@loma_homer888 @Richard_X_Roe Can we get more post from you and Richard, it’s helping 😂

English

M.S

221 posts

Tesla battery cell production is getting good

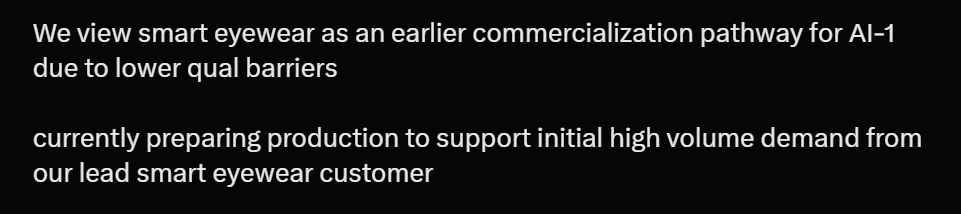

$envx Key parts of Raj‘s prepared remarks: continued advancing smartphone qual with our lead customer engagement expanded across smart eyewear and other AI devices We view smart eyewear as an earlier commercialization pathway for AI-1 due to lower qual barriers currently preparing production to support initial high volume demand from our lead smart eyewear customer defense and industrial programs continue to provide revenue, operational validation and manufacturing execution experience strong liquidity position giving flexibility to execute our commercialization roadmap 2025 positioned us well for the next phase, moving from qualification towards commercialization across smartphones, smart eyewear, and additional defense applications gross margin improved to 23%, reflecting higher production volumes and improved mix shift towards higher-margin defense batteries following our April acquisition We continue to improve yield and throughput across Fab2 Zone 1 laser dicing remains the primary rate-limiting factor, we are methodically addressing that constraint to process optimization and alternative dicing approaches. We believe in our ability to unlock higher production rates In 2026 we are capable of qualifying other new products and customers in the very production line they will use and meeting demand for smart eyewear customers focus remains on disciplined execution, advancing smartphone qual while expanding into adjacent markets that support earlier revenue and manufacturing scale, and leading in smart eyewear markets we introduced this framework for outlining the end applications where our tech can create a durable moat. The smartphone market represents the fastest path, the largest scale, and is ideal for our tech. An independent study validated our energy density leadership in smartphone batteries. This quarter we extended that validation through a second apples-to-apples comparison against a leading competitor using identical methodologies The results confirmed that AI-1 delivers a meaningful volumetric density advantage versus commercially available silicon-doped batteries. We expect AI-2 and AI-3 to further expand our lead with performance gains well beyond historical industry advancement rates We expect to ship our first smart eyewear batteries for use in AI/AR devices in second half of 2026 We believe smart eyewear battery TAM could exceed $400M by 2030. We are targeting meaningful participation based on early engagement with key partners Drones represent another priority area where we see an attractive TAM and a strong competitive advantage. Western drone platforms, both defense and commercial, are increasingly prioritizing higher ED, extended flight time, and supply chain diversification. This battery segment is projected to be approximately $1.5B this year Breaking into these markets reflects growing conviction that we are well-positioned across multiple high-growth platforms we remain engaged with 7 of the top 8 global smartphone OEMs and validation efforts have expanded this year with multiple leading OEMs including those serving the US market. Our near-term focus remains on 2 Asia market leaders Most of the [Honor] requirements have now been met, and cycle life testing remains the primary gating item to complete qual cycle life results are complex and depend heavily on test protocols, which is especially important when evaluating next-gen silicon tech. When we say cycle life testing, we are referring to multiple tests based on different charge and discharge rates, or C-rates. This is standardized measure of how quickly a battery is discharged relative to its total capacity Cont’d…