grindingmacro

2.1K posts

$MOB is laser focused imo hitting up all of the appropriate conferences. Next week in addition to Detroit, they’ll also be in Arlington, VA for Loitering Munitions USA Conference 🇺🇸

This is the only U.S. event dedicated entirely to loitering munitions programs-bringing together defense leaders, operators, & industry teams focused on deployment, integration, & mission effectiveness.

English

@JasonL_Capital All great names, I love $AVAV

Think also some attention deserved to smaller names but great tech and still unknown such as $MTEK $MOB $PRZO

English

The President is telling you exactly what to invest in.

He just proposed a $1.5 trillion defense budget - that's a 44% increase.

Here are 10 defense stocks that are well off their highs to take advantage of:

1. $AVAV - AeroVironment

The Switchblade is the most battle-tested loitering munition on the planet. $186M US Army order for Switchblade 600 Block 2 and Switchblade 300 under a $990M five-year IDIQ contract. Raised FY2026 revenue guidance to $1.95-2.0B. Record funded backlog of $1.1B. Q3 bookings hit $2.1B in a single quarter. New 140,000 sq ft Salt Lake City facility can produce over $2B worth of Switchblade annually. Modern warfare runs on autonomous munitions and AVAV owns the category.

English

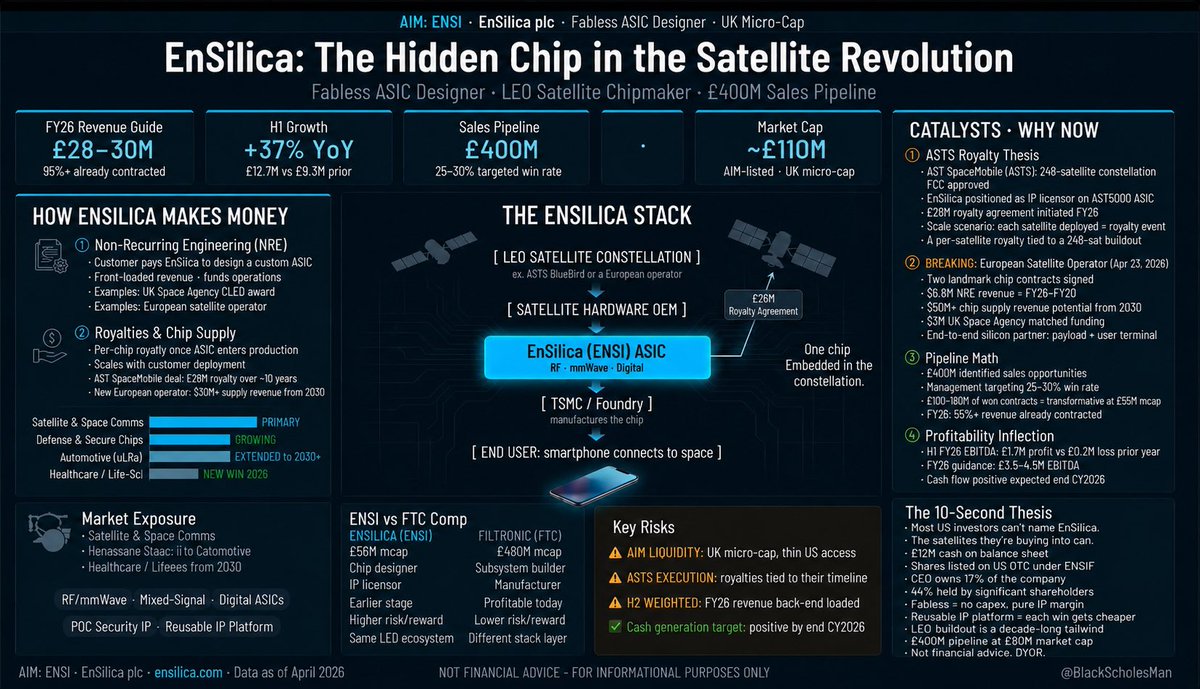

#ENSI $ENSI $ENSIF

Now over the £100m mark. Is this now where certain institutions are able to buy the stock

English

@Lee_Trades $ENSI may be the next multibagger in this space I think?

English

A small UK company is involved in this.🧐

AST SpaceMobile@AST_SpaceMobile

Announcement: Mid-June launch of three Bluebird satellites aboard a Falcon 9 rocket.🚀🚀🚀🚀🚀🚀🚀🚀🚀🚀 32 next-generation satellites at advanced stages of assembly to be ready for launch. Network deployment with a launch every one to two months on average. Space-based cellular broadband. Built in Texas. 🌎📶📱 #ASTSpaceMobile #Broadband #ConnectingtheUnconnected #BlueBirds

English

$SLNH No big deal, just negotiating with hyper scalers 😴 👀

John Belizaire@jbelizaireCEO

Our Monthly Business Update is out ... Project updates from $SLNH's 600+ MW AI/HPC development pipeline 🧵... Kati 2 (300+ MW) ✅ Award-winning architect & engineering firms selected via competitive RFP ✅ Hyperscaler & neocloud diligence active — more parties joining ✅ Geotech complete ✅ Tax abatement process kicked off ✅ Construction RFP drafting underway ✅ Initial gas engine negotiations in motion Dorothy 3 (300+ MW) ✅ Add-on 50 MW interconnection load study with Goldenspread Electric Co-op & ONCOR ✅ ~400 acres under LOI, purchase agreement expected to close in the coming weeks ✅ Fiber studies underway with leading providers ✅ Community relations task force starting in Briscoe County. Full update in our latest business release 👉 solunacomputing.com/news/monthly-u… AI infrastructure starts with power, land, fiber, and trust. We’re putting those pieces in place. We keep pushin’. $SLNH @SolunaHoldings

English

@jbelizaireCEO It looks quite positive. Keep the good work.

English

Our Monthly Business Update is out ...

Project updates from $SLNH's 600+ MW AI/HPC development pipeline 🧵...

Kati 2 (300+ MW)

✅ Award-winning architect & engineering firms selected via competitive RFP

✅ Hyperscaler & neocloud diligence active — more parties joining

✅ Geotech complete

✅ Tax abatement process kicked off

✅ Construction RFP drafting underway

✅ Initial gas engine negotiations in motion

Dorothy 3 (300+ MW)

✅ Add-on 50 MW interconnection load study with Goldenspread Electric Co-op & ONCOR

✅ ~400 acres under LOI, purchase agreement expected to close in the coming weeks

✅ Fiber studies underway with leading providers

✅ Community relations task force starting in Briscoe County.

Full update in our latest business release 👉 solunacomputing.com/news/monthly-u…

AI infrastructure starts with power, land, fiber, and trust.

We’re putting those pieces in place.

We keep pushin’.

$SLNH @SolunaHoldings

English

@xGuineapig Think the Swedish defense/space ecosystem is quite well prepared to join the top

English

"Svenska företag är för första gången med i Natos innovationsprogram Diana" 👀 #APRTEC valdes ut bland 2600 ansökande bolag för sin innovativa kylteknik 👍 Trigger i närtid är en "förväntad" order från "globalt techbolag, de bygger för massproduktion.

regeringen.se/pressmeddeland…

Svenska

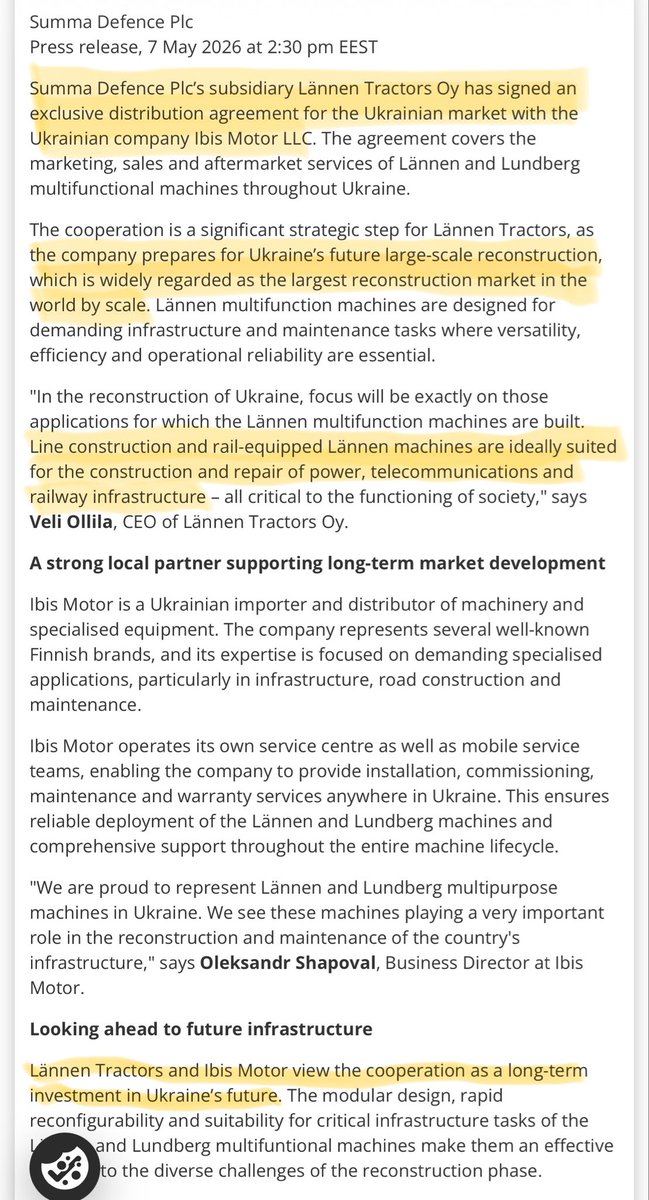

Finnish $SUMMA preparing to scale in Ukraine reconstruction market — which is estimated at $600 billion — through its tractor product, which recently received a €35 million order from an European NATO member state. Quite great news for this small but growing company.

English

@grindingmacro $SUMMA getting even more integrated with Ukraine. This time to capitalise on post-war construction ($600B market).

news.cision.com/summa-defence-…

English

Someone knows something... $SUMMA Defense suddenly up 10%.

English

🚗 The LiDAR runway is becoming clearer based on the Q1 results from $OUST and $AEVA.

Aeva’s gross margin is difficult to predict because product margin came in at -78%. The company is receiving NRE payments but is spending nearly five times its revenue.

Many FMCW companies are small and either on the verge of bankruptcy or already bankrupt—for example, the one acquired by $MVIS, which seems unable to develop its own technology and instead collects distressed assets.

⚙️ FMCW is complex, expensive, and mostly unnecessary. The biggest LiDAR companies in the world (Chinese) do not use it for a reason. In any case, the only name that still has meaningful presence is $INVZ, which reports next week. Meanwhile, analysts have raised revenue expectations for $OUST to:

📈 2026: $223M

📈 2027: $300M

📈 2028: $432M

Ouster also has a DF (Digital Flash) sensor in development for the automotive segment. It does not use mirrors or polygon prisms like Atlas from Aeva or InnovizTwo; it is fully CMOS/silicon true solid-state.

Last year, Aeva sold more sensors than Innoviz, but Innoviz generated substantial NRE revenue. It appears that $AEVA sold fewer sensors in Q1 2026, so it will be interesting to see whether Innoviz can show improvement here or whether it is still riding NRE tailwinds.

💰 Ouster will likely become profitable in Q2 2027, with 2028 being a full year of profitability.

Note, cash for AEVA includes its preferred facility ($124M debt) that will eventually be drawn, in addition to the $96M in debt already on the balance sheet. With negative equity, Aeva’s financial picture increasingly resembles bankrupt Luminar—whose bits and pieces are part of MicroVision.

English

@evanhill Importance of space AI-at-edge for timely assessment/information became a must-have in nowadays arsenal. $Unibap

English

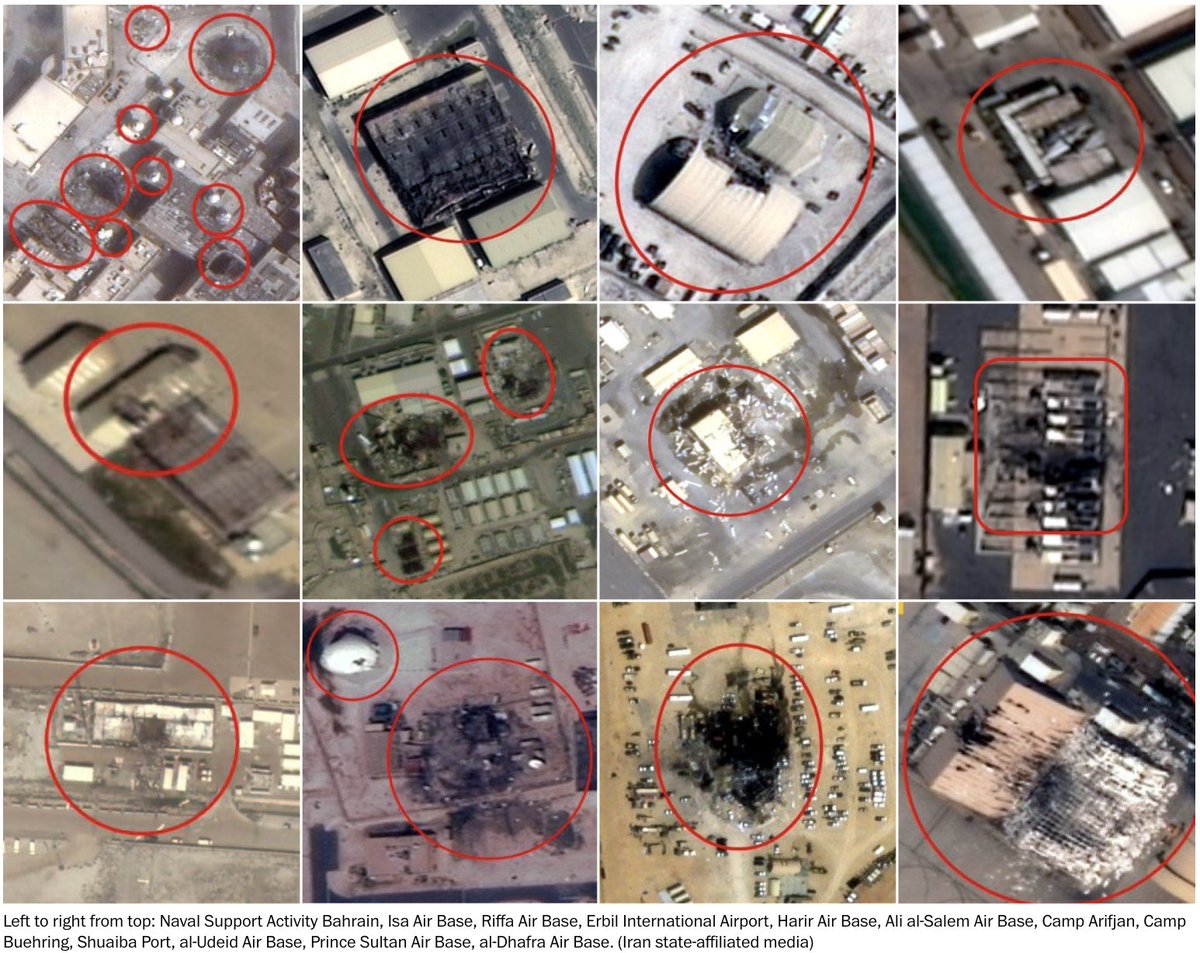

New: A Washington Post satellite imagery review reveals that Iran has caused far more damage to US military sites than previously reported.

Amid a US imagery blackout, Iran has released more than 100 images of strikes on US bases.

We analyzed them: washingtonpost.com/investigations…

English

At the current run rate, @ousterlidar is on track for $1B revenue in 2030—even before factoring in customers scaling or DF SOP in 2028. $OUST growth is faster than it appears.

Profitability in 2027, per the CFO.

jimmyrunsmoney@jimmyrunsmoney

When I was younger, I would get impatient with my stocks, larping as a trader when I should have DCA’d and held on instead. I graduated from college in 2008 with no capital to start, but think of the generational entries then. $OUST is a promising young company still earning only ~50M in revenues quarterly. We all want a 10x, but most get off the train after 50% or a double and lose focus. For those who have done the DD, this company has a long and potentially prosperous path ahead. I can see them at over $1B/qtr revenue run rate some day. DCA little by little- they’ll be in the S&P500 in the next decade

English

Scandinavian Astor Group $ASTOR: Q1'26 revenue SEK 130M — the 2nd highest quarter on record (74% growth LTM). Order backlog roughly 3× where it was three years ago, profit margin doubled to a record 21%, SEK 248M of cash with zero net debt. The Nordic rearmament theme is real 🇸🇪

English

@LeaderInvests Not my sector, but I bought here— think it will do quite well in this environment

English

$SLNH - Doesn't look bearish to me.

Holding the daily golden trend - 8 EMA and Blue Diamonds with increasing Whale Flow.

Give it time. 🔷🔷🔷

TheGentleTraveler@LeaderInvests

$SLNH structure looks similar to $DGXX. So $SLNH landing a deal or catalyst this / next week would be fun. Would send it to $3.50 quite fast. Again, $SLNH is a volatille name. Embrace it. Weekly outlook is 🔷🔷🔷 + Whale Flow coming in, that's what I'm watching

English

@BryzonX $OSS is a great company; I really like their israeli partner $MTEK which recently won a production order from tier1 loitering munition producer— worth checking out

English

@PeakGrowthRes @MegatrendGlobal $OSS is a great company; I really like their israeli partner $MTEK which recently won a production order from tier1 loitering munition producer— worth checking out

English

Well said @MegatrendGlobal . I’m looking forward to Q1 results as the $OSS base case keeps improving.

Defense + edge AI + rugged compute demand are finally converging in one story:

• $65M+ lifetime P-8A awards

• Army modernization exposure

• Commercial robotics expansion

• NVIDIA ecosystem visibility via Ponto

The key now is execution and revenue conversion through 2026. If margins stabilize and growth compounds, OSS starts looking less like a niche supplier and more like a stealth defense-tech compounder.

Megatrend Investor 📈@MegatrendGlobal

Heading into the One Stop Systems $OSS Q1 earnings call this Wednesday, May 6, 2026, here is a recap of the significant operational momentum achieved throughout the quarter: 🔹U.S. Navy Powerhouse: Secured $10.5M in new awards for the P-8A Poseidon aircraft, bringing lifetime contracted revenue for this platform to over $65M. 🔹Commercial Robotics Entry: Announced a leading manufacturer of autonomous construction and mining equipment as a new customer (Built Robotics), with $2M in orders expected in 2026 and a five-year pipeline of up to $15M. 🔹U.S. Army Modernization: Received a $1.2M order to develop ruggedized integrated compute and visualization systems for combat vehicles like the Stryker and Bradley (Second Big Situational Awareness Project). 🔹Aerospace Connectivity: Landed a $1.1M initial order for ruggedized Ethernet switches to support next-gen in-flight entertainment systems. Key Considerations on Revenue Timing: While these wins are substantial, the exact quarterly timing for revenue recognition remains variable. Notably, the P-8A Poseidon awards are expected to contribute to revenue throughout 2026 and continue well into 2027. NVIDIA GTC Highlight: $OSS recently showcased Ponto, their ultra-dense PCIe Gen5 expansion system, at NVIDIA GTC. In their recap, the company highlighted Ponto as a strategic solution for commercial data center operators to scale compute power without the massive capital expenditure of buying additional DRAM. This is a critical advantage given current high memory prices.

English

@InvestWithTimmy $OSS is a great company; I really like their israeli partner $MTEK which recently won a production order from tier1 loitering munition producer— worth checking out

English

$OSS is up +16% in the pre-market after very good earnings.

This company is in my opinion under the radar of many investors.

One Stop Systems is making portable computers that can perform like small data centers in extreme conditions. Their computers include Nvidia AI chips, giving them a lot of compute power.

Customer concentration in defense is the main risk here but if OSS keeps delivering there should be no problem with that.

TopSecretStocks 🤫@topsecretstocks

$OSS 🟢 +16% in Pre-Market 👇 $OSS Q1 2026 Earnings $OSS delivered a standout quarter, with the top line coming in well ahead of estimates. Revenue surged 55% YoY to $8.1M, with gross margin expanding 610 bps to 51.6%, a clear sign of mix improvement and operational leverage. What drove the growth? • Higher sales of data storage products to a defense prime customer for the P-8A program, increased liquid-cooled server sales to a medical imaging OEM, and new customer-funded development revenue for prototype combat vehicle compute systems were the key contributors. The revenue mix shift toward higher-margin defense and development work directly explains the gross margin expansion. Bookings are the real headline • $OSS recorded nearly $15M in bookings in Q1, described by management as one of the strongest quarters in company history, producing a book-to-bill of 1.8x and supporting a TTM book-to-bill above 1.2x. A 1.8x book-to-bill means $OSS is building backlog significantly faster than it's burning it. That's a powerful leading indicator. Cash generation turned a corner • Operating cash flow from continuing operations was $4.0M, compared to cash burn of $1.5M in Q1'25, a $5.5M swing YoY. Management called it record free cash flow from continuing operations. Profitability is inflecting • GAAP net loss narrowed dramatically to $(0.4)M vs. $(2.3)M a year ago. On a non-GAAP basis, OSS flipped to $0.3M net income and $0.2M adjusted EBITDA, compared to an adjusted EBITDA loss of $(1.6)M in Q1'25. The company is approaching breakeven on a clean basis. OpEx discipline holding • Total operating expenses grew only 2.5% YoY to $4.8M, with higher G&A partially offset by lower R&D and selling expenses. Revenue grew 55% while opex grew 2.5%, that's the kind of operating leverage that changes a business model. Balance sheet remains solid • Cash, equivalents, and short-term investments stood at $34.4M, with working capital of $44.7M. No debt concerns here. FY 2026 Guidance confirmed • Revenue growth of +20% to +25%, gross margin ~40% (note: step-down from Q1's 51.6% due to mix normalization), and positive EBITDA for the full year. The Q1 gross margin was unusually elevated, the FY guidance of ~40% suggests the development program mix won't hold at this level all year, which is expected. 👉 Bottom line: $OSS is executing cleanly on its pivot to a pure-play rugged AI compute business. The bookings strength, cash flow inflection, and near-breakeven profitability all point to a company entering a new phase. The key risk remains customer concentration in defense, but for now, demand is clearly accelerating. Long $OSS Congrats to all Investors 🥳

English