Strive paid a cash distribution for $SATA of $0.0542 per share, representing an annualized rate of $13.00 per share.

This payment marks the 16th consecutive distribution to shareholders.

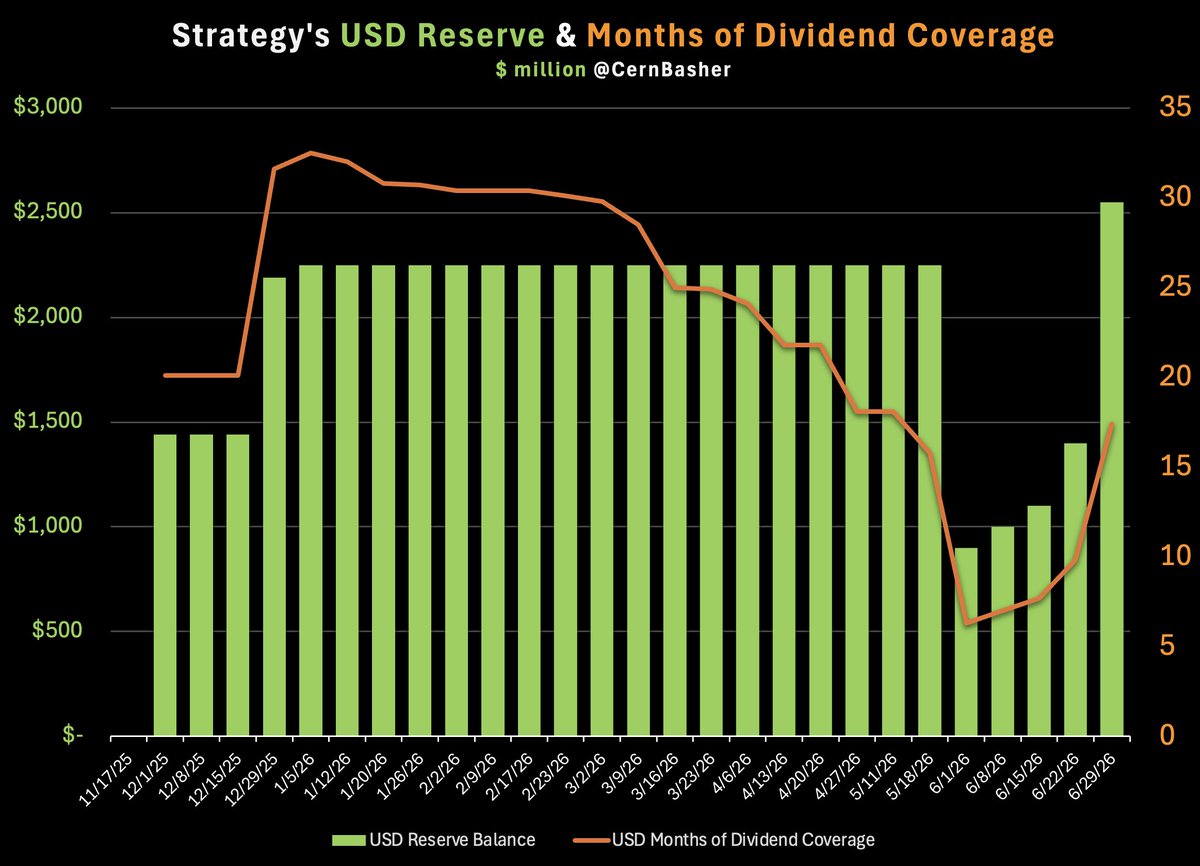

🔥STRATEGY ADDS $1.15 BILLION IN CASH TO USD RESERVE🔥

This was accretive to MSTR shareholders.

They issued 12.669M MSTR shares, raised $1.152B of cash, bought 0 BTC… and CEBE still went UP.

Why?

Because the USD reserve jumped to ~$2.55B, adding roughly 5.4 months of preferred dividend + interest coverage in one week.

CEBE rose from 138,657 to 139,135 sats/share.

That means the capital stack got stronger AND residual BTC-equivalent per common share increased.

This is why “did they buy Bitcoin?” is now the wrong question.

The real question is:

Did common shareholders own more residual BTC after senior claims?

This week: yes.

Accretive.

This was a great move for both MSTR shareholders and STRC investors.

Strategy announces a Digital Credit Capital Framework designed to strengthen Digital Credit, enhance liquidity, preserve long-term Bitcoin exposure, and support long-term value creation. $MSTR $STRC

strategy.com/press/strategy…

@CernBasher@saylor MSTR needs to hurry up and monetize its BTC stack by selling CSPs like Metaplanet or some other way. This would reduce the ponzi FUD

Strategy announces a Digital Credit Capital Framework designed to strengthen Digital Credit, enhance liquidity, preserve long-term Bitcoin exposure, and support long-term value creation. $MSTR $STRC strategy.com/press/strategy…

Michael Saylor’s Strategy announces a “Digital Credit Capital Framework” to help provide security during the bear market

This includes:

- Increase of BTC Reserve ~ $2.55 billion

- Openness to sell $1.25 billion in BTC

- Raising STRC dividend to 12%

- Buy backs of MSTR and STRC

7/ Bitcoin Monetisation Program

Strategy’s Board has authorised a Bitcoin monetisation program, allowing the company to sell BTC to:

- Build the USD Reserve.

- Fund or replenish dividends and interest.

- Fund accretive repurchases of Digital Credit Securities or common stock.

This tells me that Strategy is recognising the trade-off that comes with building a Bitcoin-backed Digital Credit platform.

If the company wants credit investors to trust the product, it needs liquidity, discipline and flexibility.

Strategy has established repurchase programs for up to $1.0B of our Digital Credit securities and up to $1.0B of $MSTR. This will create flexibility to accretively buyback securities during market dislocations. Repurchases will not be funded from the USD Reserve.

Estimates from reports and discussions put the number of EU-based Binance users at approximately 40–47 million of their 300 million worldwide, who could face disrupted access starting July 1.

Seattle (June 27) — Shocking video from the leftist pride event showing a violent far-left extremist running up to conservative live streamers and bashing them with a bat. The violence was approved by the queer activists.

@ChrisMMillas If you offer a guaranteed repurchase price (if trading under a certain market price) then it would become an attack vector for those who wish to destroy MSTR.

IMO confidence will grow after STRC survives a few more of these attacks.

Some thoughts on $STRC.

If you offered investors an 11.5% yield and could guarantee the dividends would be paid for the next 10 years, I think most people would take that deal.

So the issue isn’t the yield.

The issue is confidence in the sustainability of that yield over time.

Strategy therefore needs to convince the market that it can reliably meet its dividend obligations through *all market conditions.*

Given Bitcoin’s volatility, the best way to do that is by maintaining a USD Reserve large enough to cover ~five years of dividend payments — effectively spanning a full traditional Bitcoin cycle.

That kind of reserve would give investors greater confidence to hold the product through periods of stress.

Combine that with a commitment to repurchase $STRC whenever it trades below a predetermined threshold and you significantly reduce volatility and create a far more stable product.

And that alone would likely reduce the need to actually repurchase shares.

Much like the Fed’s “whatever it takes” moment, the commitment itself often stabilises conditions before action is even required.

As both $BTC and $STRC mature and earn greater trust, the size of the reserve can fall in line with that trust.

Let me make this crystal clear for Ionic Digital shareholders..

Institutional investors just bought 7.474M shares and paid for each of them 🚨 $53.52 🚨!

These institutional investors aren't here for small gains; they expect to make a significant return on this capital.

It's also fair to conclude they expect liquidity sooner rather than later, and that Ionic is using this capital raise to anchor price expectations before public trading begins!

Backing the now ~44.84M shares:

• +2,861 BTC (~$171M)

• +$400M fresh cash

• $ 304M non-current assets (FYE’24)

• $ 1.95B in 10-year HPC leases

• $ 741M in Expanded HPC contract coming Q2 ’27

How bullish are you? Drop your target price 👇 #IonicDigital#CelsiusNetwork

I will die on this hill and it requires urgent attention.

I have found a fundamental flaw in the mechanism Strategy uses to adjust $STRC's yield and I cannot unsee it.

The 30-day VWAP framework is grossly inadequate and hides the truth about the health of the product.

Around ex-dividend dates there is a well known arbitrage play. Traders buy $STRC in the days before the record date to capture the dividend, artificially inflating both price and volume in that window.

Because VWAP is volume weighted, those high volume days near par carry disproportionate weight in the calculation and it's a small distortion. Volumes around ex-dividend dates are dramatically higher than on a typical day, meaning those few days can dominate the entire 30-day average.

The result is that the 30-day VWAP can sit comfortably between $99 and $100 even when the product spends most of the month well below par.

The framework says performance is healthy but in actuality it is not.

Moving to bi-monthly dividends will help by compressing the arbitrage window, but it does not fix the underlying problem. The distortion just happens twice a month instead of once.

Days at par is a far better metric to evaluate.

It asks one simple question. How many days did the product actually close at or above $100? No volume weighting or dividend arbitrage distortion, just a binary answer to whether the product is functioning as intended.

This needs to be fixed ASAP and I hope @saylor considers revisiting this guidance.