تغريدة مثبتة

What took decades to build shouldn't have to change in weeks.

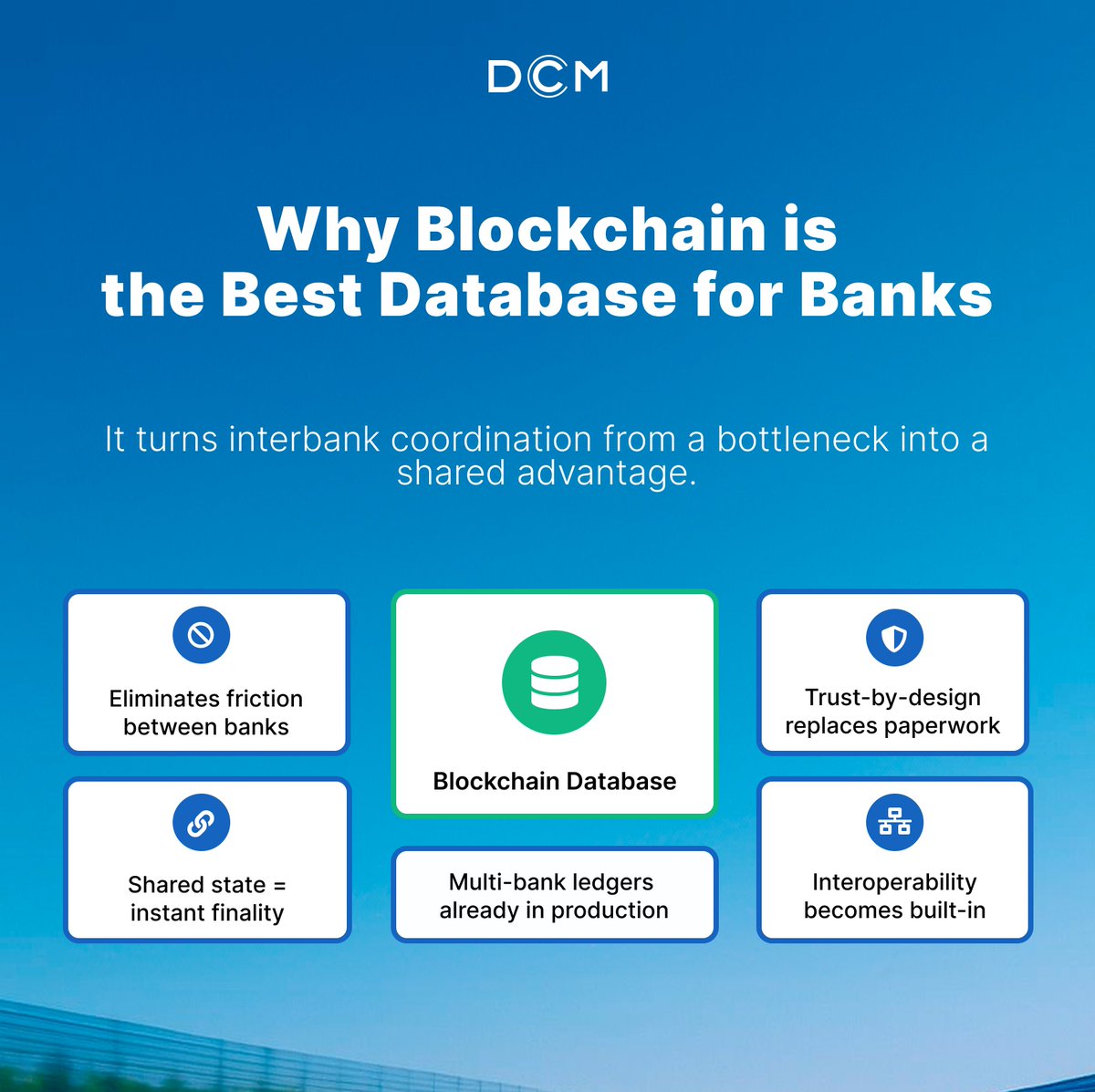

Core banking systems hold more than account balances. They hold the rules, controls, and processes that keep banks running reliably — day after day, under any pressure.

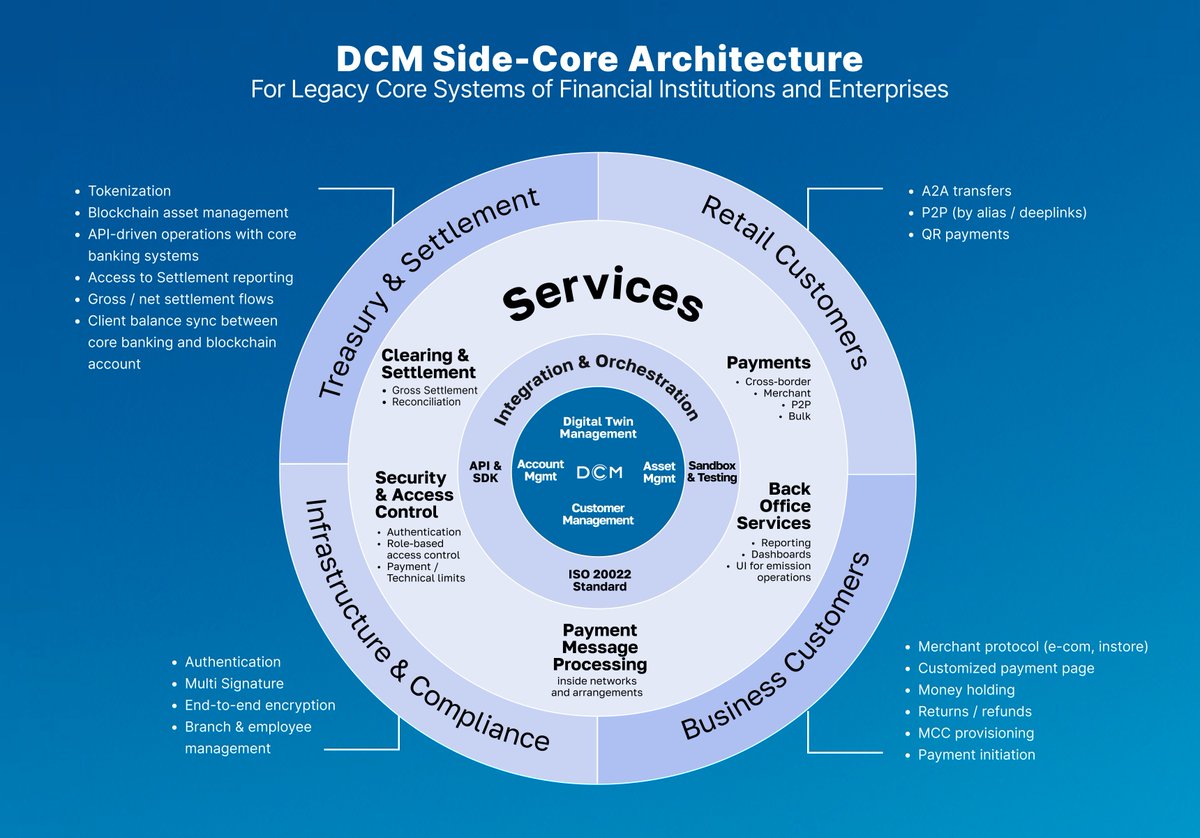

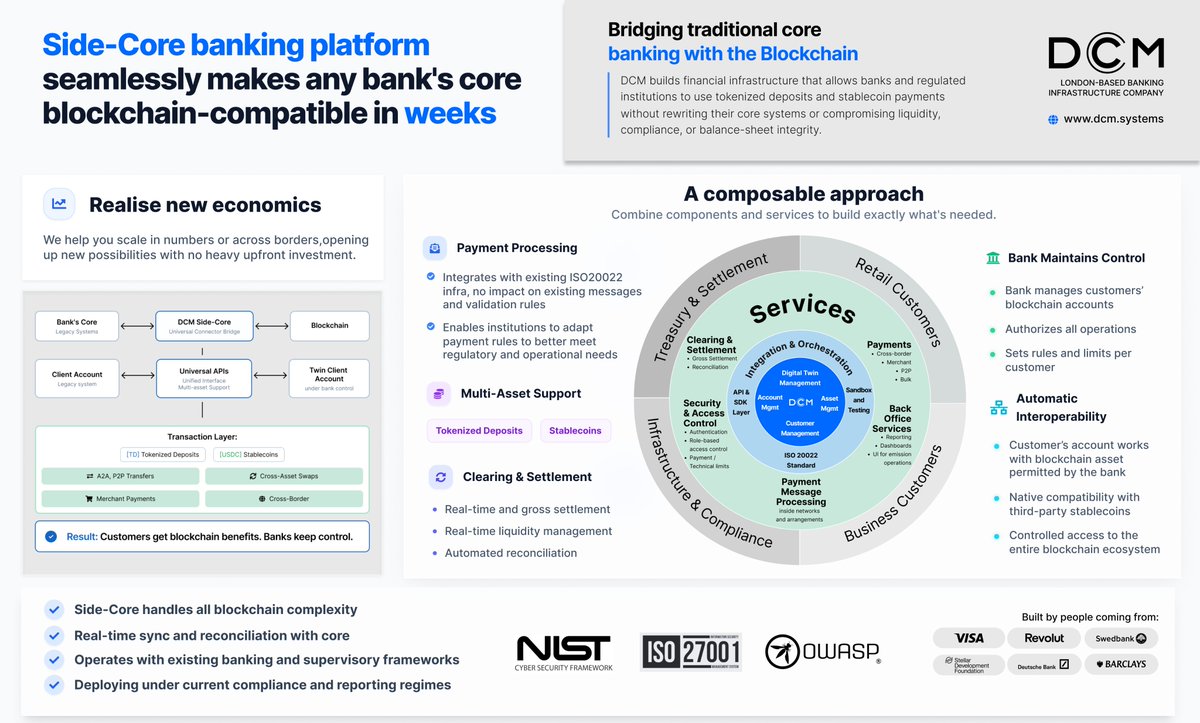

@dcm_systems developed a side-core platform that strengthens that foundation.

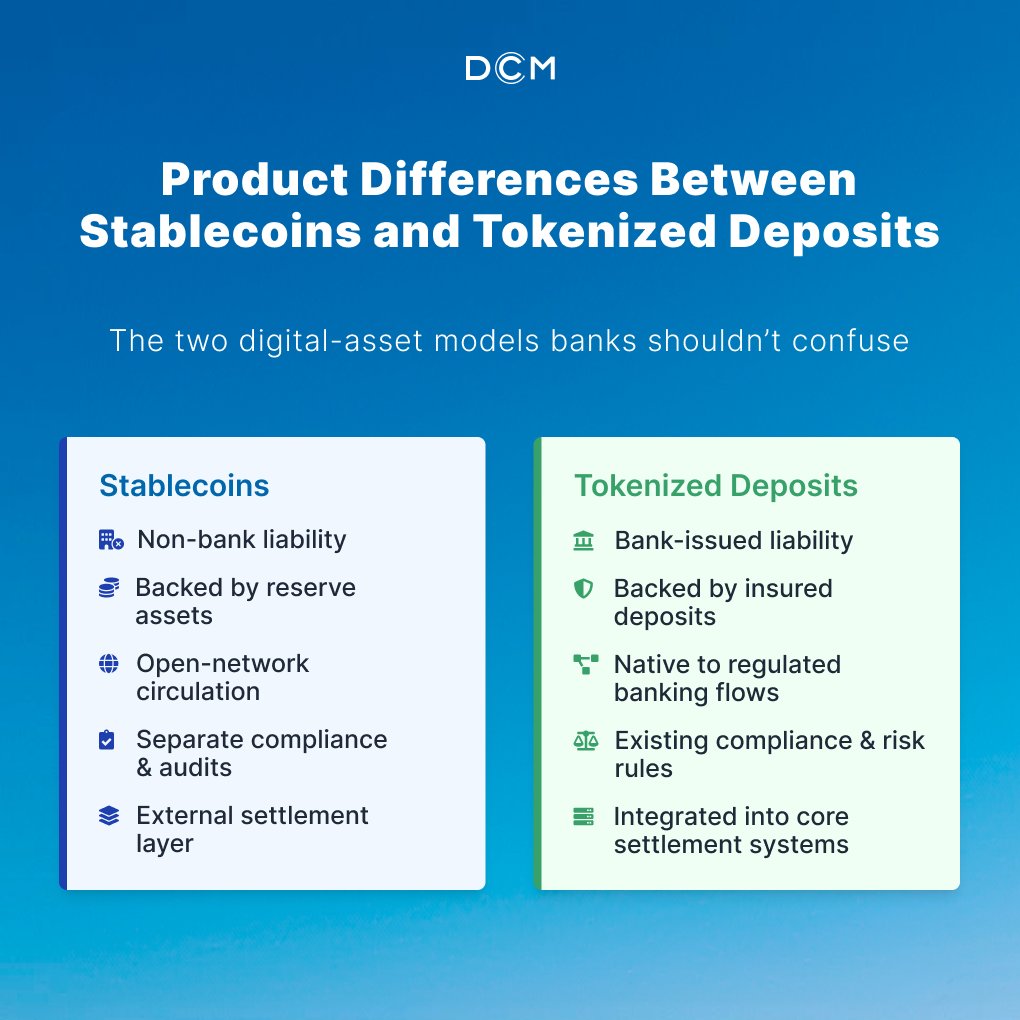

It sits alongside the existing bank core, keeps all records in place, and layers new capabilities on top: real-time settlement, easy connections between institutions, and blockchain execution where it actually makes sense — all within the operating standards banks already follow.

Integration takes weeks, not years. The core stays untouched. The bank just gets a new gear.

Learn more on our website - dcm.systems

Or ask our AI any question you have - ai.dcm.systems

English