@Biotech2k1 Lack of guidance also makes possibilities for those believe in the company and in the story. Because of the lack of guidance, analysts have been wrong many hundred % on quarterly reports.

English

Siika aka "Fisu"

336 posts

Evolution $EVO will pay no dividend in 2026 which paves the way for a big share buyback program 👌

#Diamyd Medical’s pivotal Phase 3 Type 1 Diabetes trial clears last safety review ahead of early readout in March 2026 diamyd.com/docs/pressClip…

$ROOT is the leading AI insurance company. ”As a company whose founding principles lie at the heart of AI” ”AI is not just about chatbots or RPA.”

On a GAAP basis, $LMND shows an LTM net income loss of 173.8m. But the more important question is: how much cash did $LMND actually burn? If I adjust for non cash and timing distortions: -Add back 60.1m in SBC, dilutive yes, but it does not drain the 1.06b balance sheet. -Add back 121.9m in GC synthetic agent spend, which GAAP forces them to expense immediately but not the LTV/CAC. Suddenly, the picture flips. Underlying cash flow: +8.2m. Cash tells the truth. 🍋

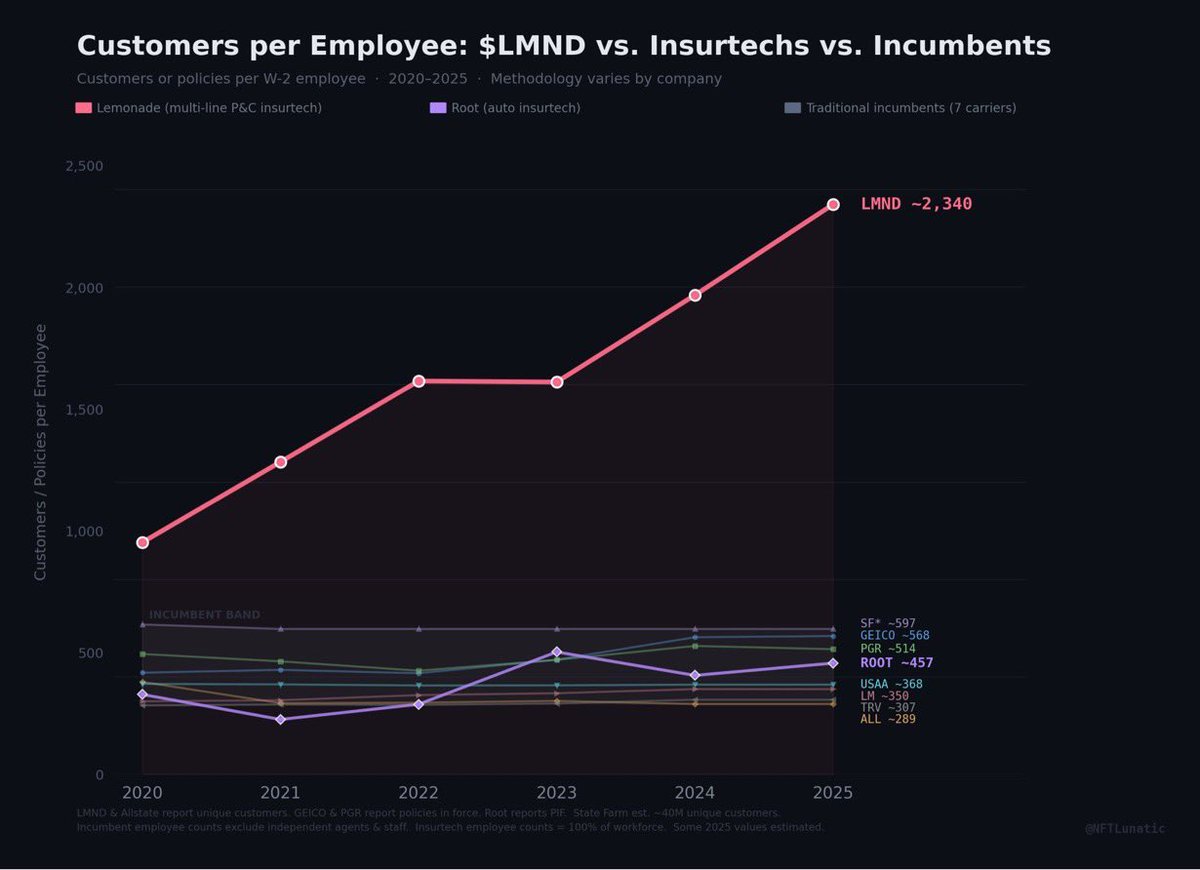

"Isn't $LMND just another insurtech?" This chart can lay that argument to rest. Customers per employee, 2020–2025: $LMND vs. $ROOT vs. 7 major incumbents. $ROOT is the perfect test case. Same era. Same "insurtech" label. Same direct-to-consumer P&C model. Public company with clean data. $ROOT at 457 customers per employee. GEICO at 568. Progressive at 514. Root IS the incumbent band. Why? $ROOT innovation was telematics — better pricing through driving data. That helped them reach profitability. But it didn't change how many humans they need to operate. Root hired 341 people last year to add 73K policies. $LMND hired 47 to add 570K. That's not a difference of degree. It's a difference of kind. $LMND didn't just digitize the front end. AI Maya underwrites. AI Jim handles claims. The marginal customer costs almost nothing to serve. $ROOT used tech to price better. $LMND used AI to run the company. That's why one curve compounds and the other flatlines. This also kills the bear argument that competitors will "just copy $LMND playbook." $ROOT has been trying for 9 years. Backed by $1.2B+ in funding. Public since 2020. Building technology from scratch with no legacy constraints. And they still ended up in the incumbent band. If a well-funded, tech-native insurtech with zero legacy baggage can't replicate this efficiency curve, what makes anyone think State Farm or Allstate will? $LMND AI-first architecture isn't a feature. It's a compound advantage that gets harder to replicate every quarter — because every new customer, claim, and interaction feeds the models that make the next one cheaper to serve. The moat isn’t JUST the AI operating system running the company. It’s 3 million customers (and growing) training the AI.