SFYL

1.2K posts

SFYL

@SFYLL

Ex TradFi, Ex @wintermute_t Building at @homeDAO https://t.co/lPd3KhgWvH

Paris انضم Şubat 2012

1.2K يتبع994 المتابعون

End of the road for parsec I'm afraid. The market zigged while we zagged a few too many times

A little parsec lore for posterity, In early 2020 I started charting uniswap *v1* charts as a side project, this spiraled into a full blown DeFi terminal during DeFi summer and into the 2021 craziness. Our big break was DeFi completely unwinding its insane leverage in 2022, first wonderland, then ohm, then terra, then 3ac/stETH depeg. Lots of firms and traders were using parsec to navigate (and in some cases being the ones getting liquidated!).

Post FTX DeFi spot lending leverage never really came back in the same way, it changed, morphed into something we understood less, activity onchain changed hugely in a way that I never fully grokked. We had pockets of life after that, Friendtech (rip), our polymarket election dash that grabbed a few hundred thousand hits in 1 night. But nothing stuck as the ephemerality of crypto crept in (more on this another time).

I've made about a thousand mistakes along the way but the team I built was not one of them, a group of hardworking, knowledgable and overall good people with the unwavering @bshee1102 as my right hand from the very early days

My vision was for DeFi to reinvent finance and permeate the opaque and gated systems of old, a vision I still hold (perhaps masochistically). Parsec was a part of the very beginning of this and will sadly not be of part of the long journey the industry has left.

I'm not going anywhere, will be doing some writing and finding new ways to contribute. Onwards!

parsec@parsec_finance

After 5 years, parsec is shutting down. Not how we wanted our story to end, but we are proud of what we built and the value we provided along the way. We are eternally grateful to those that traversed the ups and downs onchain with us. It was quite the ride 🔭

English

@jupiters_string had a look on the nike side, trend is diversifying partners for the innovation labs (project amplitude with Dephy, Hyperbook with Hyperice). Also common projects stopped (Apple Watch). Unsure where they can meet, Nike prob can't produce good crystal tech for AR. "Cheap" tho

English

@alexocheema @awnihannun @angeloskath Given that agentic workloads amplify KV-cache and memory pressure, one should favor architectures and vendors that can sustain long context with low latency and high concurrency. Is Exo the local solution?

English

Two misconceptions about clustering here:

1/ The ONLY benefit of clustering multiple machines is being able to run larger models.

Not true. With low-latency RDMA over Thunderbolt released in macOS 26.2 and the MLX Jaccl backend (h/t @awnihannun, @angeloskath) you get a speed-up as you add more devices. E.g. Llama 3.3 70B runs 1.8x faster on 2 Macs and 3.2x faster with 4 Macs (not quite linear, but that's the case with NVIDIA and NVLink too...)

2/ It costs $10,000 to get started.

No. @exolabs runs on a base Mac Mini that you can pick up for $479. You can even cluster this with a MacBook. RDMA supports any Thunderbolt 5 enabled device including a M4 Pro Mac Mini ($1,399) and a M4 Pro MacBook ($1,999). You can even cluster with a friend who also has a MacBook and run large models at faster speeds than on a single MacBook.

Dave W Plummer@davepl1968

We keep getting offers to run Ai clusters - GB10s, Mac Studios, etc. It's tempting, because I love hardware, but I keep saying no. I've already got a Mac w/ 128GB. As far as I can tell, the ONLY benefit of clustering multiple machines together seems to be the ability to run a larger model, albeit quite slowly. Yawn. I don't know how to make an episode about how running a big model slowly at home for ten thousand dollars into compelling content. What the heck would you do with four 128GB Macs if you had them besides pose with them? And this guy has five!

English

@jacquesmarron @aleph_im It could be, but imho simpler = better. This MVP doesn't have many dependencies, it's better to test the market at first vs making a tech Frankenstein to realize your product is off the mark

English

@SFYLL Nailed it — cross-chain relayers like Across are ideal for undercollateralized lending thanks to their fully transparent, on-chain track records.

@aleph_im could supercharge this: decentralized compute for running solvers trustlessly, immutable storage for performance history, and confidential VMs for verifiable credit scoring without exposing sensitive data.

This unlocks capital for capital-constrained relayers while staying 100% decentralized. What do you think? 🚀

English

What differentiates cross-chain solvers from the rest in the picture?

Cross-chain solvers are capital constrained.

Take Across, one of the largest bridging protocols. It routinely bridges around $1B monthly. Yet its largest relayer is the Across team itself, which maintains its edge despite running open-source code. What sets it apart? Capital — multiples more than any competitor.

Relayers are also pristine borrowers. Their balance sheets and income statements are open, auditable, and engraved on the blockchain. I posit that they are the best niche to start building robust, undercollateralized lending on DeFi rails.

Check out more on sfyl sub tack

English

@merklefruit 100%. At first you can avoid liquidations with well calibrated computations if NPV of future cash flows > NPV defaulting. Indeed, assuming there is no competition, to default also means to let go of your business, given your capital cost will then be higher than the competitors'

English

From an essay I wrote (focused on the UK, can expand to continental EU, ASML Netherlands, etc). Would look at the data, as this narrative is strongly pushed over social-medias on which some sovereign states have more control than others:

The United Kingdom makes for a perfect testing ground. Possessing a unique regulatory agility post-Brexit compared to its European neighbors, it also has a long-lasting history of successfully cultivating a world-leading deep-tech ecosystem. London-based DeepMind delivered AlphaFold, solving one of biology's greatest challenges. In hardware, Cambridge-designed ARM architecture powers the vast majority of the world's smartphones. Thenation pioneered the integration of whole-genome sequencing into a national health service. In energy, the Culham Centre for Fusion Energy continues to be a global leader with its ambitious STEP program. In distributed systems, the UK is a major hub, hosting foundational companies for leading DeFi protocols like Aave. This pro-innovation environment is perhaps best exemplified by the Financial Conduct Authority’s pioneering 'regulatory sandbox,' a model now adopted globally that cements the UK’s role as a crucible for the industries of tomorrow.

English

@robustus They are pretty competitive when it comes to quantum believe it or not

English

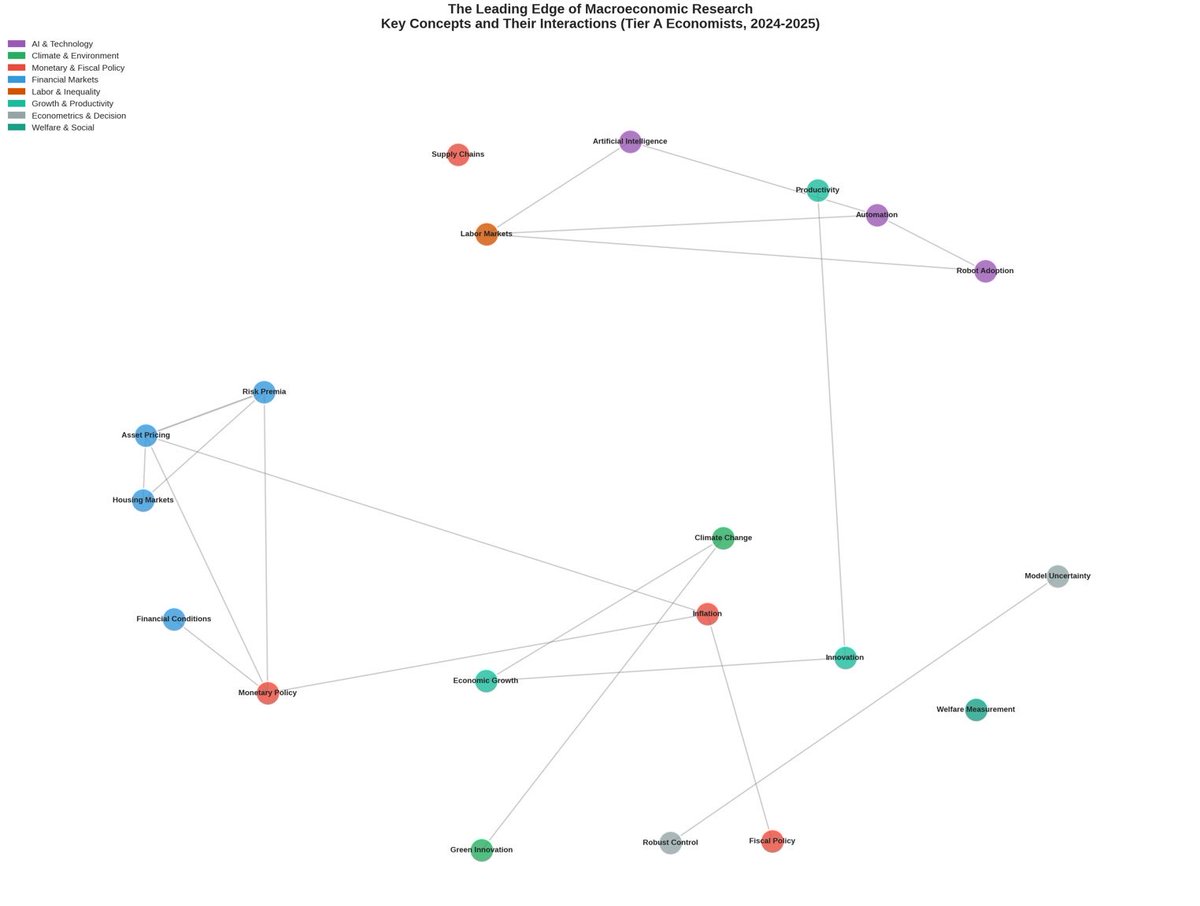

The network graph shows common core macroeconomic concepts behind frontier research of Tier A macroeconomists published from 2024 onwards. In other words, what topics keep "preoccupied" the best macroeconomist. The connections in the network graph are shared research concepts between papers.

sourced from PSDMACRO agentic workflows

English

@Citrini7 Indeed, I just copy pasted and switched few terms, this is what you get, though I didn't understand he went short

x.com/SFYLL/status/1…

SFYL@SFYLL

THE CASE FOR TREASURY COMPANIES (July 2025) THE CONCEPT Superficially, treasury companies seem to resemble exchange traded funds designed to provide exposure to cryptocurrencies. But the analogy is misleading. The true attraction of treasury companies lies in their ability to generate capital gains for their shareholders by selling additional shares at a premium over book value. If a trust with a book value of $10 and a 12% return on equity doubles its equity by selling additional shares at $20, the book value jumps to $13.33 and per-share earnings go from $1.20 to $1.60. Investors are willing to pay a premium because of the high yield and the expectation of per-share earnings growth. The higher the premium, the easier it is for the treasury company to fulfill this expectation. The process is a self-reinforcing one. Once it gets under way, the trust can show a steady growth in per-share earnings, even if it were to distribute practically all its earnings as dividends. Investors who participate in the process early enough can enjoy the compound benefits of a high return on equity, a rising book value, and a rising premium over book value. ANALYTICAL APPROACH The conventional method of security analysis is to try and predict the future course of earnings and then to estimate the price that investors may be willing to pay for those earnings. This method is inappropriate to the analysis of treasury companies because the price that investors are willing to pay for the shares is an important factor in determining the future course of earnings. Instead of predicting future earnings and valuations separately, we shall try to predict the future course of the entire self-reinforcing process. We shall identify three major factors which reinforce each other and we shall sketch out a scenario of the probable course of development. The three factors are: 1. The effective rate of return on the Treasury company's capital 2. The rate of growth of the treasury company’s size 3. Investor recognition, i.e., the multiple investors are willing to pay for a given rate of growth in per-share earnings THE CATCH Everything above is taken verbatim from Soros’ The Alchemy of Finance (p. 61). The only modifications were: “February 1970”, “Mortgage Trusts” and “Mutual Funds” for respectively “July 2025”, “Treasury Companies” and “Exchange Traded Funds”. Finally, “despite the fact that it” was replaced by “even if it were to” to better represent the lack of dividends for treasury companies ("T Cos"). Obviously, this thesis touches on T Cos for which the underlying offers yield-generation opportunities at the very least, as does real estate. Hence, we’ll be focusing on Ethereum T Cos while laying down our scenario, parting with the quotation framework but maintaining Soros' format. THE SCENARIO Act One: The stage is set in the wake of a deleveraging event. On-chain activity has dried up, establishing a stable floor for Ethereum's staking yield, while only the most robust DeFi protocols have survived, outlasting their centralized competitors. This pristine environment coincides with a flurry of regulatory strides, from ETF approvals to new legislation, channeling historic capital inflows into the digital asset space. This has spurred a multiplication of investment vehicles, which are now expanding beyond Bitcoin to capture the yield-bearing potential of assets like Ethereum, igniting the self-reinforcing process. Act Two: As these Treasury Companies deploy capital, a new feedback loop emerges: their on-chain activity directly increases the base staking yield, boosting their own top-line revenue. By putting capital to work, they make their own vehicles more attractive, growing both ETH-per-share and yield-per-share. The market rewards this growth by maintaining the premium over NAV, which in turn enables accretive share issuance that further boosts yield-per-share. Competitors, attracted by these returns, enter the fray but, lacking a unique strategy, struggle to differentiate themselves. Act Three: Increasing competition for capital forces T Cos to take greater risks to justify their book value premiums. This manifests in two ways: applying significant leverage to the balance sheet (the primary strategy for T Cos holding non-yielding assets like Bitcoin) and, for the rest, moving further down the on-chain risk curve to magnify yields. They navigate beyond blue-chip protocols, allocating to novel applications without a proven history—the DeFi equivalent of subprime. This flood of capital inflates the valuation of the underlying DeFi protocols themselves, and ultimately Ethereum’s valuation, further boosting the T Cos' NAV and masking the danger. Initial losses from minor protocol incidents are quickly overcome by the sheer momentum of the rising market. Act Four: Investor disappointment from a major loss event will shatter the narrative and affect the valuation of the entire group. A lower premium coupled with slower growth and compressing yields will in turn crush the per-share earnings progression. The multiple will collapse, often turning a premium into a steep discount to NAV. The group will go through a violent shakeout period. After the shakeout, the industry will have matured: there will be fewer new entries, regulations may be introduced, and the surviving Treasury Companies will settle down to a more moderate, sustainable growth based on a more conservative strategy. EVALUATION The primary danger, at present, is that the self-reinforcing process may not get under way at all. In a serious market decline, investors may be unwilling to pay any premium, nipping the cycle in the bud. However, the survival and performance of MicroStrategy through the 2022 market decline suggests a degree of resilience, particularly for entities with savvy capital structures that favor long-term debt, itself unattainable for individuals. Furthermore, the macro-political environment appears uniquely favorable. The passage of landmark regulations cemented Bessent public strategy to rely on stablecoin for government funding, effectively its sole lifeline at the current deficit level. It is thus in the US government’s interest to foster a vibrant on-chain capital market. Ultimately, the stage is set to unleash the self-reinforcing process. The return potential for these companies is multi-faceted, extending far beyond a simple staking yield. Take for example Sharplink Gaming. It could earn a base Yield-per-Share (YPS) of $0.401 from its initial equity through staking alone, assuming a 3% staking rate. It can resort to either equity issuance or leverage (most likely both) to magnify this number. First, the company can issue shares at its premium to NAV. A quick back-of-the-napkin math shows that a 66% expansion of the asset base, funded by selling shares at the current 1.91x multiple, would increase the YPS from $0.401 to $0.476, assuming no market impact on both legs. This is a direct testament to reflexivity and how people’s perception, reflected in the book value premium, can shape better fundamentals. Second, through financial engineering, the company can add leverage. If Sharplink were to issue 0% convertible senior notes, as did MicroStrategy. At a 0.5x debt-to-equity ratio, again assuming no market impact, YPS would jump from $0.401 to $0.601, or $0.801 at 1x. The existence of these two independent and powerful mechanisms for amplifying shareholder returns—one reliant on market sentiment, the other on access to capital markets— forms a compelling case for a significant and durable premium over book value. If the reflexive process fails to launch, investors would find downside protection in the company's book value. A modest premium over NAV seems justified even in the absence of growth, given the baseline yield generation. The primary challenge for investors is not the thesis, but securing an entry at these low premiums, though opportunities have presented themselves punctually. If the self-reinforcing process does get under way, shareholders in well-managed Treasury Companies should enjoy the compound benefits of a high return on equity, a rising book value, and a rising premium over book value. But in this thesis, there is a final accelerant: the T Cos' own activities—generating on-chain transactions and locking up supply—directly improve the fundamentals of the underlying asset itself, further amplifying the reflexive loop.

English

it’s literally almost the same example if you read about the mREITs trading at a premium to NAV when Soros shorted them

Citrini@citrini

With MSTR, Saylor has created the best real life example of reflexivity ever. Like way better than the mortgage REIT example soros used in Alchemy of Finance.

English

@HugoMartingale @cobie jailcobie.sfyl.xyz

had made this, if people want to crowdfund can update to latest price tag, not usable right now

English

@Galois_Capital If you sell the underlying that may have more than an adverse effect on financial ratios, breaking the reflexive link. Effectively you should only sell to wind out the company and distribute cash to shareholders... unlikely.

x.com/SFYLL/status/1…

SFYL@SFYLL

THE CASE FOR TREASURY COMPANIES (July 2025) THE CONCEPT Superficially, treasury companies seem to resemble exchange traded funds designed to provide exposure to cryptocurrencies. But the analogy is misleading. The true attraction of treasury companies lies in their ability to generate capital gains for their shareholders by selling additional shares at a premium over book value. If a trust with a book value of $10 and a 12% return on equity doubles its equity by selling additional shares at $20, the book value jumps to $13.33 and per-share earnings go from $1.20 to $1.60. Investors are willing to pay a premium because of the high yield and the expectation of per-share earnings growth. The higher the premium, the easier it is for the treasury company to fulfill this expectation. The process is a self-reinforcing one. Once it gets under way, the trust can show a steady growth in per-share earnings, even if it were to distribute practically all its earnings as dividends. Investors who participate in the process early enough can enjoy the compound benefits of a high return on equity, a rising book value, and a rising premium over book value. ANALYTICAL APPROACH The conventional method of security analysis is to try and predict the future course of earnings and then to estimate the price that investors may be willing to pay for those earnings. This method is inappropriate to the analysis of treasury companies because the price that investors are willing to pay for the shares is an important factor in determining the future course of earnings. Instead of predicting future earnings and valuations separately, we shall try to predict the future course of the entire self-reinforcing process. We shall identify three major factors which reinforce each other and we shall sketch out a scenario of the probable course of development. The three factors are: 1. The effective rate of return on the Treasury company's capital 2. The rate of growth of the treasury company’s size 3. Investor recognition, i.e., the multiple investors are willing to pay for a given rate of growth in per-share earnings THE CATCH Everything above is taken verbatim from Soros’ The Alchemy of Finance (p. 61). The only modifications were: “February 1970”, “Mortgage Trusts” and “Mutual Funds” for respectively “July 2025”, “Treasury Companies” and “Exchange Traded Funds”. Finally, “despite the fact that it” was replaced by “even if it were to” to better represent the lack of dividends for treasury companies ("T Cos"). Obviously, this thesis touches on T Cos for which the underlying offers yield-generation opportunities at the very least, as does real estate. Hence, we’ll be focusing on Ethereum T Cos while laying down our scenario, parting with the quotation framework but maintaining Soros' format. THE SCENARIO Act One: The stage is set in the wake of a deleveraging event. On-chain activity has dried up, establishing a stable floor for Ethereum's staking yield, while only the most robust DeFi protocols have survived, outlasting their centralized competitors. This pristine environment coincides with a flurry of regulatory strides, from ETF approvals to new legislation, channeling historic capital inflows into the digital asset space. This has spurred a multiplication of investment vehicles, which are now expanding beyond Bitcoin to capture the yield-bearing potential of assets like Ethereum, igniting the self-reinforcing process. Act Two: As these Treasury Companies deploy capital, a new feedback loop emerges: their on-chain activity directly increases the base staking yield, boosting their own top-line revenue. By putting capital to work, they make their own vehicles more attractive, growing both ETH-per-share and yield-per-share. The market rewards this growth by maintaining the premium over NAV, which in turn enables accretive share issuance that further boosts yield-per-share. Competitors, attracted by these returns, enter the fray but, lacking a unique strategy, struggle to differentiate themselves. Act Three: Increasing competition for capital forces T Cos to take greater risks to justify their book value premiums. This manifests in two ways: applying significant leverage to the balance sheet (the primary strategy for T Cos holding non-yielding assets like Bitcoin) and, for the rest, moving further down the on-chain risk curve to magnify yields. They navigate beyond blue-chip protocols, allocating to novel applications without a proven history—the DeFi equivalent of subprime. This flood of capital inflates the valuation of the underlying DeFi protocols themselves, and ultimately Ethereum’s valuation, further boosting the T Cos' NAV and masking the danger. Initial losses from minor protocol incidents are quickly overcome by the sheer momentum of the rising market. Act Four: Investor disappointment from a major loss event will shatter the narrative and affect the valuation of the entire group. A lower premium coupled with slower growth and compressing yields will in turn crush the per-share earnings progression. The multiple will collapse, often turning a premium into a steep discount to NAV. The group will go through a violent shakeout period. After the shakeout, the industry will have matured: there will be fewer new entries, regulations may be introduced, and the surviving Treasury Companies will settle down to a more moderate, sustainable growth based on a more conservative strategy. EVALUATION The primary danger, at present, is that the self-reinforcing process may not get under way at all. In a serious market decline, investors may be unwilling to pay any premium, nipping the cycle in the bud. However, the survival and performance of MicroStrategy through the 2022 market decline suggests a degree of resilience, particularly for entities with savvy capital structures that favor long-term debt, itself unattainable for individuals. Furthermore, the macro-political environment appears uniquely favorable. The passage of landmark regulations cemented Bessent public strategy to rely on stablecoin for government funding, effectively its sole lifeline at the current deficit level. It is thus in the US government’s interest to foster a vibrant on-chain capital market. Ultimately, the stage is set to unleash the self-reinforcing process. The return potential for these companies is multi-faceted, extending far beyond a simple staking yield. Take for example Sharplink Gaming. It could earn a base Yield-per-Share (YPS) of $0.401 from its initial equity through staking alone, assuming a 3% staking rate. It can resort to either equity issuance or leverage (most likely both) to magnify this number. First, the company can issue shares at its premium to NAV. A quick back-of-the-napkin math shows that a 66% expansion of the asset base, funded by selling shares at the current 1.91x multiple, would increase the YPS from $0.401 to $0.476, assuming no market impact on both legs. This is a direct testament to reflexivity and how people’s perception, reflected in the book value premium, can shape better fundamentals. Second, through financial engineering, the company can add leverage. If Sharplink were to issue 0% convertible senior notes, as did MicroStrategy. At a 0.5x debt-to-equity ratio, again assuming no market impact, YPS would jump from $0.401 to $0.601, or $0.801 at 1x. The existence of these two independent and powerful mechanisms for amplifying shareholder returns—one reliant on market sentiment, the other on access to capital markets— forms a compelling case for a significant and durable premium over book value. If the reflexive process fails to launch, investors would find downside protection in the company's book value. A modest premium over NAV seems justified even in the absence of growth, given the baseline yield generation. The primary challenge for investors is not the thesis, but securing an entry at these low premiums, though opportunities have presented themselves punctually. If the self-reinforcing process does get under way, shareholders in well-managed Treasury Companies should enjoy the compound benefits of a high return on equity, a rising book value, and a rising premium over book value. But in this thesis, there is a final accelerant: the T Cos' own activities—generating on-chain transactions and locking up supply—directly improve the fundamentals of the underlying asset itself, further amplifying the reflexive loop.

English

DAT Mechanics Part 1

Some folks saying this the next LUNA (it’s not). Others are saying there’s nothing to unwind (there is). Think carefully about the mechanics.

A lot of these DATs have no leverage so there won’t be any forced selling from getting called on debt. Still there is an incentive to sell the underlying and buy the stock back to capture the arb and push mNAV up. But how much of an incentive is there and how far up should mNAV be. This largely depends on the underlying asset. In the case of BTC, there is one very large player (MSTR) and many much smaller players. So you could say that MSTR alone as a DAT drives BTC price. Since mNAV here is healthy and since the leverage is controlled well, you probably won’t see much selling of the underlying here. As a side note, it makes sense that the debt is at a safe level since Saylor got such a great deal against the buyers of the early converts since he was the only game in town selling crypto upside to fixed income desks.

Now imagine an underlying where the distribution of DAT holdings isn’t as extremely skewed toward one mega holder. If there is a small handful of major DATs for a single underlying, then this becomes a Prisoner Dilemma coordination game where the good outcome is possible to some extent. At .9 or .95 mNAV, it is conceivable that none of the players go for the arb. Even without outright coordination, they could all choose to (3,3). Now suppose mNAV drops to .5 as an extreme example. Now the arb profits are much bigger and could outweigh the negative consequences of underlying market cap compression, reflexive selling effects, and reputational considerations. So we can see that whether there is an underlying unwind is dependent on a whole host of factors including how many large players are running DATs on that underlying. In other words, the gain in arb value is individual while the compression of the underlying market cap and hence all DAT market caps for the same underlying is socialized. All else equal, more big DATs is worse than fewer big DATs for this game.

As a tangent, I’m roughly assuming above that most DATs for the same underlying have similar mNAVs. If this wasn’t the case, we could see 1) different levels of incentives to do the arb and 2) one DAT buying another DATs equity. An exercise left to the reader.

Now let’s introduce more complexity into this toy model. Each manager of a DAT for the same underlying has a different propensity to take the arb. It depends how crypto native vs tradfi native the manager is. Crypto natives don’t want the music to slow. For tradfi natives, well, whoever sells first sells best. Also there are reputational considerations. Whoever is more prominent has more personal considerations outside of managing the DAT. These considerations could push up or down the threshold for where arbs will be taken.

Galois Kevin@Galois_Capital

It’s getting late in the DAT cycle. Time for a healthy unwind then we resume up only.

English