The Valuation Shop

978 posts

The Valuation Shop

@Valuation_Shop

On a quest to understand valuation and separate price from value in the stock market (without losing my mind)

Bay Area, CA Joined Kasım 2025

115 Following135 Followers

A collection of High-Quality Businesses 📈

Visa

ASML

LVMH

Zoetis

Adobe

L'Oreal

Amazon

Alphabet

Microsoft

S&P Global

Mastercard

Constellation

Idexx laboratories

What else?

English

@NotA_Bull We'll probably see a large acquisition from them in the coming year or so as well

English

If you think slow and steady wins the race, grab some $BRK.B and $BA while it's below $200/share.

Too cheap to ignore, the P/E of $BRK.B is sitting at 15.2.

Make it make sense …

English

@Mr_Derivatives Yes, it really did not seem possible. More likely narrative seemed that search would be hit by ChatGPT and Claude

English

$GOOG inches away from overtaking $NVDA.

If I told you this last year, you would have laughed so hard you would pop an aneurysm.

But here we are…

English

@qualtrim Could it be because they've raised prices? AI competitors like ChatGPT and Claude HAVE to be cutting into search to some degree.

English

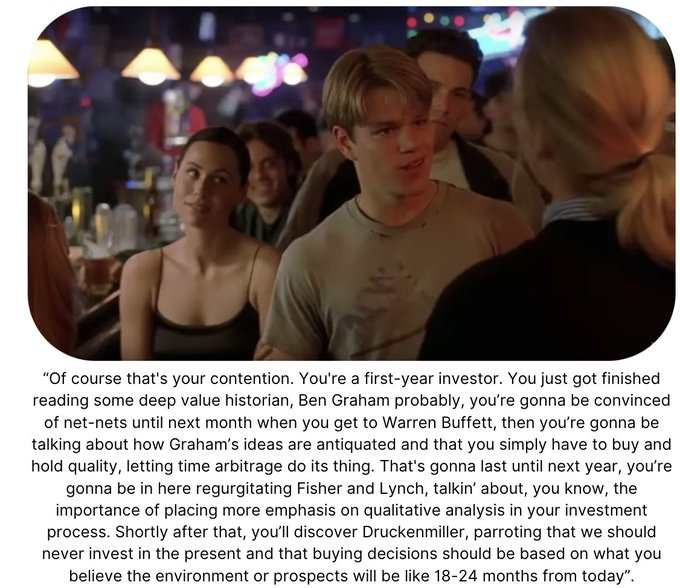

@BrianFeroldi For the Graham and Dodd disciples, this is probably the greatest meme ever created.

Charlie would have nothing to add

English

@SixSigmaCapital It's just incredible. A company this large growing at these rates...

English

Google search growing at 19%…imagine the look on 2024-2025 $GOOGL bears faces when they saw that

Or GCP growing >60% with operating margins high 30’s.

English

I wish I had answers to any of these questions. There's a big future and lots of money to be made, but I just cannot tell who will win and how. Being here in the Bay Area I've seen Waymos and used to see some other AVs around the city for years now, but Waymo is the only company that had a good enough technology to stay and begin offering rides. They're everywhere now. Given that Tesla still doesn't have a completely autonomous competitor, the AV technology must be borderline impossible to develop, and perhaps only a small handful of companies will get the technology where it needs to be and become players.

English

Let's talk about $UBER because it's been on my mind alot recently... I'm assuming others are also debating these questions in their spare time 😏

Last weekend I took a Waymo and it was a wonderful experience so it's fair to say I'm a big believer in robotaxis as the future of ridesharing.

Right now it feels like Waymo is the leader in robotaxis but they only have ~3,000 cars (ie AVs) on the road doing ~500,000 rides per week.

Tesla might be next but they have less than 150 cars (ie cybercabs) on the road doing less than 1,500 rides per week.

$UBER currently has 1.5M human drivers (just in the US) but nothing in terms of robotaxis other than partnerships with Waymo and AVride (owned by $NBIS) however both options are very limited... Austin & Atlanta for Waymo... and Dallas for AVride. I do think it's possible that Waymo dumps $UBER in the future and just uses their own app in every market... however I could be wrong and maybe it goes the other way because $UBER does have 200M global customers which is massive distribution for any AV ridesharing service that wants scale.

fwiw, $UBER currently does 200-250M rides per week which is 400-500x more than Waymo... however Waymo just raised capital at $126B valuation while $UBER currently trades at $153B valuation. I know some people think Waymo will be the winner but kind of crazy it's already worth 80% of $UBER with just 3,000 cars on the road vs $UBER with 1.5M US drivers and another 4M+ drivers outside the US.

Over the past ~12 months $UBER has announced 15+ partnerships with different brands and OEMs including Lucid, Rivian, Nissan, Pony, Zoox, Nuro, Oro, WeRide, Baidu, Wayve, Volkswagon, May Mobility, Momenta, Mercedes and probably a few more that I'm forgetting about.

I don't think we need to debate that $UBER already has massive distribution but my question is around these 15+ partnerships. Sure it's lots of constant PR which might sound good but we have very limited details... which of these AV companies has technology that is good enough to compete and scale?

Putting tens or hundreds of thousands of AVs on the road in the coming years will be extremely expensive and capital intensive. I'm sure Baidu and Mercedes could handle the upfront capex but I don't know about these other brands. So who is covering the capex? the brand? uber? or do they split it?

With the capex in mind, what does the rev share look like for these partnerships? Will it be the same across the board or does every partnership have different economics? For instance, let's say Pony.ai can't afford the upfront capex themselves, do they split it with $UBER? or does $UBER cover 2/3 of the capex but then they own 80% of the rev share?

Let's say Baidu and Mercedes can afford the capex themselves and they want to go that route... does that mean $UBER just handles distribution & logistics but only gets to keep 1/3 of the rev share?

Obviously I'm just making up numbers and scenarios because we don't have much else to go on.

Would you prefer $UBER stay asset light and just collect a 1/3 toll like they do now? or do you want $UBER to leverage up the balance sheet to become asset heavy in order to get a bigger rev share % ?

and here comes the monkey wrench in all of this... what if $UBER enables anyone with an AV (similar to what $TSLA might do)... to put their car onto the $UBER network in order to generate some extra income while they're working, sleeping or just not using the car? This would allow $UBER to stay asset light and maybe collect a higher % of the rev share since the car owner might be very happy just collecting 40% of the revenues since it's extra income for them not including the accelerated depreciation.

I'd love to know how others are thinking about this... especially $UBER shareholders... what do you think is the right business/economics model going forward? and do you want them in the capex business in order to get a bigger rev share?

I am very curious to see how this all plays out in the coming years.

NFA.

DYOR.

**We have a tiny $UBER position at @FirstWaveFund because I think the valuation is attractive when you consider 200M customers with the potential to be the robotaxi leader... but I still have lots of concerns about what their strategy looks like going forward and what % of the ridesharing market they lose to Waymo and Tesla and if the TAM can grow big enough for all three companies to be winners? Best case for $UBER is the TAM keeps growing and even as they lose market share the economics for robotaxis are meaningfullly better than a human focused ridesharing network.

Jonah Lupton@JonahLupton

Some of you know that I launched a hedge fund several months ago (early November). We run a long/short strategy, focused on owning the 20-40 growth stocks that we believe have the most upside over the next 2-3 years... this means they need to have great fundamentals, strong management teams, compelling valuations, and multiple catalysts that we can identify and track accordingly. It's been a rough few months for many growth investors (we also took some pain)... thankfully we were averaging down into our core positions but we've still seen some red months and it has not been enjoyable. I'm not a fan of losing money. Stepping back... I've never had more conviction in my process or my portfolio than I do right now... especially with some of my favorite stocks down 20-40% from their September/October/November highs despite strong Q4 earnings reports, strong CY2026 guidance and extremely compelling valuations. With that said, here are our top 10 positions in alphabetical order: $APP $CPNG $CRDO $HIMS $HROW $SKHYNIX $IREN $NBIS $RDDT $TMDX I believe all of these stocks are trading at meaningfully higher prices in 2-3 years which remains my focus for generating outsized long-term returns. Enjoy the rest of your day 😊 NFA. DYOR. ** @FirstWaveFund owns all of the stocks mentioned in this post.

English

@StockSavvyShay It's hard to believe how much $GOOGL is still growing, given their size

English

This was one of the books that reprogrammed my brain to recognize that an interest in investing is absolutely compatible with, and indeed a high expression of, dedication to broad learning

English

@DividendDynasty We see $BRK.B continuing to grow under Greg Abel's leadership. May perhaps even see a large acquisition in the next few years.

English

Berkshire has had a rough year, now down -10% 📉

Is $BRK.B currently an opportunity in a market that keeps pushing new ATHs?

Cash and Cash Equivalents sits at $373.31B or roughly 37% of the current market cap 🤯

I’m long $BRK.B and it currently makes up 10% of my own portfolio

English

$GOOGL Cloud Q1 revenue hit $20.0B (up 63% YoY) with operating income reaching $6.6B.

Insanity for a company this large

The acceleration is an increase in demand for GPUs and core Cloud. Plus, the revenue backlog just doubled to $460B.

English

Thanks for coming on Rose, it was great talking to you!

The podcast will be released next week!

Rose Celine Investments 🌹@realroseceline

I did my first podcast ever today and honestly it was a really enjoyable experience. Looking back, I probably could have gone deeper on a few answers, but that likely just comes with doing more of these over time. Really appreciate you having me on @DrewCohenMoney. You’re a great interviewer and I genuinely mean that. The episode will be available next week, so definitely check it out. And if you’re not already following Drew and listening to his podcast, you should be! 🌹

English

Mohnish Pabrai: "We choose what books we want to read — and that narrows what data we are taking in. I have no control over which books David Senra puts in the @FoundersPodcast. So I decided I'm going to listen to every podcast he did ... because that will introduce randomness."

English

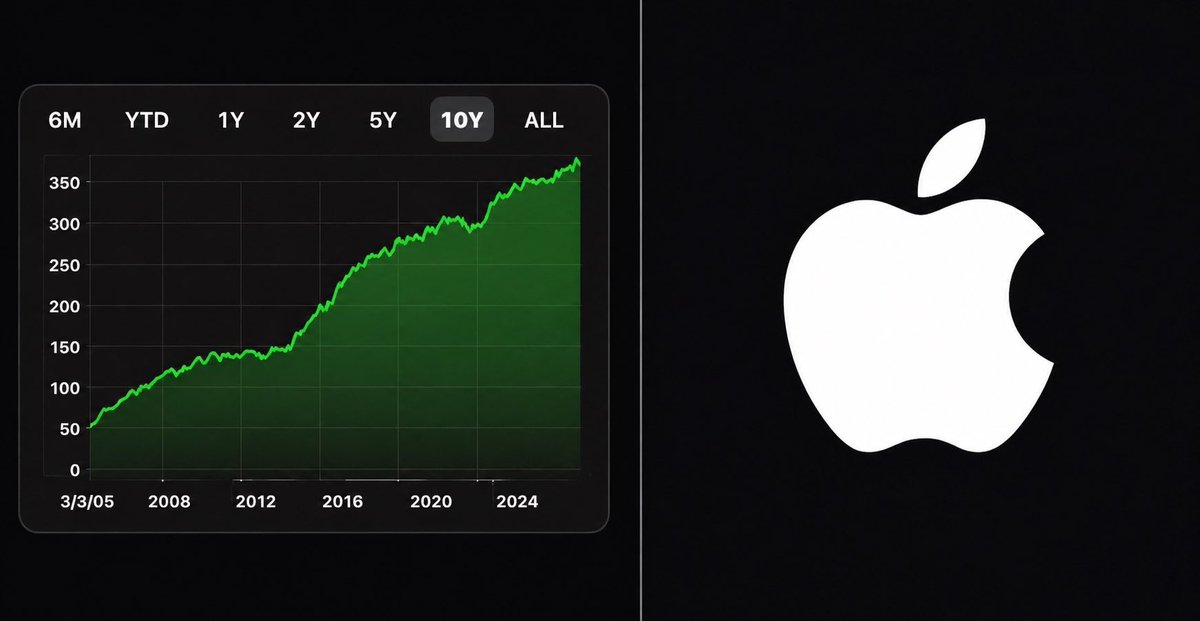

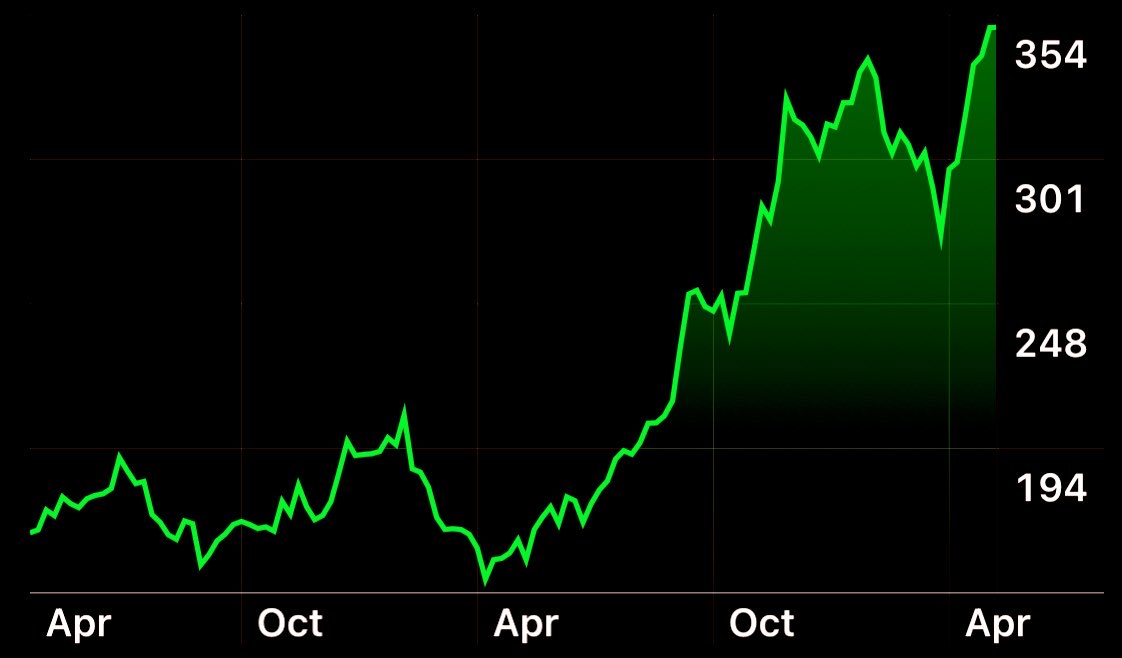

If you just put your entire portfolio into $GOOGL last April and then sat on the beach, you'd be up +155% in one year…

You stupid idiot.

English

I accept defeat, I did not suspect revenues to accelerate to this extent

All hail the one true king Sundar full-stack

$GOOG $GOOGL

English

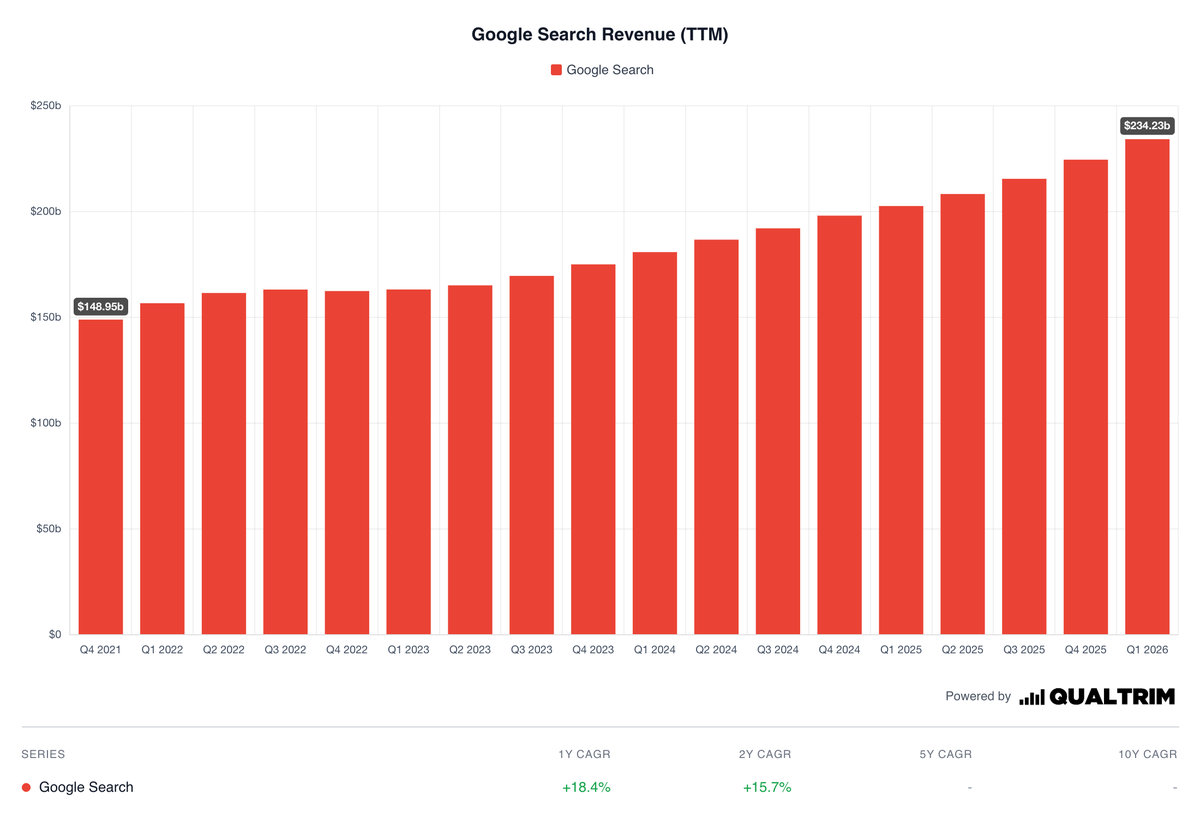

$GOOGL "search" revenue is up 19% YoY

Many are surprised by this large of an increase on a percentage basis, but don't forget ad prices have been going up

Sundar Pichai@sundarpichai

Q1 earnings are in: 2026 is off to a terrific start. Our AI investments and full stack approach are lighting up every part of the business: Search queries are at an all-time high with AI continuing to drive usage. Google Cloud revenue grew 63%, Gemini models have incredible momentum, and it was our strongest quarter ever for consumer AI subs, driven by @GeminiApp. Thanks to our partners + employees around the world. Much more to share on our earnings call in 20 minutes… and at Google I/O in 20 days!

English

After seven years of intense work, I am excited to announce that my new book, The Law of the Sublime, will be out in November. and is now available for pre-order (see link below).

The book is designed to expand your mind, and to reveal to you a world to explore beyond what you consider reality: the realm of the Sublime.

This adventure does not require travel, drugs, or any form of external stimulation.

It only requires a new pair of eyes to see the extraordinary all around you.

Through stories, exercises, and meditations, the book will immerse you in the Sublime and forever transform how you experience life.

English

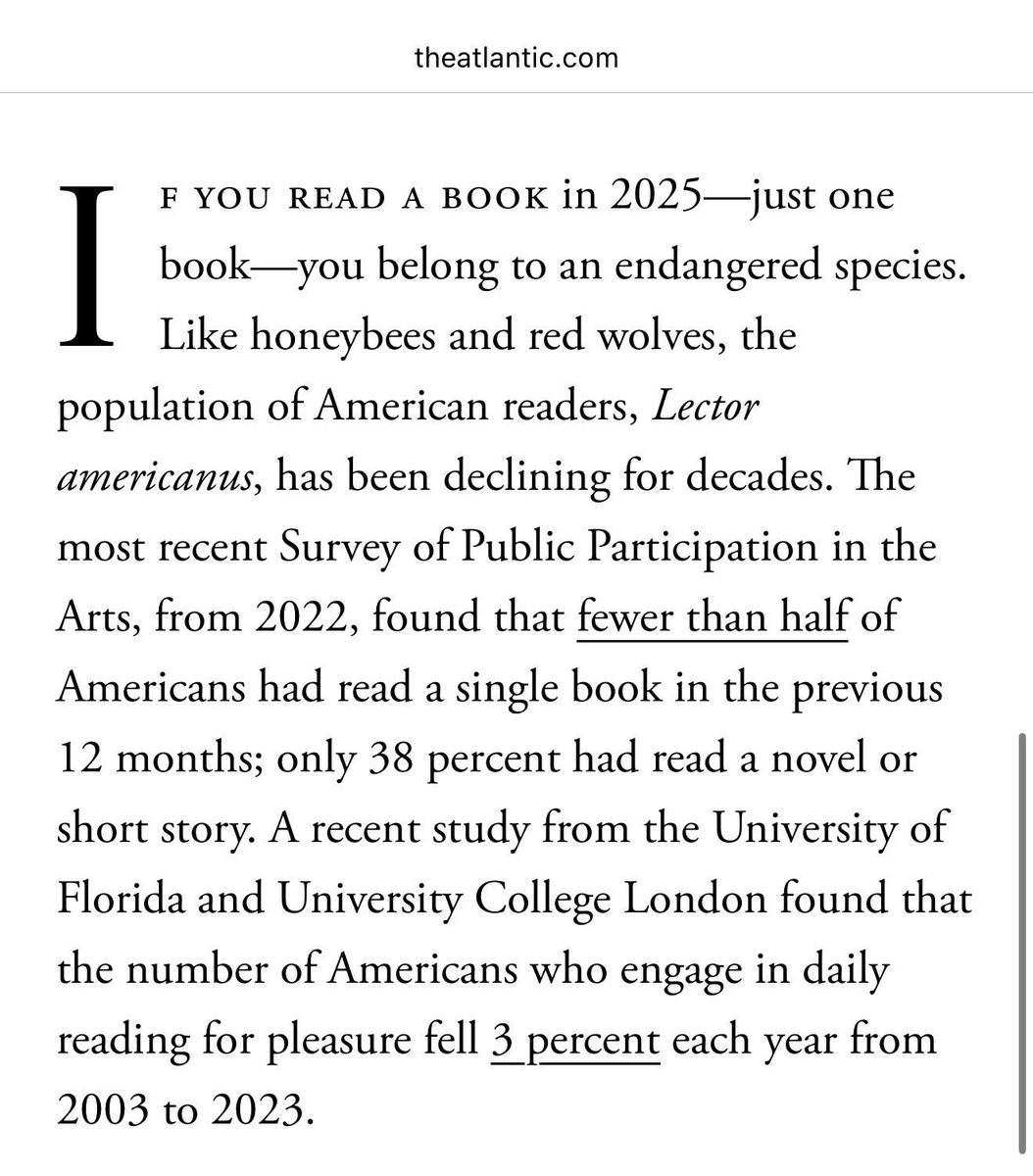

Fewer than half of US adults read a book last year.

Even fewer read an actual novel, and the trend is looking worse still for teenagers.

Why is nobody talking about this??

English