முகில்நிழல்

1.2K posts

பெரும்பான்மையை நிரூபிக்க வேண்டிய நேரத்தில் CVS - SPV ஆதரவு மிக முக்கியமான நகர்வு.

இந்த இடத்தில் திமுக கூட்டணி கட்சிகளை Expose செய்து அவர்களை பொருளற்றவர்களாக ஆக்கிவிட்டார்..கூட்டணி கட்சிகள் இனி முதல்வர் விஜய் அவர்களின் கருணைப் பார்வைக்கு தவமிருக்கலாமே ஒழிய தவெகவின் கையை முறுக்க முடியாது..விஜய் எப்படி எதையும் மறக்க மாட்டார் என்பதற்கு உதாரணமாக திருமா அன்று செய்ததைப் போலவே இன்று கடைசியாகப் போய் அவரை பார்த்துள்ளார்.இது ஒரு அரசியல் செய்தியாகவே உள்ளது.

முதல்வர் விஜய் எல்லா தலைவர்களையும் சென்று பார்ப்பதன் வழியே அவரை வெறுப்பவர்களைக் கூட ஒரு மென் போக்கிற்கு வலுலக்கட்டாயமாக நகர்த்துகிறார்..இதில் எதிர்க்கட்சிகள் எல்லாம் பலத்தை இழக்கின்றனவே ஒழிய அவர்களுக்கு இதில் பெரிய லாபமில்லை..பார்த்தாயா எங்கள் அண்ணனின் மாண்பை என அவரது ஆதரவாளர்களின் பலமான கருத்துருவாக்கமாக என்றும் இது நிற்கப் போகிறது.

தன்னை நிலைநிறுத்திக் கொள்ளும் வரை தன்னை வெளிக்காட்டுவதில் விஜய் காட்டும் பொறுமை உண்மையிலேயே ஆச்சர்யமாக உள்ளது.விஜய், தன்னை கணிக்க முடியாத இடத்திற்கு எல்லோரையுமே தள்ளுகிறார் இது அவரது வெற்றிக்கு மிக முக்கியமான காரணம்..ஆனால் ஒரு மாநில முதல்வராக எதிர்காலத்தில் இவை சவாலானது..பார்ப்போம்.

தமிழ்

காமராஜை டிடிவி கட்சியை விட்டு தூக்கின மாதிரி, EPS ஏன் இன்னமும் அந்த 28-30 பேரை இன்னமும் தூக்கலை?

குறைஞ்சது CVS, SPV, விஜயபாஸ்கர் இவங்க மூணு பேரையாவது தூக்கியிருக்கலாமே. ஏன் இன்னமும் அப்படி பண்ணலை?

தமிழ்

Thalaiva ne pota kannaku apdiye nadukuthu 😭

Pradip Varma@Pradip_K_Varma

CVS announces support to TVK.👍

@taiganeon @labstamil @A_n_b_e_S_i_vam youtube.com/watch?v=xqjy-C… Vintage Talkies has most of his dramas.

YouTube

English

Genuine doubt.

What is their Source of Income?

What was his Dad's Net Worth before Politics?

I've seen Old Ramadoss Videos..

Used to be a Simple Man bashing RSS left Right.

How many salary does an MP get?

ANI@ANI

#WATCH | Tamil Nadu CM Vijay meets PMK President Anbumani Ramadoss at his Akkarai residence in Chennai. (Source: PMK)

English

English

@labstamil @A_n_b_e_S_i_vam Yes, probably because videos are from 90's. He is blasting Jaya as CM 🙂. From 2001, he toned it down after Amma said his criticism hurt her the most.

English

@mydaymywin It won't be brought as laws. Can all companies make employees can easily work from home? Which IT companies need physical presence?

English

IT Companies resisting work from home must be moved to bad behavior book and be applied 10%

Work from office Tax... which we can use to buy fuel

Tokugawa Iyeyasu@mydaymywin

Good work. Its time force these non compliant companies.

English

முகில்நிழல் retweetet

@hsinha1445 A mutual fund scaled their position to almost 9% ownership in two of them in a span of 6 months

English

Why India is sleeping on REITs.

India has 5 listed REITs. Most retail portfolios own zero of them.

Seven years after Embassy's IPO, the asset class is still treated like a footnote. Let me lay out why that's a mistake.

What a REIT actually is

A SEBI-regulated trust that owns income-producing commercial real estate — offices and malls. By law, it must distribute 90% of its rental income to unit-holders every quarter. You buy it on the NSE like any equity.

The five listed:

• Embassy (2019) — office

• Mindspace (2020) — office

• Brookfield (2021) — office

• Nexus Select Trust (2023) — retail malls

• Knowledge Realty Trust (2025) — office

That's the entire universe. ~₹2 lakh crore total market cap. Versus the US, where REITs are a $1.4 trillion asset class.

Equity in trading and taxation. Debt in payouts. Real estate underneath. One ticker, three asset characteristics.

Performance vs Nifty 500 TRI and 10y G-Sec — period-matched

Each REIT measured over its own listed window, against Nifty 500 TRI and the 10-year Gilt over the SAME window:

• Embassy (7.1y): Nifty 500 14.0% > Embassy 10.8% > 10y G-Sec 6.8%

• Mindspace (5.7y): Nifty 500 18.3% > Mindspace 13.8% > 10y G-Sec 5.1%

• Brookfield (5.2y): Nifty 500 13.1% > Brookfield 10.5% > 10y G-Sec 5.4%

• Nexus Select (3.0y): Nexus 21.3% > Nifty 500 15.3% > 10y G-Sec 6.1%

For context — buying a flat in India without a loan and renting it out has returned ~6.4% a year over the past 7 years (BIS Housing Price Index + ~2.5% gross rental yield, unlevered).

G-Secs are obviously the safest of the three — sovereign-guaranteed, near-zero credit risk. Lower returns are the price for that safety.

Three of four REITs trailed equity over their full windows. Only Nexus beat. All four comfortably beat fixed income; all five comfortably beat unlevered residential real estate.

Risk-adjusted returns (Sharpe) tell the same story — Nifty 500 edges out 3 of the 4 REITs with enough history.

The pitch isn't total return. It's everything below.

The cash yield is the silent hammer

Pre-tax yield comparison:

• REITs (TTM, 4 mature): ~6.7%

• Nifty 500 dividend yield: 1.13%

• 10-year G-Sec yield: ~6.5%

• Bank FD: ~7%

REITs yield roughly 5x what the Nifty 500 pays in dividends — and competitive with G-Sec / FD, but with equity-like upside on the underlying real estate.

The cash arrives quarterly. Predictable. Contracted at the lease level (most leases have 5-15% rent escalations every 3 years).

Diversification — REITs are a third asset

Average 3-year monthly correlations:

• REIT ↔ Nifty 500 TRI: 0.21

• REIT ↔ AAA bonds: 0.27

Anything below 0.4 is a weak relationship; above 0.7 means the assets move together.

For context: Nifty 50 ↔ Nifty 500 is 0.97. The 20-year correlation between Nifty 500 and 10y Gilt is 0.08 — but it's risen to 0.51 in the latest 5-year window because both got hit in the rate-hike cycle.

REITs at 0.21 with equity offer better diversification than bonds do in the current regime.

Access — REITs are the only door under ₹5 Cr

Commercial real estate yields meaningfully more than residential. But a single Grade-A office unit starts at ₹2-5 Cr.

If you have under ₹5 Cr to allocate to property, REITs are pretty much the only way to participate in commercial real estate. Diversified across 20-50+ buildings, multiple cities, dozens of MNC tenants. One click, ~₹400 per unit.

NAV — the part most people don't understand

Like an ETF, a REIT has two prices:

→ NAV — what an independent SEBI-registered valuer says the underlying real estate is actually worth. Formula: (Building values − Debt + Cash) ÷ Units outstanding. Refreshed only twice a year — every March 31 and September 30 (a SEBI mandate, not a company choice).

→ Market price — what buyers and sellers settle at on NSE, second by second.

For a normal ETF, arbitrage keeps the two glued together within paise. For a REIT, NAV updates twice a year, so market price drifts in between based on what investors think the next NAV will look like.

Right now, every mature REIT trades below its audited NAV:

• Embassy: -14.5% (₹491.62 NAV vs ₹420 traded)

• Mindspace: -10.7% (₹527 vs ₹470)

• Brookfield: -6.4% (₹349 vs ₹327)

• Nexus Select: -1.0% (₹159 vs ₹157)

Average: ~8% below independently audited fair value.

Why the persistent discount? Three forces:

(a) Investors demand higher cap rates than valuers. Embassy's March 2026 valuation used 7.5-8.25% cap rates. The market is pricing closer to 8.5-9% — wanting a bigger margin of safety given WFH risk and ~30% US tenant exposure.

(b) Big early backers are still selling. Blackstone exited Embassy through 2023-24. More supply than demand pushes prices down.

(c) REITs trade in equity portfolios. When broader markets fall, REITs get sold along with them — even when the buildings themselves are doing fine.

At today's prices, you're paying ~92 paise on the rupee for institutional-grade Grade-A real estate.

Tax math — better than equity on income, equal on capital gains

Capital gains taxation (post Budget 2024) — identical to listed equity

Where REITs win is on income. Distribution arrives in three components, taxed differently:

→ Interest (loan from REIT trust to SPVs, returning) — taxed at your slab rate

→ Dividend (from SPVs) — tax-free

→ Capital repayment (loan principal returning) — Why India is sleeping on REITs

India has 5 listed REITs. Most retail portfolios own zero of them.

Seven years after Embassy's IPO, the asset class is still treated like a footnote. Let me lay out why that's a mistake.

What a REIT actually is

A SEBI-regulated trust that owns income-producing commercial real estate — offices and malls. By law, it must distribute 90% of its rental income to unit-holders every quarter. You buy it on NSE like any equity.

The five listed:

• Embassy (2019) — office

• Mindspace (2020) — office

• Brookfield (2021) — office

• Nexus Select Trust (2023) — retail malls

• Knowledge Realty Trust (2025) — office

That's the entire universe. ~₹2 lakh crore total market cap. Versus the US, where REITs are a $1.4 trillion asset class.

Equity in trading and taxation. Debt in payouts. Real estate underneath. One ticker, three asset characteristics.

Performance vs Nifty 500 TRI and 10y G-Sec — period-matched

Each REIT measured over its own listed window, against Nifty 500 TRI and the 10-year Gilt over the SAME window:

• Embassy (7.1y): Nifty 500 14.0% > Embassy 10.8% > 10y G-Sec 6.8%

• Mindspace (5.7y): Nifty 500 18.3% > Mindspace 13.8% > 10y G-Sec 5.1%

• Brookfield (5.2y): Nifty 500 13.1% > Brookfield 10.5% > 10y G-Sec 5.4%

• Nexus Select (3.0y): Nexus 21.3% > Nifty 500 15.3% > 10y G-Sec 6.1%

For context — buying a flat in India without a loan and renting it out has returned ~6.4% a year over the past 7 years (BIS Housing Price Index + ~2.5% gross rental yield, unlevered).

G-Secs are obviously the safest of the three — sovereign-guaranteed, near-zero credit risk. Lower returns are the price for that safety.

Three of four REITs trailed equity over their full windows. Only Nexus beat. All four comfortably beat fixed income; all five comfortably beat unlevered residential real estate.

Risk-adjusted returns (Sharpe) tell the same story — Nifty 500 edges out 3 of the 4 REITs with enough history.

The pitch isn't total return. It's everything below.

The cash yield is the silent hammer

Pre-tax yield comparison:

• REITs (TTM, 4 mature): ~6.7%

• Nifty 500 dividend yield: 1.13%

• 10-year G-Sec yield: ~6.5%

• Bank FD: ~7%

REITs yield roughly 5x what the Nifty 500 pays in dividends — and competitive with G-Sec / FD, but with equity-like upside on the underlying real estate.

The cash arrives quarterly. Predictable. Contracted at the lease level (most leases have 5-15% rent escalations every 3 years).

Diversification — REITs are a third asset

Average 3-year monthly correlations:

• REIT ↔ Nifty 500 TRI: 0.21

• REIT ↔ AAA bonds: 0.27

Anything below 0.4 is a weak relationship; above 0.7 means the assets move together.

For context: Nifty 50 ↔ Nifty 500 is 0.97. The 20-year correlation between Nifty 500 and 10y Gilt is 0.08 — but it's risen to 0.51 in the latest 5-year window because both got hit in the rate-hike cycle.

REITs at 0.21 with equity offer better diversification than bonds do in the current regime.

Access — REITs are the only door under ₹5 Cr

Commercial real estate yields meaningfully more than residential. But a single Grade-A office unit starts at ₹2-5 Cr.

If you have under ₹5 Cr to allocate to property, REITs are pretty much the only way to participate in commercial real estate. Diversified across 20-50+ buildings, multiple cities, dozens of MNC tenants. One click, ~₹400 per unit.

NAV — the part most people don't understand

Like an ETF, a REIT has two prices:

→ NAV — what an independent SEBI-registered valuer says the underlying real estate is actually worth. Formula: (Building values − Debt + Cash) ÷ Units outstanding. Refreshed only twice a year — every March 31 and September 30 (a SEBI mandate, not a company choice).

→ Market price — what buyers and sellers settle at on NSE, second by second.

For a normal ETF, arbitrage keeps the two glued together within paise. For a REIT, NAV updates twice a year, so market price drifts in between based on what investors think the next NAV will look like.

Right now, every mature REIT trades below its audited NAV:

• Embassy: -14.5% (₹491.62 NAV vs ₹420 traded)

• Mindspace: -10.7% (₹527 vs ₹470)

• Brookfield: -6.4% (₹349 vs ₹327)

• Nexus Select: -1.0% (₹159 vs ₹157)

Average: ~8% below independently audited fair value.

Why the persistent discount? Three forces:

(a) Investors demand higher cap rates than valuers. Embassy's March 2026 valuation used 7.5-8.25% cap rates. The market is pricing closer to 8.5-9% — wanting a bigger margin of safety given WFH risk and ~30% US tenant exposure.

(b) Big early backers are still selling. Blackstone exited Embassy through 2023-24. More supply than demand pushes prices down.

(c) REITs trade in equity portfolios. When broader markets fall, REITs get sold along with them — even when the buildings themselves are doing fine.

At today's prices, you're paying ~92 paise on the rupee for institutional-grade Grade-A real estate.

Tax math — Identical to listed equity.

→ Interest (loan from REIT trust to SPVs, returning) — taxed at your slab rate

→ Dividend (from SPVs) — tax-free

→ Capital repayment (loan principal returning) — not taxed today. You pay capital gains tax (at the lower LTCG rate) whenever you eventually sell.

Net post-tax yield for a 30%-slab investor: roughly 5.5% on a 6.7% pre-tax distribution yield. An FD at 7% yields 4.9% post-tax. The math isn't close.

The inflation question

30 years of US data, average calendar-year return when CPI > 3%:

• Gold: +9.5%

• REITs: +9.0%

• Bonds: +6.3%

• S&P 500: +1.7%

REITs come in a close second to gold as an inflation hedge — and both decisively beat equity and bonds. The "real assets" thesis (rents escalate with CPI, replacement cost rises) plays out in the data.

If India drifts into a higher-CPI decade — likely as shelter inflation sticks — REITs are one of the few assets that handles it without bleeding.

The case against is real

→ Young — only 5 listed, oldest just 7 years of history

→ 4 of 5 are office-heavy (no warehousing, storage, or residential exposure) and ~30% of office REIT rent comes from US firms — GCC slowdown or de-globalisation policy is a tail risk

→ Bangalore-concentrated portfolios (60-75% of Embassy's GAV is in BLR alone)

→ Rate-hike sensitive — US REITs fell 26% in 2022's aggressive hiking cycle

→ Low trading liquidity (<₹40 Cr daily value for most; only Embassy is genuinely liquid)

→ No DRIP (dividend reinvestment plan) — distributions arrive as cash, manual reinvestment costs ~1-1.5pp/year of compounded TR

Bottom line

REITs trail equity in most windows. They beat fixed income comfortably. They beat unlevered residential real estate decisively. They're genuinely uncorrelated to both equity and bonds. They yield 5x the dividend cash of Nifty 500. They trade at ~8% discount to audited value. Capital gains taxed identically to equity. Distribution income mostly tax-efficient. They're a competitive inflation hedge — second only to gold.

The case to ignore them entirely is harder than the case to own them. Even at a modest 5-10% portfolio sleeve.

Net post-tax yield for a 30%-slab investor: roughly 5.5% on a 6.7% pre-tax distribution yield. An FD at 7% yields 4.9% post-tax. The math isn't close.

The inflation question

30 years of US data, average calendar-year return when CPI > 3%:

• Gold: +9.5%

• REITs: +9.0%

• Bonds: +6.3%

• S&P 500: +1.7%

REITs come in a close second to gold as an inflation hedge — and both decisively beat equity and bonds. The "real assets" thesis (rents escalate with CPI, replacement cost rises) plays out in the data.

If India drifts into a higher-CPI decade — likely as shelter inflation sticks — REITs are one of the few assets that handles it without bleeding.

The case against is real

→ Young — only 5 listed, oldest just 7 years of history

→ 4 of 5 are office-heavy (no warehousing, storage, or residential exposure) and ~30% of office REIT rent comes from US firms — GCC slowdown or de-globalisation policy is a tail risk

→ Bangalore-concentrated portfolios (60-75% of Embassy's GAV is in BLR alone)

→ Rate-hike sensitive — US REITs fell 26% in 2022's aggressive hiking cycle

→ Low trading liquidity (<₹40 Cr daily value for most; only Embassy is genuinely liquid)

→ No DRIP (dividend reinvestment plan) — distributions arrive as cash, manual reinvestment costs ~1-1.5pp/year of compounded TR

Bottom line

REITs trail equity in most windows. They beat fixed income comfortably. They beat unlevered residential real estate decisively. They're genuinely uncorrelated to both equity and bonds. They yield 5x the dividend cash of Nifty 500. They trade at ~8% discount to audited value. Capital gains taxed identically to equity. Distribution income mostly tax-efficient. They're a competitive inflation hedge — second only to gold.

The case to ignore them entirely is harder than the case to own them. Even at a modest 5-10% portfolio sleeve.

English

Among actively managed mid cap mutual funds:

> 50% funds failed to beat the index.

> 70% funds failed to generate even 1% alpha over the index.

English

முகில்நிழல் retweetet

@joybharali81 @ThetaVegaCap Small cap funds have great volatility

English

@taiganeon @ThetaVegaCap Any small cap fund will outperform in 5 years. Cash call in mutual fund hardly show any impcat

English

Nifty is Up 7% in april itself

Mid and Small Is also up 13-17% respectively

Parag Parikh is up by 5.75% only

Is it Due to Cash ?

#Investing #MutualFunds

English

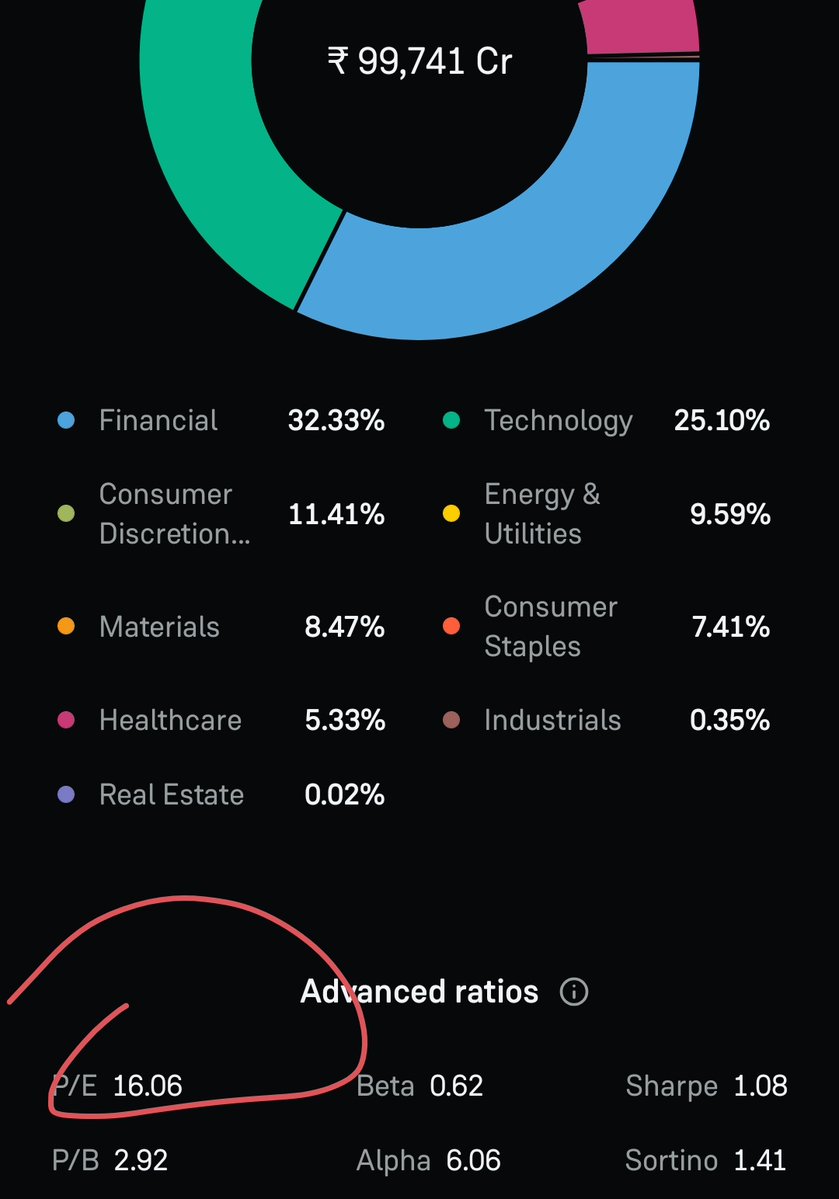

Parag Parikh Flexicap fund at PE of just 16.

You know why??

English

インド人の皆さん、日本からこんにちは🇯🇵😄

日本の夏は本当に暑いです。最高気温は40度くらいです🥵

インド人に質問があります🇮🇳🤔

インドも夏は暑いと聞きました。インドの夏の最高気温はどれくらいですか?😄

日本語

@nikitabier @doganuraldesign If you give subtitles and other cool features you can beat Youtube

English

𝕏 is one tab away from YouTube

Just launch a separate Videos tab like this:

English

Muthu potrays a rich landed zamindar, his lowly worker and an actress all living in the same house and falling in love with each other.

Because it's not about muh class or caste when it's fictional.

Siddharth@DearthOfSid

Big Bang Theory portrays a waitress and physicists as neighbours because it’s blind to class. In India, class is deeply intertwined with caste. So not only would the waitress be living elsewhere, it’s far less likely she’d ever become friends with physicists, let alone date one.

English

@mydaymywin NCIS Hawaii was really good. I stopped after season 1 only because they cancelled it

English

@karthik2k2 Land of bad & Eyes in the sky in Prime ,

Reptile & Athena in Netflix .

If you want a fun and entertaining watch Midnight runners in prime 👍

English

Dear friends,

Please suggest a fast paced movie for the weekend. (Tamil/Hindi/English) 🙏

Preferably on Netflix / Prime.

English