Planemo Trading@PlanemoTrading

what is statistical arbitrage and why we built an algo around it.

stat arb is one of the oldest strategies in quantitative finance. it originated in the 1980s on morgan stanley's equity trading desk and has been a core strategy at hedge funds and prop firms ever since.

the concept is simple: find two or more assets that historically move together. when their prices temporarily diverge, bet on convergence. buy the one that dropped too far, short the one that rose too far, and wait for the relationship to normalize. you profit from the spread, not from market direction.

the classic example is coca-cola vs pepsi. same industry, same macro exposure, prices move in tandem. when one drifts away from the other, the gap almost always closes. stat arb captures that gap, hundreds or thousands of times.

it's market-neutral by design. you're not betting on up or down. you're betting on the relationship between two instruments reverting to its statistical mean. this is what makes it so attractive: it works in bull markets, bear markets, and sideways chop.

traditionally this has been the domain of institutional desks with massive infrastructure. you need real-time data feeds, fast execution, statistical models to identify pairs, and risk systems to manage hundreds of simultaneous positions.

now here's where crypto changes the equation.

perpetual DEXs are fragmented. the same asset trades on dozens of venues with different liquidity, different market makers, and different pricing dynamics. the same ETH perp on hyperliquid and extended can deviate by several basis points multiple times per minute. these are structural inefficiencies baked into how decentralized exchanges work.

this is what our stat arb algo exploits.

we identify mean-reverting price dislocations between correlated perpetual markets across venues. when a spread deviates beyond a statistical threshold, the algo enters. when it converges, it exits. delta neutral. no directional exposure.

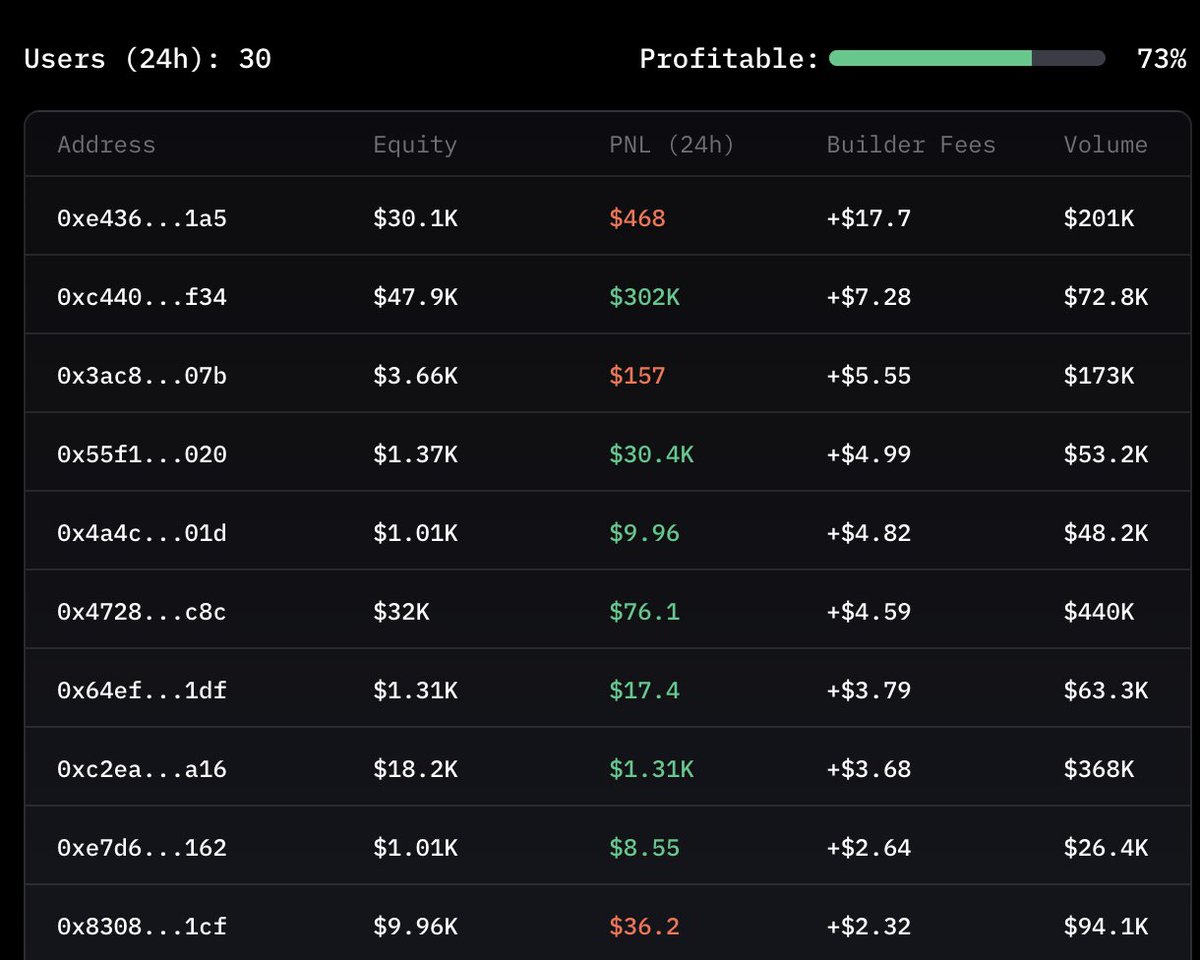

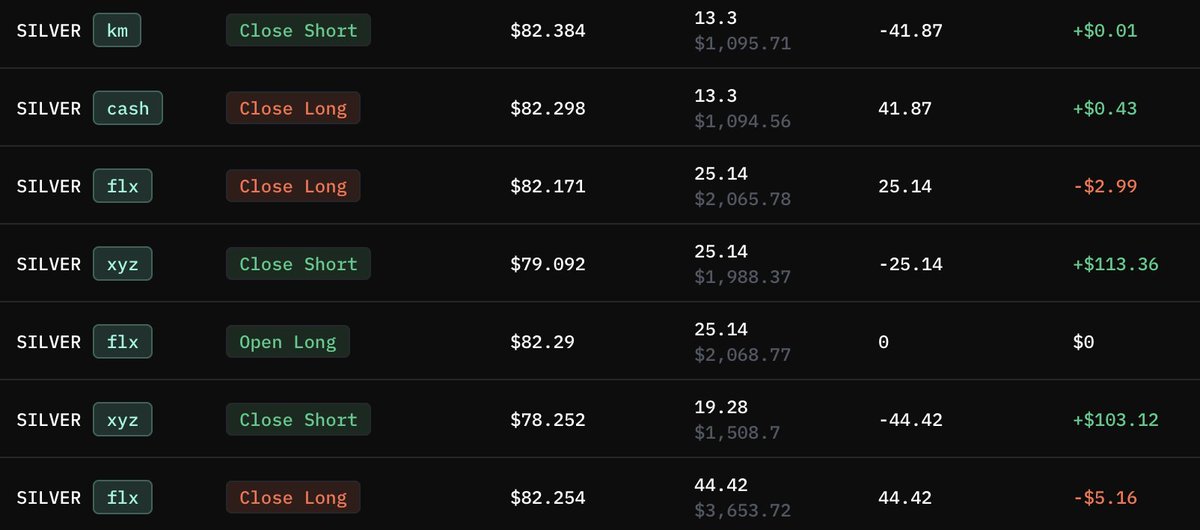

we started with the low hanging fruit. HIP3 across @markets_xyz @tradexyz @felixprotocol @Dreamcash to validate the performance.

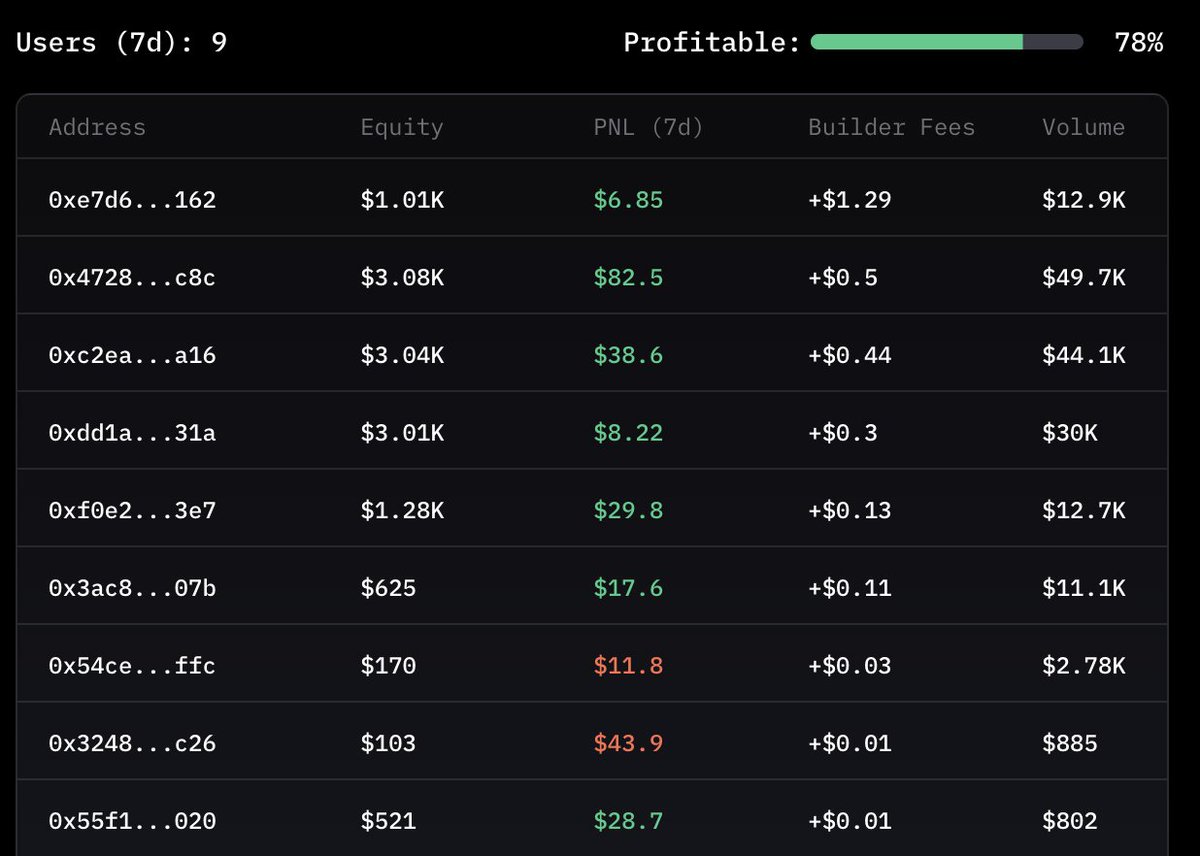

current results: 97% win rate, +1.4 bps average per trade, running 24/7. we're now live on @HyperliquidX, farming HIP3 rewards at positive PnL after all fees.

for context: every other volume tool on the market costs you $200-700 per $1M in volume. you pay to farm. with our stat arb, the farming pays you.

scroll our feed to see live results. early testers are confirming the same performance on their own accounts.

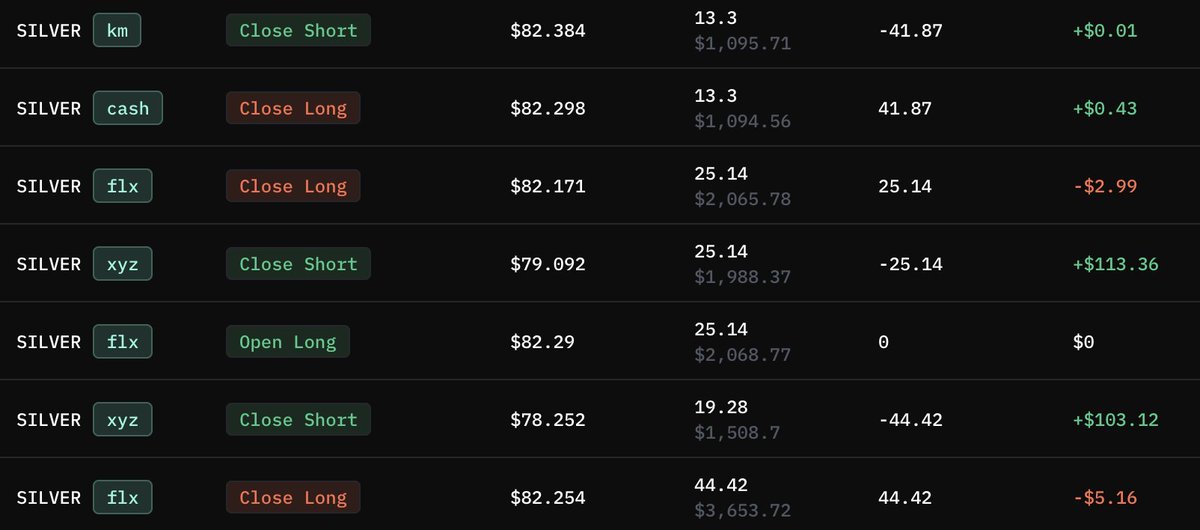

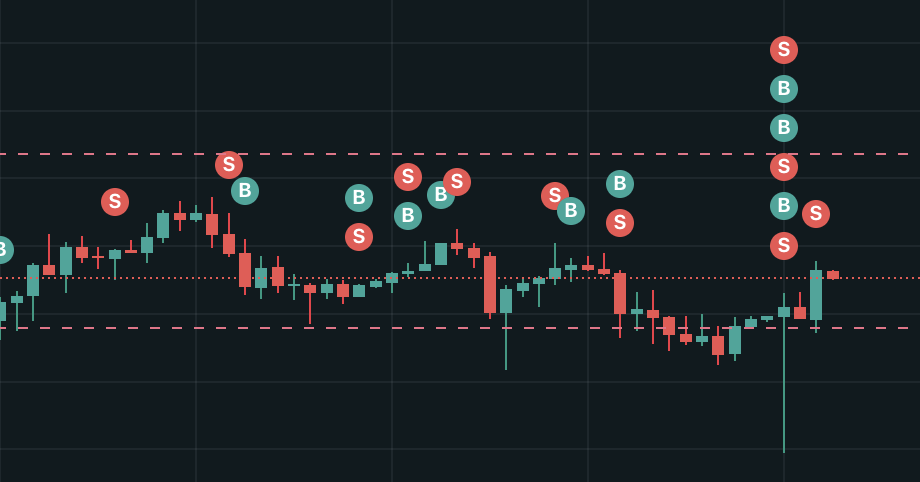

trades like in the image below happen all day long, 24/7.

next step is to expand this tech across more tickers and exchanges.

hip3.planemotrading.xyz