@kylewhitegoat @anthonynoto @TRADEsterJJ Does fresh horses mean them switching who they are focusing on for Galileo customers. (Small banks/credit unions to big banks) 🤷♂️ maybe a big whale is on the horizon 💪

English

Future Inspired Mind

45 posts

34 Points HCC vs Santa Fe, 10-13 3FG Stats: 16.4 PPG, 47% FG, 49% 3FG #2 in the Nation 3FG made “103-211”

The performance of our Financial Services and Technology Platform businesses generated strong results, and demonstrate we are not just a lender. Together, these businesses generated $1.2B, +54% YoY, accounting for 47% of net revenue. Both businesses set records, and we see significant growth opportunity.

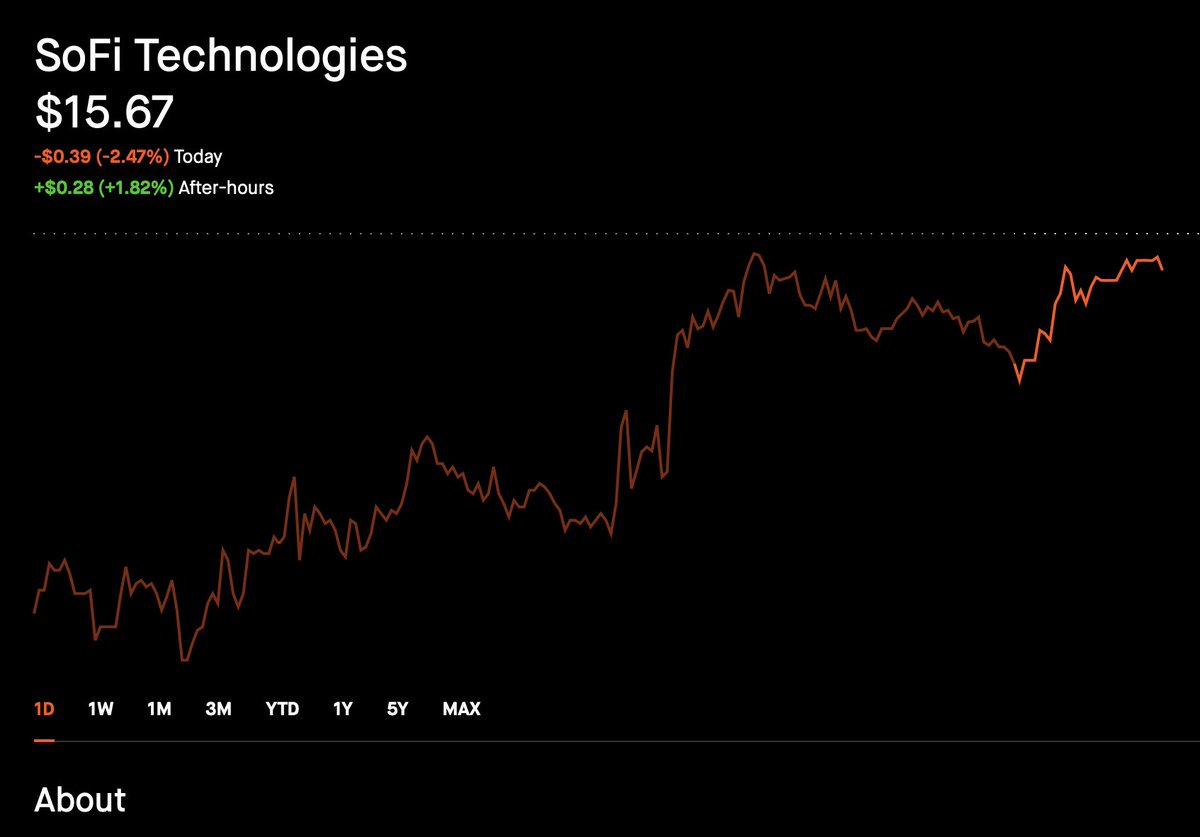

$SOFI WE ARE LIVING IN CLOWN WORLD TRUST ME Current Market Cap SOFI 16.6 Billion AFFIRM 21.7 Billion (Net income Q3) SOFI +61 Million AFFIRM -100 Million