7T+ US unsecured consumer credit market is starting to move beyond credit scores alone.

For decades, lenders mostly relied on systems like FICO to decide who should get a loan, how much they should get, and at what rate. That is changing: newer lending systems, including those used by @SoFi and @CashApp, use signals ranging from education and employment history to cash flow and platform-specific behavior to make those decisions.

The next step is to upgrade the lending stack and move key components onchain.

Rialo makes this possible by connecting onchain credit systems to real-world data, providing infrastructure to automate servicing workflows onchain, and enabling seamless tokenization of real-world assets, including private credit and consumer loans.

That opens up three opportunities:

- Richer credit assessment: Lenders can use alternative signals to determine creditworthiness by tapping into real-world data through Rialo.

- Efficient servicing: Lenders can run loan management and repayment workflows on Rialo’s transparent, programmable blockchain rails, reducing overhead and improving transparency.

- Loan packaging: Lenders can tokenize loans and bundle them into risk-weighted vintages, or loan pools organized by risk profile, with clearer visibility into risk and performance.

The opportunity for lenders is not just to make better loans. It is to use infrastructure that enables them to assess, service, and package loans in a single integrated system.

Get Real about credit. Get Rialo.

English

Geleneksel Kredi Sistemi Çöktü. #Rialo On-Chain Kredi Bunu Düzeltiyor...

Normal kredi (geleneksel) nasıl işliyor?

Banka FICO skoruna birde birkaç belgeye bakıyor. Karar insan merkezi sistemle veriliyor. Süreç yavaş, pahalı, bürokrasi bol, şeffaflık sıfır. Geri ödeme takibi, faiz hesabı falan hep aracılarla dönüyor.

"$Rialo on-chain kredi" ise bambaşka:

Gerçek zamanlı ve çok daha zengin veri kullanıyor (eğitim, iş geçmişi, nakit akışı, platform davranışı vs.). Bunların hepsini doğrudan blockchain'e çekiyor. Akıllı kontratlar otomatik olarak kredi onayı, faiz ödeme, temerrüt tespiti, covenant kontrolü yapıyor. Ara katman, bot, manuel iş yok. Her şey şeffaf, hızlı ve kodla garanti altında.

Rialo ne yapmak istiyor?

1.7 trilyon dolarlık teminatsız tüketici kredisi pazarını on-chain'e taşımak. Kredileri tokenleştirip likit hale getirmek, riski daha adil dağıtmak ve geleneksel finansı blockchain'e gerçek anlamda bağlamak. Yani "#GetReal #GetRialo." diyorlar... krediye gerçekçi bak, Rialo’ya geç.

Kısaca: Normal kredi = yavaş + pahalı + kara kutu

#Rialo kredisi = hızlı + ucuz + şeffaf + veri odaklı

Bu iş tutarsa, #DeFi ile gerçek dünya kredisi arasında büyük köprü olur fr fr.

Ne düşünüyorsun? güzel olurmu sence?

@RialoHQ @RialoTR

#Rialo #OnChainCredit #RWA #Web3

Rialo@RialoHQ

The $1.7T+ US unsecured consumer credit market is starting to move beyond credit scores alone. For decades, lenders mostly relied on systems like FICO to decide who should get a loan, how much they should get, and at what rate. That is changing: newer lending systems, including those used by @SoFi and @CashApp, use signals ranging from education and employment history to cash flow and platform-specific behavior to make those decisions. The next step is to upgrade the lending stack and move key components onchain. Rialo makes this possible by connecting onchain credit systems to real-world data, providing infrastructure to automate servicing workflows onchain, and enabling seamless tokenization of real-world assets, including private credit and consumer loans. That opens up three opportunities: - Richer credit assessment: Lenders can use alternative signals to determine creditworthiness by tapping into real-world data through Rialo. - Efficient servicing: Lenders can run loan management and repayment workflows on Rialo’s transparent, programmable blockchain rails, reducing overhead and improving transparency. - Loan packaging: Lenders can tokenize loans and bundle them into risk-weighted vintages, or loan pools organized by risk profile, with clearer visibility into risk and performance. The opportunity for lenders is not just to make better loans. It is to use infrastructure that enables them to assess, service, and package loans in a single integrated system. Get Real about credit. Get Rialo.

Türkçe