uncoveredalpha@uncovered_alpha

I’ve had a few requests for prompts I use and have found success with, so here’s one I like for stress‑testing a single assumption in a 3‑statement model.

The basic idea: upload your own model (I like Perplexity Computer for this task and I pre-select the GPT-5.4 model -seems the best for excel based tasks), then tell the assistant which assumption you want to attack — for example, Chipotle same‑store sales growth — and have it (1) benchmark that assumption versus history and category data, and (2) role‑play a skeptical PM to surface second‑order questions. You either come out with conviction that’s been stress‑tested, or a list of the 3–4 things you actually need to diligence.

Example prompt: stress‑testing a same‑store sales assumption

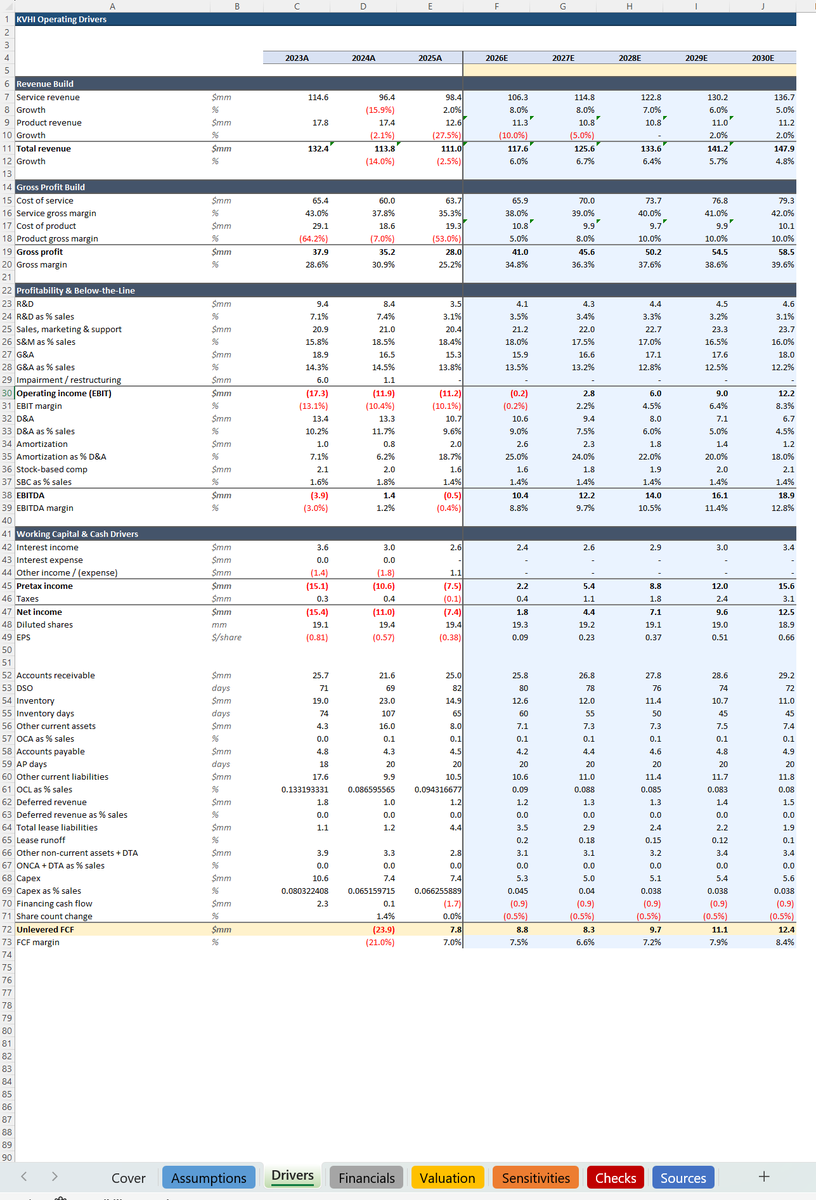

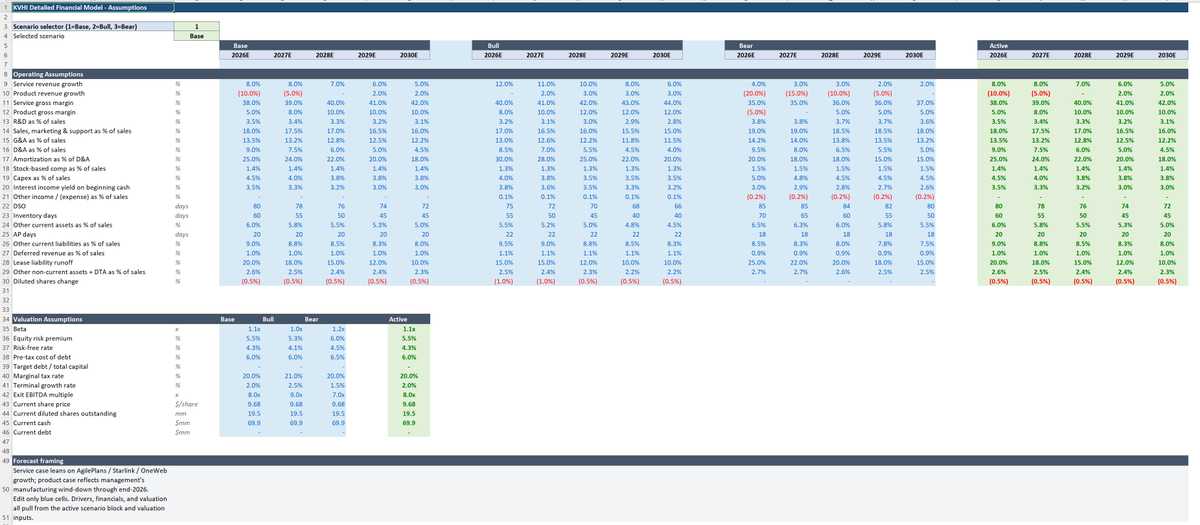

I’m going to upload my own 3‑statement model for Chipotle (CMG) that includes an explicit same‑store sales (SSS) assumption by year.

Your job is to attack one assumption in that model: my base‑case U.S. same‑store sales growth for the next 5 years.

Step 1 – Read and restate my assumption

Ingest the uploaded model and identify the line item(s) that represent same‑store sales or comparable restaurant sales growth by year.

Restate back to me, in plain English, what SSS path I am underwriting (e.g., “you are assuming ~7% SSS in year 1, then 5–6% annually through year 5”).

Flag any inconsistencies between the SSS assumption and other model drivers (traffic vs. price mix, margin progression, unit growth).

Step 2 – Historical and industry context check

Using public data from SEC EDGAR or company-specific press releases, summarize Chipotle’s historical SSS and traffic/price mix over the last 10–15 years, highlighting periods of high growth, normalization, and drawdowns

Compare my forward SSS assumptions to:

Chipotle’s own historical SSS distribution and volatility.

Recent SSS trends for major QSR/fast‑casual peers (McDonald’s, Taco Bell, Starbucks, Cava, etc.), noting whether the category is in broad acceleration, normalization, or deceleration.

Tell me explicitly: relative to that backdrop, is my SSS path aggressive, conservative, or in line with history and peers?

Step 3 – Structured adversarial role‑play I want you to run adversarial dialogues where you role‑play different skeptical PMs who each attack my SSS assumption from a distinct angle.

For each persona:

Run a short dialogue (5–10 exchanges) between that persona and me (as the analyst) focused only on whether my Chipotle SSS assumption is reasonable.

Each persona should ask pointed, practical questions that a real operator or PM would ask, and surface second‑order issues rather than generic “what if growth slows?” prompts.

Step 4 – Synthesis and decision

From all personas, extract the 5–10 most important challenges to my SSS assumption, grouped into themes (e.g., “category traffic headwinds,” “unit growth cannibalization,” “LTO fatigue,” “labor/throughput ceiling”).

For each theme, tell me: How big a swing factor it is to my SSS (e.g., could it move SSS by ±200 bps?). What specific evidence I should diligence with management or third‑party data (e.g., recent weekly traffic trends, saturation analysis, new‑unit AUV cohorts).

Conclude with a one‑page style summary: “If you keep your current SSS assumption, here is the conviction statement you should be comfortable making.” “If you are not comfortable with that, here are the 3–4 targeted diligence items that would most update the SSS view.”

Important constraints

Do not rewrite or “fix” my entire model; stay focused on SSS and variables directly tied to SSS (traffic, pricing, mix, throughput, unit growth).

Be explicit when you are inferring or generalizing from industry data vs. citing Chipotle‑specific history