Net new assets and the best censorship resistant, permissionless rails trading rails.

mert@mert

English

ryan

256 posts

@ryanchern

information @capitola_xyz | prev: @solana | podcast: https://t.co/l7DgfAYfJD

Prediction Market Notional Volume Recap (2026-03 vs 2026-02) 2026-03: $25.7B | 2026-02: $23.2B • Kalshi: $13.1B (+25.2% MoM) • Polymarket: $10.6B (+33.1% MoM) • Crypto(.)com: $629.7M (+58.5% MoM) • Opinion: $496.2M (-84.0% MoM) • Limitless: $464.5M (+25.2% MoM) • Predict: $329.7M (-58.0% MoM) • Myriad: $60.4M (-51.7% MoM) • IBKR: $41.2M (-35.0% MoM) • Gemini: $19.0M (+1932.1% MoM) • Overtime: $17.9M (+2.4% MoM) • Total: $25.7B (+10.6% MoM)

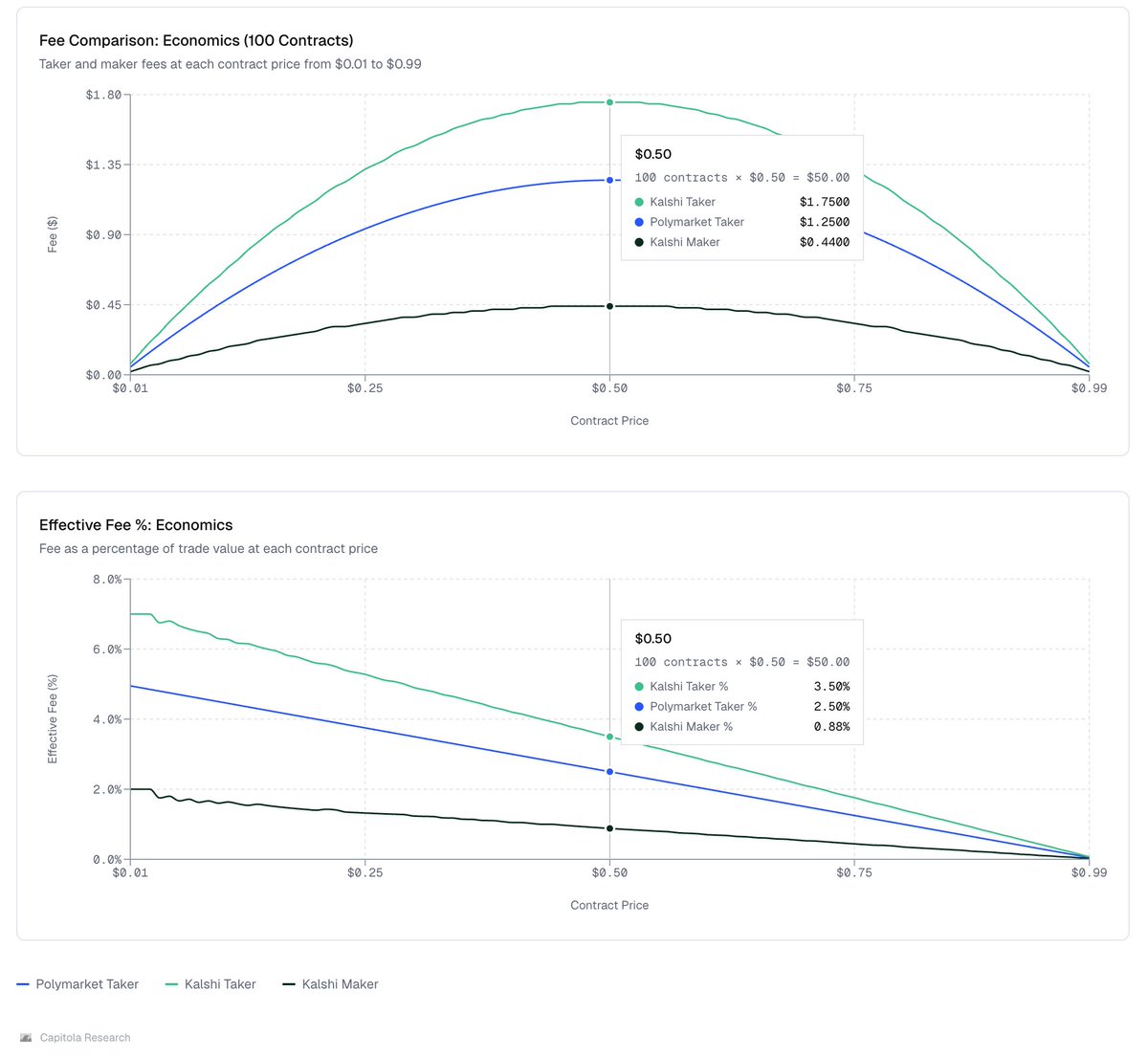

Polymarket's new fee structure creates the explicit incentive to call the splitPosition() function on markets and sell the shares below $0.50 to incur the minimum trading fee. - Buying 100 shares of YES @ 80c according to the Finance category fee schedule incurs a fee of $0.512. - Buying 100 shares of NO @ 20c incurs a fee of $0.128. If you want to go long YES @ 80c, you can either: 1. Directly buy YES shares 2. Call the splitPosition() contract, splitting $100 --> 100 YES + 100 NO shares for free, then sell 100 NO @ $0.20 Directly buying YES shares translates to 4x higher fees. For a $100,000 notional taker order, this is a $480 difference. Creating microstructure games like these further hurts retail traders who almost certainly are not aware of this dynamic. In addition to the downstream market quality effects this imposes, one could argue this shouldn't even be in Polymarket's first-order interest as this is a lever third party interfaces can implement and capture this spread.

Anecdotally feel the opposite: AI tools enable hyperproductivity as you don't have to spend mental energy on random blockers. Can work longer and feel less exhausted because the amount of deep work is distributed across the day.

$MSFT, down 24% YTD. Azure +39% YoY. $GOOGL, down 20% YTD. Trading at 17x earnings vs. a historical median of 26x. Google Cloud grew 48% last quarter though... $META — down 17% YTD. Ackman actually put $2B in and called it “one of the world’s greatest businesses.” Lol. The market is scared of capex. The ad engine doesn’t care. Although Zuck was obsessed with VR… $UBER — Ackman says it trades at “a massive discount to intrinsic value.” FCF up 34% YoY. 30%+ EPS growth expected. Personally I love Uber. $BN (Brookfield) — trading at a 22% discount to NAV. Record Q4 earnings. Bought back $1B of stock. Maybe getting hit by private credit fears but should he fine. $QSR (Restaurant Brands) — Burger King, Tim Hortons, Popeyes. Global franchise model returning 4.6% of market cap to shareholders this year. Restaurant stocks sold off on consumer fears that don’t apply to franchisors. Also BK objectively has better food than McD

If everyone has a resy bot, does anyone have one?

sponsoring market rewards is now open to all users 😛 add rewards to any market to get the liquidity for the size you want to trade. permissionless market deployment and creator fees next...