@LawnChairCap @InvestingTmr @BobbaPaddop Margins have indeed been slim over the past couple of years. We will have to see to in the next set of results what degree of operating leverage can kick in with increased revenue.

English

LibCapital

5.1K posts

@Lib_Capital

G10 FX, UK, US and European equities. Re-tweets/likes not always endorsements. Entirely opinion. No financial advice.

The 2nd Robot Marathon has officially begun in Beijing. This year feels different. 1. Around 40% of teams are running fully autonomous, no remote control. 2. Top robots are already hitting ~10s per 100 meter, getting surprisingly close to human sprint limits. 3. You can also see much better safety design upfront. Way more structured than last year’s chaos. 4. Still, failures happen. Marathon distance pushes motors, structure, and control to the limit. What works in short demos breaks down over longer runs. Overall, a big step forward, but also a reminder that real-world robotics is still far from the polished demo videos you get fed from companies.

Photonics is a bit confusing, hopefully this simplified summary helps. I have positions in $TSEM, $SOI, $ALMU, $LPKF

Now look at valuation context: $LITE - multi bn market cap $COHR - multi bn $FN - multi bn $SOITEC - multi bn $AXTI - multi bn All exposed to optical connectivity in different ways. IQE? £160m market cap. Yet it sits at a foundational upstream layer of the same ecosystem.

If you think you’ve “missed” $IQE after the recent move, zoom out. c$650m mcap, ~c5x sales - still trading at a steep discount to peers. That was always the thesis: it was so cheap that even a 2x rerate still leaves upside.

$IQE is one of two names on its layer. IQE FY25 $130M rev / $335M mcap - 2.6x sales $VPEC $114M (Q3'25 run-rate) / $1.4B mcap - 12.3x Landmark FY25 $69M rev / $4B mcap - 58x For the same photonics exposure, IQE stands out.

🧵 The NVIDIA Supply Chain Super cycle (2026) Here are Top NVIDA Suppliers growing Revenue Super Fast for investing opportunities Source: @tenet_research tenetresearch.ai The Top 10 Ranked by 2026 Growth Momentum 1. $MU (Micron Technology) Role: High Bandwidth Memory (HBM3E/HBM4). Catalyst: Revenue up nearly 200% YoY. They are effectively sold out through 2027 as AI chips require 3x more memory than traditional servers. 2. $AVGO (Broadcom) Role: AI Networking & Custom Silicon. Catalyst: Dominates the networking "fabric" (switches) that connects 100k+ GPU clusters. AI segment growing at triple digits. 3. $VRT (Vertiv Holdings) Role: Liquid Cooling & Power Infrastructure. Catalyst: Blackwell chips run so hot they require liquid cooling. $VRT is the industry standard for keeping "AI Factories" from melting. 4. $MRVL (Marvell Technology) Role: Optical Interconnects & Custom XPUs. Catalyst: Just secured a strategic partnership from $NVDA. Optical port demand is expected to double as data transfer speed becomes the new priority. 5. $AMKR (Amkor Technology) Role: Advanced Packaging (CoWoS). Catalyst: The #1 physical bottleneck. $AMKR is tripling Capex to package memory onto $NVDA GPUs to meet massive backlogs. 6. $VICR (Vicor Corp) Role: Power Conversion Modules. Catalyst: Providing high-density power modules for AI racks. Revenue is surging as power density becomes a critical data center constraint. 7. $TSM (Taiwan Semi) Role: The Sole Foundry. Catalyst: The world's foundry. They are the only ones capable of printing the ultra-advanced 3nm and 2nm designs for $NVDA. 8. $ASML (ASML Holding) Role: Lithography Machines. Catalyst: Record order backlogs from memory makers. You literally cannot build a modern AI chip without an $ASML machine. 9. $SKHYNIX (SK Hynix) Role: HBM Memory Leader. Catalyst: Operating profits are soaring as the primary first-mover for $NVDA’s newest memory architectures. 10. $ADI (Analog Devices) Role: Power Signal Management. Catalyst: Supplies precision components that keep power stable. Critical for the massive power stages in $NVDA’s latest hardware.

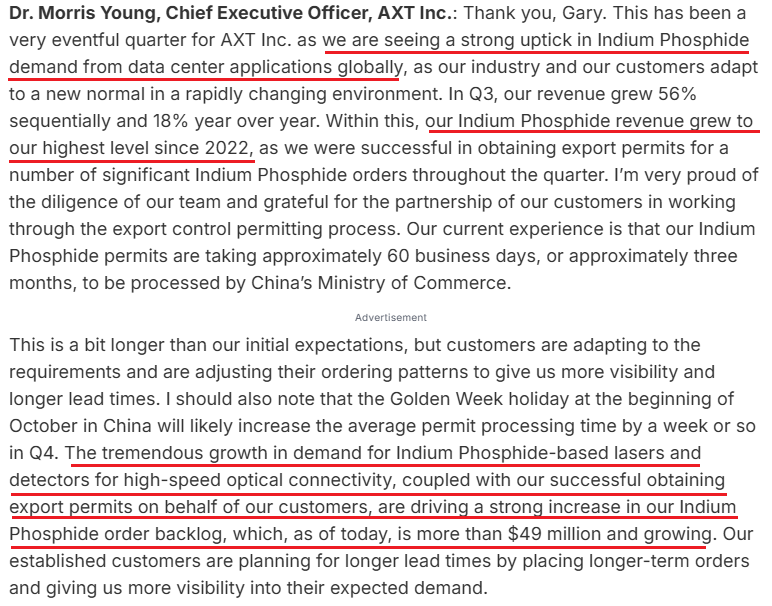

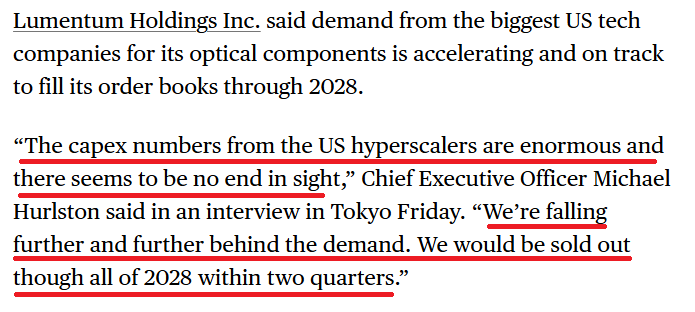

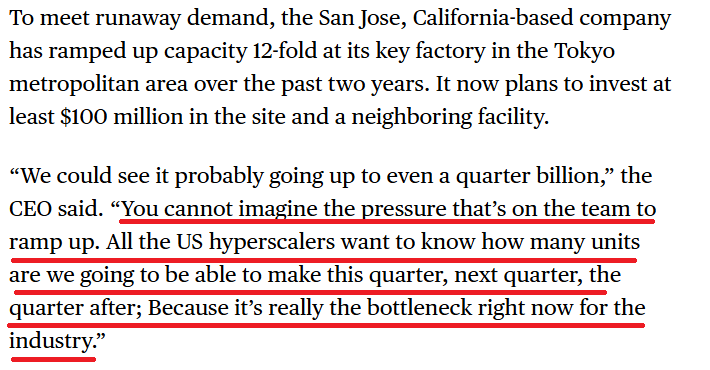

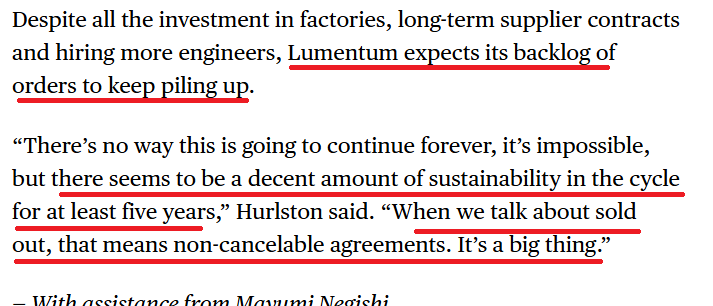

$IQE has a multi-year strategic supply agreement with $LITE. Refer to the screenshots to see what LITE's CEO is saying on demand. IQE is already embedded in LITE’s photonics supply chain - a standout picks and shovels play. Institutions are noticing. bloomberg.com/news/articles/…

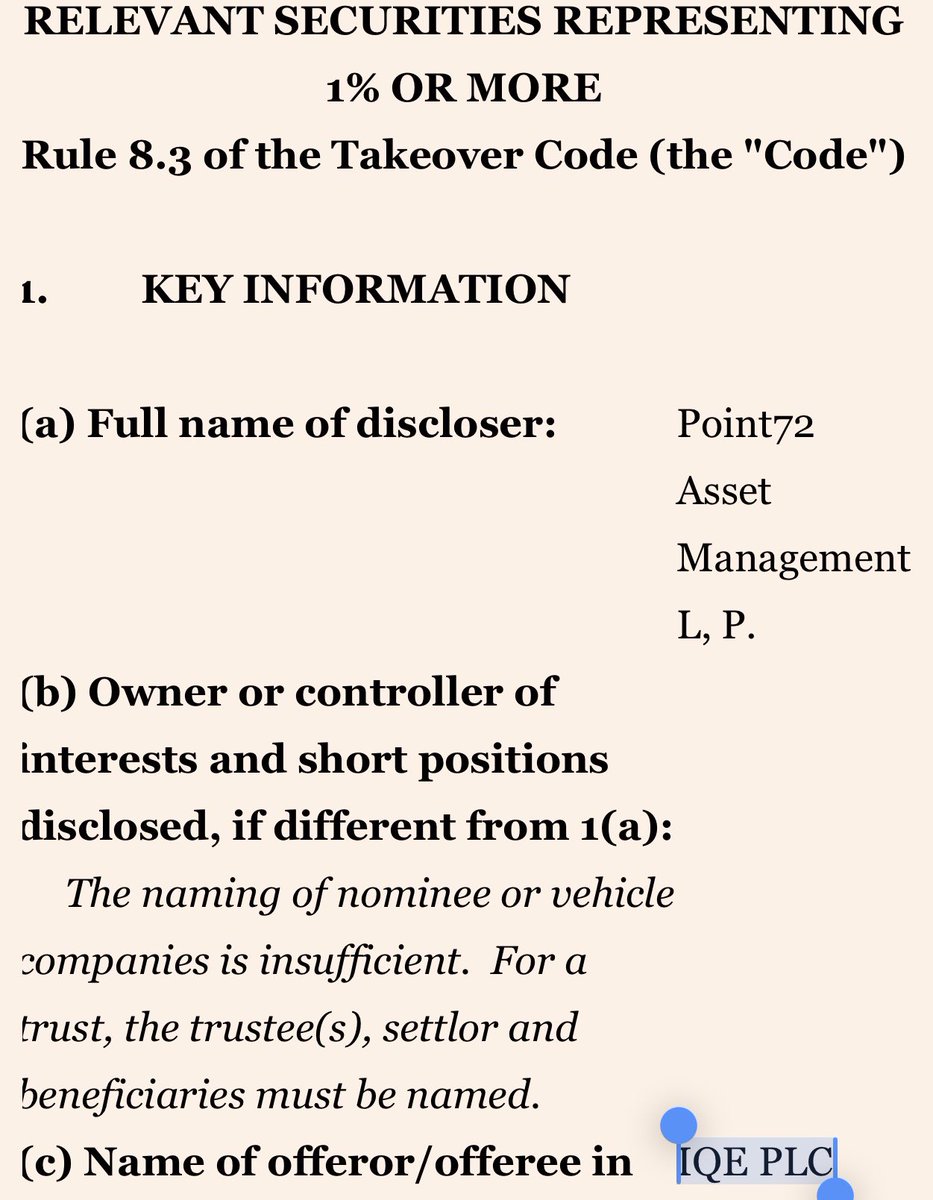

Didn’t I tell you all it’s possible retail can frontrun institutions anon?? -> Point72 is aggressively buying up $IQE 2 months later at ATHs... After my latent InP reactor capacity + $LITE supplier thesis post. -> Apollo literally bought out NSG, the $TSM COUPE glass provider I identified. -> And I've identified many others like $SIVE, the $MRVL / $JBL supplier to Riber the unknown quantum supplier to $MSFT (with the help of a friend) recently. I happen to like democratizing information discovery/synthesis to retail investors at the very beginning… Instead of selling analysis to institutions or behind $20000+ paywalls. Stocks are genuinely positive sum where retail can get the lead for the first time.

Was the first to talk about $AXTI in relation to photonics BOM/supply chains: $IQE is very interesting too as one of the only Western suppliers. Basically if you look at photonics flow on $GOOGL TPU/hyperscaler ASICs kinda looks like this (very likely, but undisclosed): Optical Transceivers (highest BOM): Lumentum/Cloud Light: ~ Vital / $AXTI-> $AXTI/Sumitomo/JX -> $IQE (Epi-Wafers) -> $LITE / Cloud Light -> $FN (Contract Manufacturing) -> $GOOGL TPU Merhcant optical supply chain: ~ Vital / $AXTI -> $AXTI / Sumitomo / JX -> → $LITE / $AVGO / $COHR (EML) + $MRVL / $MTSI / Semtech -> Innolight/Eoptolink -> $GOOGL So if you want moonshot-type photonics BOM / price-hikes stocks deeper upstream in the photonics BOM: $AXTI, $IQE and your way to go. $AXTI had terrible fundamentals before but the recent Northland fundraising round cemented its run. $IQE has terrible fundamentals now (Net debt £23.5 million) but is probably one of the most critical parts of the supply chain. If they manage to sell their Taiwan operations, wouldn't be surprised if it went up quite a bit just from their inp business. There's £18m convertible notes (which is basically nothing), then there's 120 to 154m new shares (~12% to 15%), which is also kinda nothing relative to current size. On the other hand, others $LITE and Innolight are probably more established. TLDR: $IQE -> seems critical to Western supply chains, $130MC. Net debt, if they sell Taiwan business -> strong re-rating or they might just dilute you anyway. But if the Taiwan business fails to be sold, probably expect to be diluted to oblivion like Wolfspeed. So huge, huge, risk ad do you own research into risks. But $AXTI and $IQE might are personally interesting to me (I do own $IQE).