@mr_deepvalue Looks interesting. Going into an investment phase it seems, historical ROIC doesn't look great, so unless something has changed, more investment will likely yield a substandard return.

There’s a company in the UK that designs security systems for critical infrastructure. It’s been around for decades. Today you can buy the operating business for £19m while it quietly generates £4m in owner-adjusted FCF. Net cash is £13m. The market thinks it’s dying. The numbers suggest otherwise.

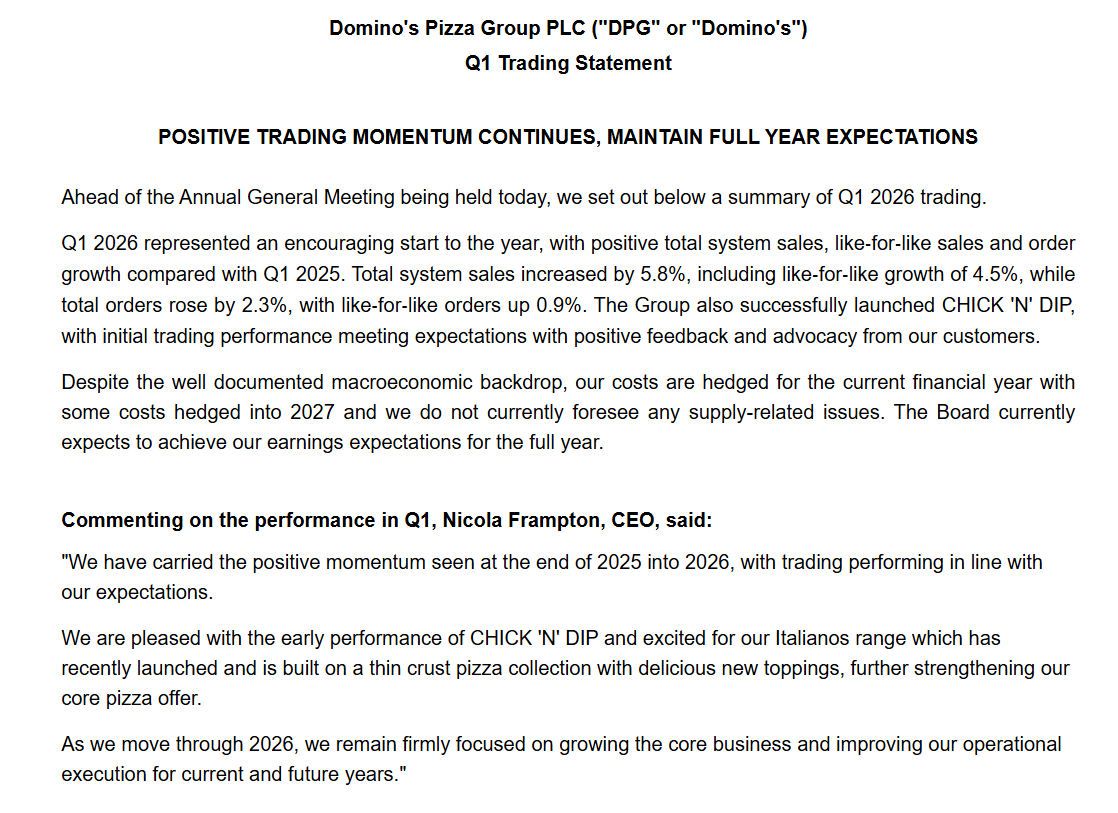

Positive $DOM.L #DOM trading update. Strong system sales growth which surprised me. Total orders returning to growth is really important as most revenue comes from selling ingredients to franchisees, so more orders = more ingredients needed. I like the continued focus on core.

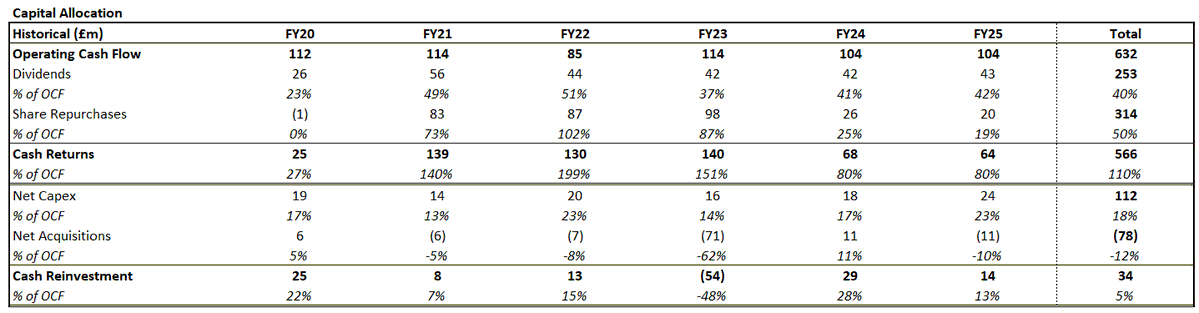

Large share repurchases were made from FY21-23 at average price of 349p (91% premium to current) at much higher P/E ratios, this is an example of poor share repurchases which destroyed value. Due to such depressed P/E ratios currently that same mistake cant happen at these prices

Doing some digging into #DOM $DOM.L. 110% of OCF has been returned to shareholders over the last 6 years. 5% reinvested. Should this simply be valued at a cash return yield? Assuming a £104m OCF and all of that returned that's a 10.3% cash yield, with maybe some growth potential?

Some of the best deep value / special sits blogs I've started following over the last 12 months, a mix of private investors and funds, all worth bookmarking 👇

1) @everyonehatesp1: Small & micro-cap ideas with inflection and catalyst-rich trades

2) @MaiusPartners: Deep dives on global value stocks

3) Tactile Find: Alluvial Capital's new fund, LT investing in firms with extraordinary physical assets

4) @DismAssetBkd: Small cap net-net / deep value.

5) @SnowsofNebraska: Special sits focused with a great blog

6) @DWPartnership: Value / special sits leaning fund blog

7) @e_pap4: Microcap investor going through the most obscure deep value bets

8) @JustValue48: Special sits focused in the small/midcap space

9) @RodAlzmann: Special sits focused private investor

10) Illiquid Edge: Obscure, illiquid microcap stocks

Anyone I'm missing? Drop names below 👇

New Write Up: SaaSpocalypse survivor? 1.7x EV/ARR with incentive to return £150m to shareholders (Market Cap £35m)

#GETB $GETB.L

open.substack.com/pub/dwpartners…

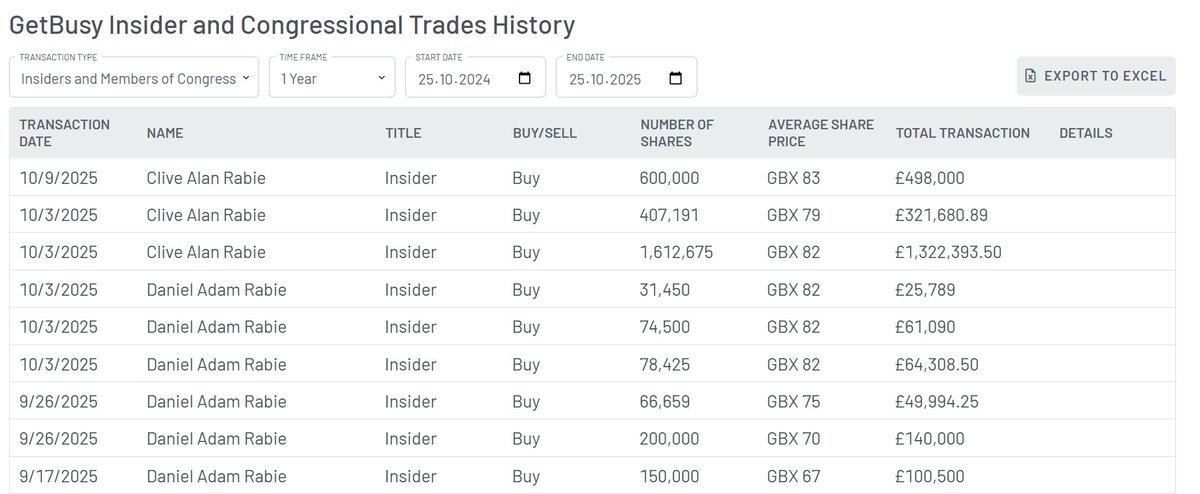

Getbusy $GETB.L leadership been buying hundreds of thousands of £ of shares. It’s a £40m market cap company that operates a platform of task management and collaboration solutions.

Growing 15-20%

Management are bullish. One of them now owns 23% of company

$GETB

@cermrew Agreed the insider buying is encouraging, especially with how open they are about selling SmartVault, shows they must see a serious potential of getting a deal done. I have also written a bit more here: open.substack.com/pub/dwpartners…

Recently took a stake in $GETB.L. I'm usually skeptical of big promises in company slides, but when insiders go through the pain of de-recognition as a concert party and then aggressively buy shares at increasing prices, that's a strong signal.

@Compoundandfire Nice to see Smartvault reaching profitability too. Worried slighly about Workiro but hopefully can return it to growth. I have written a bit more here if want to check it out and discuss. open.substack.com/pub/dwpartners…

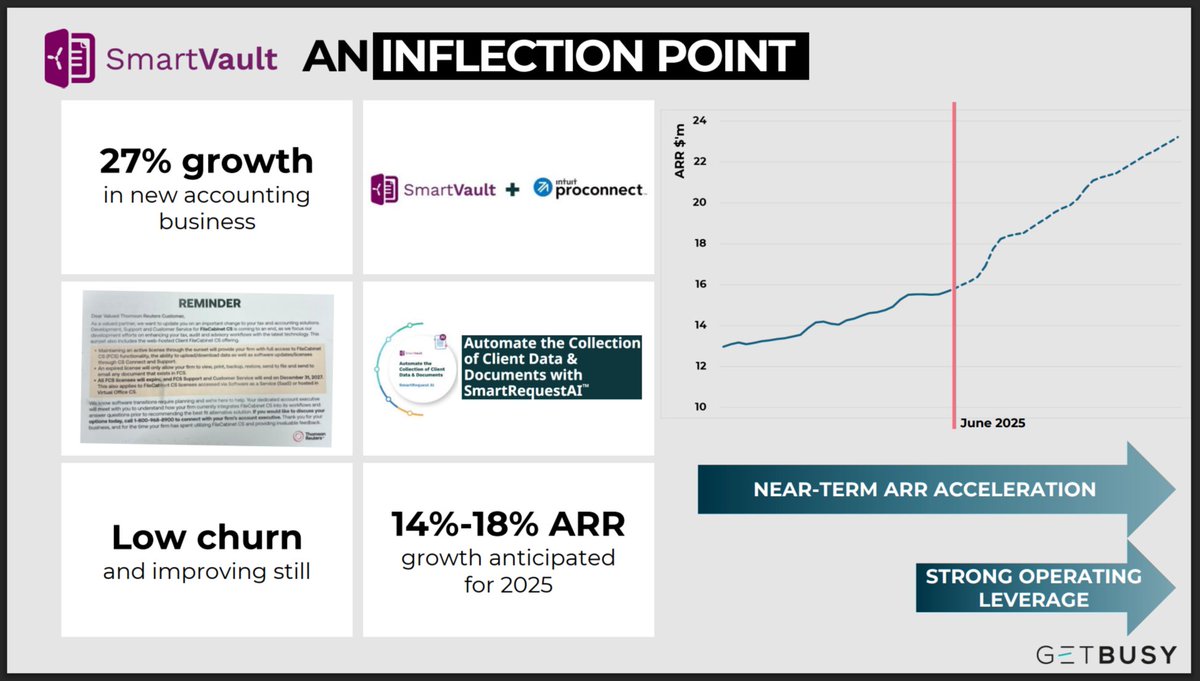

Revenue growth on SmartVault is accelerating. This is the upside of $GETB.L I was expecting and exciting to see how fast growth continues in 2026. polaris.brighterir.com/public/getbusy…

After 60 years, Warren Buffett stepped down as CEO of Berkshire Hathway.

Greg Abel just published his first shareholder letter.

To honor the Oracle of Omaha's legacy, we asked Computer to build something to make sure Buffett's wisdom lives on.

Introducing the Buffett Archive.

@finphysnerd I agree but I think the downside is not as steep as 30%. The largest shareholder owns 29% and has an advisor who is the chair of Titon, so I would imagine, if things are going south they would be prompt in pushing for a liquidation. FCF positive 9 out of last 11 years to also.

@DWPartnership Good writeup and an interesting setup. Warehouse provides downside protection, but the only world in which it's monetised is a liquidation where the cash is probably gone already, so downside is probably a few years opportunity cost and 30% downside to factory value.

@Jave_t23 CEO,CFO and Chair own about 8.3% of the company including there stock options. Also the chair has purchased £100k of stock in the open market over the last 24 months so, they are incentivised to see the stock doing well. I suspect they will look to sell to a bigger player.

@DWPartnership There was a point early last year when I was very up to date on it but I passed, evidently the correct choice, due to the outlook for the business at that point. If I remember correctly management are fairly well incentivised despite not owning much.

I posted a new write up on a nanocap

• 86% Recurring Revenue

• 7x FCF

• Revenue has grown from £4 million to £20 million in 4 years

• FCF goal of £5 million a year in 3 years on a £17 million market cap

Link in Bio

$REAT.L