Tweet fijado

Glenn

948 posts

Glenn retuiteado

TODAY 🚨: The Commission issued an interpretation that clarifies the application of federal securities laws to crypto assets.

This is a major step to provide greater clarity regarding the Commission’s treatment of crypto assets.

Read the release here: ow.ly/XhhV50YvxvO

English

Glenn retuiteado

Glenn retuiteado

In 1971, money changed from a natural system (gold) to a socialist system (fiat).

Crypto is tech to replace socialist money with a free-market system.

Market systems are inherently competitive and as tech evolves, new monies will continue to emerge to challenge existing ones.

English

Glenn retuiteado

We think stablecoins are just the start of what’s possible with programmable money and we’re excited to fund teams building what comes next. Thanks @jessepollak for talking with me about what that might be and why now is the time to build it.

Y Combinator@ycombinator

We are entering the era of Fintech 3.0. Regulatory clarity, growing consumer adoption, and low-cost chains have paved the way for a golden age of building in crypto — and at YC, @base and @coinbase we want to fund builders to seize this moment. @harjtaggar and @jessepollak sat down to discuss what kinds of companies they're most excited to see, why this is such an exciting time, and what the future could look like onchain. 00:00 – The Golden Age of Crypto 02:00 – Jesse’s Path to Coinbase & Base 04:00 – From Fintech 1.0 to Fintech 3.0 07:00 – Why Lowering Costs Changes Everything 10:00 – L1 vs. L2, Simply Explained 13:00 – How to Build Your First Crypto App 16:00 – Regulation: Bottleneck or Unlock? 19:00 – Stablecoins as the Killer Use Case 23:00 – Beyond the Dollar: Local Stablecoins 27:00 – Tokenization of Assets 31:00 – New Asset Classes & the Creator Economy 35:00 – What Coinbase Looks for in Founders 39:00 – The Future of Crypto in 10 Years

English

Glenn retuiteado

Markets on everything.

We’re proud to announce that $ICE, the owner of @NYSE and the largest exchange company in the world, is making a strategic investment of $2 billion into Polymarket, valuing us at $9 billion post-money.

Our partnership with ICE marks a major step in bringing prediction markets into the financial mainstream. But in addition to that, it’s a monumental step forward for DeFi. ICE is the one remaining founder-led exchange company, and Jeff is all-in on utilizing his assets, including NYSE, to usher in a new financial era of tokenization. We’re humbled to be working together on this endeavor. ICE will also begin distributing Polymarket data to thousands of financial institutions around the world. There is so much to build when you combine the force of ICE’s institutional scale and credibility with Polymarket’s consumer + cultural savvy and distribution.

The past two years have been surreal. Going from a write off to creating a category, watching our vision become a reality. The Polymarket origin story is funny because it's a rare case of the dream being identical to how things played out. If I learned one thing, it’s that bold ideas are everywhere, hidden in plain sight. It just takes someone crazy enough to spend their life willing it into existence. That’s entrepreneurship: willing things into existence.

I remember reading Robin Hanson’s literature on prediction markets and thinking - man, this is too good of an idea to just exist in whitepapers. There were a million reasons why it shouldn’t work, countless arguments of why not to do it, and the odds were against us, but we had to try.

At the onset of the pandemic, I quite literally had nothing to lose: 21, running out of money, 2.5 years since I dropped out and nothing to show for it. But I knew we were entering an era where ways to find truth would matter more than ever, and Polymarket could play a critical role in that. After all, nothing is more valuable than the truth. It’s still a work in progress, but we’re honored to have made the impact we have thus far.

I’d also like to give a special thank you to all of our users, builders, and community members who have been with us since 2020. Your support will not be forgotten 🔮

Last but not least, I am deeply grateful for all of the support and hard work of my brilliant team. I’m getting to live my wildest dreams, seemingly against all odds, and I don’t take it for granted.

The best is yet to come… 🇺🇸

Que Sera Sera

English

hosting london tings with @binji_x and @StaniKulechov 🇬🇧 if you’re here let us know!

English

Glenn retuiteado

How to build a category defining project:

- Have a unique vision

- Believe in it deeply

- Give 0 fucks about short-term

- Persistence

- Will to win

Study Coinbase, Ethereum, Opensea, Bridge, Polymarket, etc.

English

Glenn retuiteado

0/ Token markets are broken & suffer from information asymmetry & hidden risks.

We're changing that.

Introducing the Token Transparency Framework, a new standard for leveling the playing field.

English

Glenn retuiteado

Insane how far defi has come so quickly 🤯

Maker + Compound + Uniswap launches in 2018 feel like the true start of the movement (+others like 0x, augur, etc)

The word DeFi didn't even exist before then

Now government agencies publicly recognize it as a national priority

U.S. Securities and Exchange Commission@SECGov

The American values of economic liberty, private property rights, and innovation are in the DNA of the DeFi, or Decentralized Finance, movement.

English

Glenn retuiteado

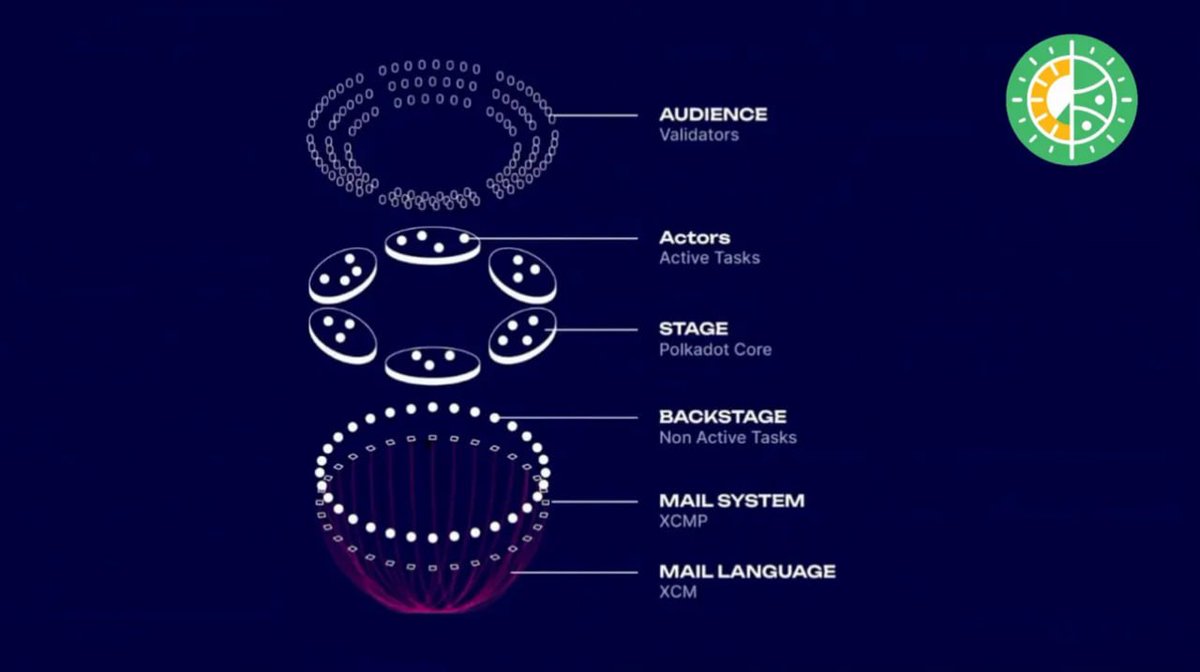

polkadot launched in 2020, but its ideas still feel futuristic:

• modular blockspace

• on-demand execution

• chain-level governance

• native cross-chain logic

most of what's trending today - rollups, appchains, interoperability - @polkadot already built its own version years ago

its architecture still questions how chains should really talk to each other ( 🧵👇 )

here's what i'll explore:

→ intro: what is polkadot & why it matters

→ relay chain: the backbone of polkadot

→ parachains: modular chains w/ shared security

→ opengov: polkadot's decentralized governance

→ consensus: nominated proof-of-stake explained

→ substrate: building custom chains

→ agile coretime: flexible blockspace allocation

→ interoperability: cross-chain messaging via xcm

▫️what is polkadot

polkadot started as a bet: what if multiple chains could share security and talk to each other?

not bridges. not wrapping assets. actual native messaging across different chains.

each parachain works like its own L1 - but they all plug into a central relay chain. that relay chain doesn't run smart contracts. it just keeps everyone in sync, secure, & connected.

the goal? composable, sovereign chains that still feel like one ecosystem.

▫️relay chain

• no dapps here

• no user logic

• just validation, finality, and cross-chain messaging

validators rotate across parachains, validate block candidates, & finalize them on the relay chain. it's like a referee in a game - doesn't play, just enforces rules.

also where $DOT staking, governance & slashing logic live.

▫️parachains

every parachain can be completely different.

some are DeFi hubs, some run ZK circuits, some focus on privacy, some act as bridges.

they all customize their execution logic w/ substrate, but still follow the relay chain's consensus.

what's interesting is they don't rely on external trust assumptions when talking to each other.

XCM (Cross-Consensus Messaging) handles that, it's native.

▫️governance (opengov)

openGov replaced the old council-based model.

anyone can start a referendum, anyone can vote. votes carry conviction - the longer you're willing to lock your tokens, the stronger your vote.

there's no emergency veto, no fast track. it's flatter, slower, & more transparent.

▫️consensus

nominated proof-of-stake (NPoS) is what runs under the hood.

• nominators stake $DOT to back validators

• validators get chosen based on total backing

• bad behavior gets slashed

• rewards are shared proportionally

the twist is: nominators hold a lot of power. they don't run nodes, but their choices decide who gets in.

that can be good - or dangerous if people stake blindly.

▫️substrate

substrate is how polkadot ships features

every parachain is built w/ substrate. but also the relay chain.

you pick pallets (prebuilt modules), add custom logic, and ship.

want to change governance? plug in a new pallet.

want new tx logic? build your own runtime module.

no need for hard forks - just upgrade logic at runtime.

▫️agile coretime

parachains used to bid for slots through auctions - it was expensive & risky.

agile coretime changed that.

• teams can now buy execution time in chunks

• pay on demand, reserve in advance, or commit longer term

• slot auctions still exist - but now there are more flexible options

this should lower the barrier for smaller teams, sidechains & experiments.

▫️cross-chain messaging

xcm is what lets chains inside polkadot actually talk.

it's not token transfers. it's instructions, logic, full-on programmatic messaging between chains.

you can call contracts on another chain, move assets, trigger actions - all in a trust-minimized way.

the challenge? it's complex. from my pov not many teams use its full potential yet.

also: most retail still doesn't know what polkadot is.

🔃 found this useful? repost to help others read

English

Glenn retuiteado

You’re not behind.

You’re not too late.

You’re not missing out.

You’re on your timeline.

And your path doesn’t have to look like anyone else’s.

English

Glenn retuiteado

🇧🇲 Bermuda just went onchain.

At the Bermuda Digital Finance Forum, attendees used @USDC to pay local merchants — fast, secure, and fully digital.

The future of finance is already here.

English

Glenn retuiteado

Stablecoins: Payments Without Intermediaries

The internet made information free and global. So why is it still so hard — and expensive — to move money?

The early internet promised a future where anyone could publish, build, or transact without permission. Protocols like email and the web were open and neutral — and they sparked an explosion of creativity, innovation, and entrepreneurship. But somewhere along the way, we veered off course.

Today, the global financial system resembles a patchwork of corporate networks: centralized, closed, and extractive. Behind every transaction is a Rube Goldberg-machine of intermediaries — points of sale, payment processors, acquiring banks, issuing banks, local banks, correspondent banks, foreign exchanges, card networks, and others — each taking a cut, adding latency, and imposing rules. These networks levy unnecessary taxes on commerce and curb innovation. They turn what should be neutral plumbing into high-friction bottlenecks.

Stablecoins, or cryptocurrencies pegged to stable assets like the U.S. dollar, are a way out, a reset — a way to bring the internet’s original vision to money.

The Disruptive Opportunity of Stablecoins

The current payments stack wasn’t built for the internet — it was built for a world rife with fee-taking middlemen (who had been necessary to manage local partnerships, fraud, and operations). Even today, international remittances can cost up to 10% in fees. (A $200 remittance cost 6.62% on average in September 2024.) These aren’t just friction points — they’re effectively regressive taxes on some of the world’s poorest workers. The system we’ve inherited is slow, opaque, and exclusionary, and it leaves billions of people underserved or entirely cut off from the global financial system.

For many businesses, the inefficiencies of traditional payments are also massive. Stablecoins could dramatically improve the situation. B2B payments from Mexico to Vietnam take 3-to-7 days to clear and can cost anywhere from $14-to-$150 per $1000 transacted, passing through as many as five intermediaries along the way, each of whom takes a cut. Stablecoins could bypass legacy systems, like the international SWIFT network and associated clearing and settlement processes, and make such transactions nearly free and instant.

This isn’t theoretical — it’s already happening. Right now, companies like SpaceX are using stablecoins to manage their corporate treasuries (including by repatriating funds from countries with volatile local currencies, like Argentina and Nigeria). Other companies, like ScaleAI, are using stablecoins to make faster, cheaper payouts to global workforces. Meanwhile, on the B2C side, Stripe is the first widely used service to offer crypto payments and it is already offering 1.5% on checkout — half what incumbents charge. This could drastically improve certain businesses’ profit margins: As a16z crypto’s @SamBroner has shown, for a very low margin business like a grocery store, a 1.5% improvement could potentially double net income. (And in a competitive, blockchain-based market, I would expect transaction fees to go much lower.)

Unlike the old financial stack, which evolved in silos, stablecoins are global by default. They live on blockchains: open, programmable networks that anyone can build on. There’s no need to negotiate with dozens of banks across borders. You just plug into the network. People are already recognizing the advantages. In 2024, stablecoins moved $15.6 trillion in value, effectively matching Visa’s volume. While that figure mostly represents financial flows (versus retail payments), its magnitude still suggests we’re on the verge of a financial infrastructure shift, one that doesn’t rely on duct-taping 20th-century systems together.

Instead, we can build something new, something truly internet-native — or what Stripe calls “room-temperature superconductors for financial services,” where rather than lossless energy transmission, you get lossless value transmission.

The WhatsApp Moment for Money

Stablecoins are our first real shot at doing for money what email did for communication: make it open, instant, and borderless.

Consider the evolution of text messaging. Before apps like WhatsApp, sending a text across borders meant paying 30 cents per message. Even then, you were lucky if it actually got delivered. Then came internet-native messaging: instant, global, free. Payments are now where messaging was in 2008: Fragmented by borders. Burdened by middlemen. Gatekept by design.

Stablecoins offer a clean-slate alternative. Instead of stitching together clunky, costly, and outdated systems, stablecoins flow seamlessly on top of global blockchains. These systems are programmable, composable, and designed to scale across borders. Already, stablecoins are slashing the cost of remittances: Sending $200 from the U.S. to Columbia using traditional methods will cost you $12.13; with stablecoins, it costs $0.01. (Fees to convert from stablecoins to local currencies can range from as high as 5% to as low as 0%, and prices continue to fall due to competition.)

Just as WhatsApp disrupted costly international phone calls, blockchain payments and stablecoins are transforming global money transfers.

Regulation: From Bottleneck to Breakthrough

It’s tempting to frame regulation as an obstacle — but smart legislation is actually the unlock.

Clear rules of the road for stablecoins and crypto market structure could finally allow these technologies to move out of the sandbox and toward widespread adoption. For years, decentralized finance (DeFi) was trapped in a kind of self-contained, circular, “crypto-for-crypto” economy. Not because the tools weren’t useful, but because regulators made it incredibly difficult to bridge into traditional financial systems.

That’s changing. Policymakers are now actively shaping rules to recognize and regulate stablecoins in ways that maintain U.S. competitiveness, protect consumers, and allow innovation to flourish. Thoughtful regulation — like frameworks that differentiate network tokens from security tokens — can protect against bad actors while giving good actors the clarity they need to build. In fact, a forthcoming bill clarifying this regulation could pave the way for even broader adoption and integration into the global financial system. (Congress is hashing out the details as I write.)

Building Public Goods for Everyone’s Benefit

Traditional finance is built on private, closed networks. But the internet showed us the power of open protocols — like TCP/IP and email — to drive global coordination and innovation.

Blockchains are the internet’s native financial layer. They combine the composability of public protocols with the economic strength of private enterprise. They are credibly neutral, auditable, and programmable. Add stablecoins on top and you get something we’ve never really had before: open money infrastructure.

Think of it like a public highway system. Private companies can still build the vehicles, the businesses, the roadside attractions. But the roads themselves are neutral and open for everyone.

Blockchain networks and stablecoins are doing more than just cutting fees. They’re enabling new categories of software:

- Programmatic payments between machines: Imagine AI agent-powered marketplaces automatically brokering deals for computer resources and other services.

- Micropayments for media, music, and AI contributions: Imagine setting a budget with some simple rules and leaving it to “smart” wallets to disburse the payments.

- Transparent payouts with full audit trails: Imagine using these systems to track spending in government.

- Global commerce without a mess of intermediaries: Imagine settling international transactions instantly at negligible cost — in fact, you don’t have to imagine it as it’s already happening.

The moment for blockchain networks and stablecoins is now: Technology, market demand, and political will are lining up and making these applications a reality. A stablecoin bill could be on the floor this year, and regulatory agencies are weighing frameworks that finally align risk with the right oversight. In the same way that early internet startups were able to thrive once it was clear they wouldn’t be shut down by telcos or copyright lawyers, crypto is ready to cross the chasm from financial experiment to infrastructure backbone, with stablecoins leading the way.

We don’t have to patch the old system.

We can make a better one.

English

Glenn retuiteado

Ethereum-compatible SMART CONTRACTS on @Polkadot

Stage1️⃣ (soon): Smart contracts on @kusamanetwork

Stage2️⃣ (this summer): Smart contracts on Kusama get access to native assets, staking, governance + XCM

Stage3️⃣ (Q3): Smart contracts launch on Polkadot

😍Are you excited yet?

English

Glenn retuiteado

Glenn retuiteado

1/ Stablecoins are reshaping finance 🏦

Explore all insights, market trends, asset deep dives, and more in "The State of Stablecoins 2025"— a comprehensive report by Dune & @artemis

Link at the end of the thread 🧵

English

Glenn retuiteado

Aave Labs is partnering with the Oxford Blockchain Society to deliver lectures on DeFi and smart contracts. Our Oxford alumni will share their knowledge with the next generation of builders.

Oxford Blockchain Society (University of Oxford)@blockchainox

IRL event: Aave Labs x Oxford Blockchain Society - Explore DeFi, Blockchain Fundamentals and the Future of Finance Date: 18th March 2025 Time: 5pm - 8pm Location: Fitzhugh Lecture Theatre, Exeter College, Walton St (Cohen Quad) Join Avara and meet team members behind Aave, Lens, GHO, and Family products for a hosted event for crypto enthusiasts and the crypto-curious alike. You’ll hear directly from our core developers, who will share their insights and experiences at the forefront of DeFi. Don’t miss this opportunity to network and join the discussion. All levels of crypto knowledge are welcome! Register now: lu.ma/aavelabsoxford #AaveLabsOxford

English

Glenn retuiteado

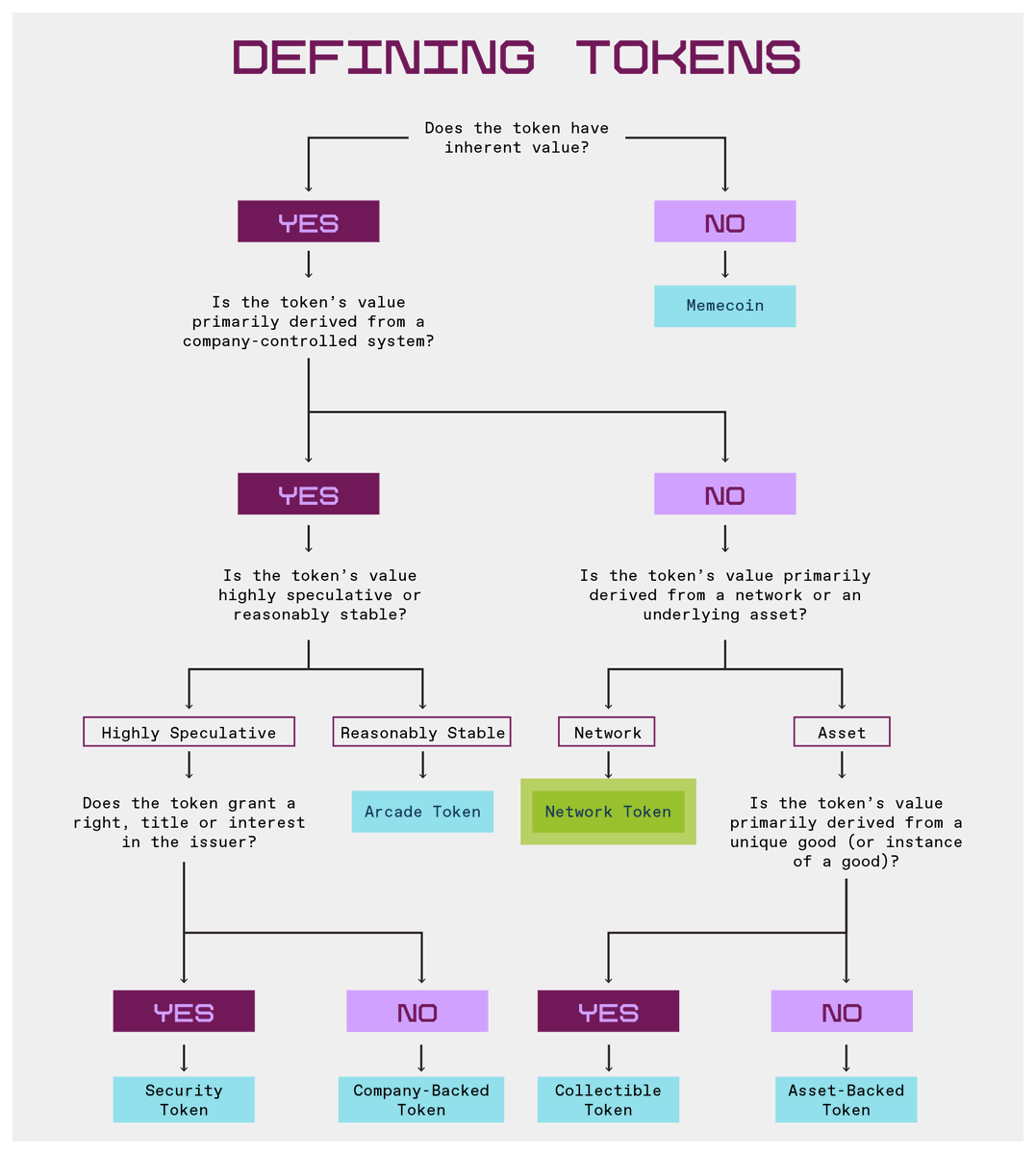

Tokens are the fundamental building block of blockchain networks.

Builders, consumers, and policy makers are all wondering how to distinguish the different types and to better understand their roles and risks.

To help organize the conversation, @a16zcrypto presents definitions, examples, and a framework for understanding the 7 categories of tokens we see entrepreneurs building with most often:

• Network tokens

• Security tokens

• Company-backed tokens

• Arcade tokens

• Collectible tokens

• Asset-backed tokens

• Memecoins

👇

English