Tweet fijado

Stephan Coleman

1.2K posts

@StephanC86

https://t.co/lllWJxF54g sc: big_man91

$SIVE is now up +73.78% today ($231M MC). As markets price in information synthesis of the next potential $LITE of photonics. If I had to explain the difference: One laser source in Lumentum primarily benefits from current optical bottlenecks. The other in $SIVE is for the upcoming CPO/Silicon Photonic bottleneck. Lumentum is largely benefiting right now from $NVDA and hyperscalers securing capacity of EML lasers for current pluggable optical transceivers cycles. As seen with the current EML bottleneck, hyperscalers are buying out any 800G/1.6T transceiver + upstream capacity from: - $AAOI (in-house) - $COHR, $LITE (EML lasers + design) -> $FN (assembly) - $COHR, $LITE (EML lasers) -> Innolight / Eoptolink What's next? Silicon Photonics and Co-Packaged Optics. The architectural shift to CPO requires massive arrays of high-power CW DFB lasers. And this would likely trigger a complete, sudden paradigm shift in volume demand. $SIVE benefits from InP CW DFB lasers for SiPh and CPO: The up and coming companies like: $AYAR, $POET source $SIVE lasers, but primarily do advanced packaging. Then they feed up to larger companies like $MRVL Celestial (that buy $POET's interposers). However, if you go upstream, the light source is $SIVE. CW DFB lasers are light engine ( $SIVE ); the silicon photonics package ( $POET and others) is how it gets transmitted. CPO scale is not there yet. But we know it's coming. And as seen with current optical transceiver cycles: - Light sources from $LITE and $COHR demand much higher valuations than companies like $FN that focus on advanced packaging. Markets have been focusing on $POET, but missed where they get the actual $LITE type light source for Starlight. The risks are present including facing multi-source competition with $LITE, $COHR, $AVGO, and others. So again, make sure to do your own research. But my argument against that: Sivers been early enough to tailor custom lasers to fit $POET, Ayar, and other specifications before they got popular (sort like the $POET to $MRVL Celestial analogy). There's volume risks as well: But the potential Win Semi qualification offsets that. Dilution risk to scale capacity, is always present with every early-stage company as well. I did my thesis on $LITE last year and still love the stock for Google TPU ramp/OCS. But this year, I'm focusing on: $SIVE, as my personal CW DFB laser exposure for the new photonics architectural shift. I’m sharing my own thoughts on capturing the rotation from the current EML cycle to the upcoming CW DFB/Silicon Photonics cycle.

$AEHR looks extremely promising at ~$1.1B MC. Aehr is starting to remind me of an early $TER, mixed with pre-earnings $AAOI. If we look at the timeline and speculated customers: Feb 11th: Sonoma production win for Hyperscaler's AI ASIC processors. (likely $GOOGL, $AMZN, $META). - Probably Google? Aehr bought Incal, who was speculated to be used by Google for their TPUs. Feb 26th: $14 million from AI lead customer (likely $AMD, $NVDA) - Probably $AMD here for Instinct MI300/MI400. March 3rd: Lead silicon photonics customer for one FOX-XP system (likely $INTC siph) - Very likely $INTC has been their lead customer. March 31st: Initial order from major new silicon photonics customer (likely $AVGO, $MRVL, $CSCO ) - New customer (rules out Intel), prob one of these transitioning to 800G/1.6T silicon photonics transceivers (All speculative, very confidential BOM) Regardless. This timeline is just bottling up for $AEHR. Could be next earnings. Or two quarters from now. But feels like a matter of time before we see mass orders.

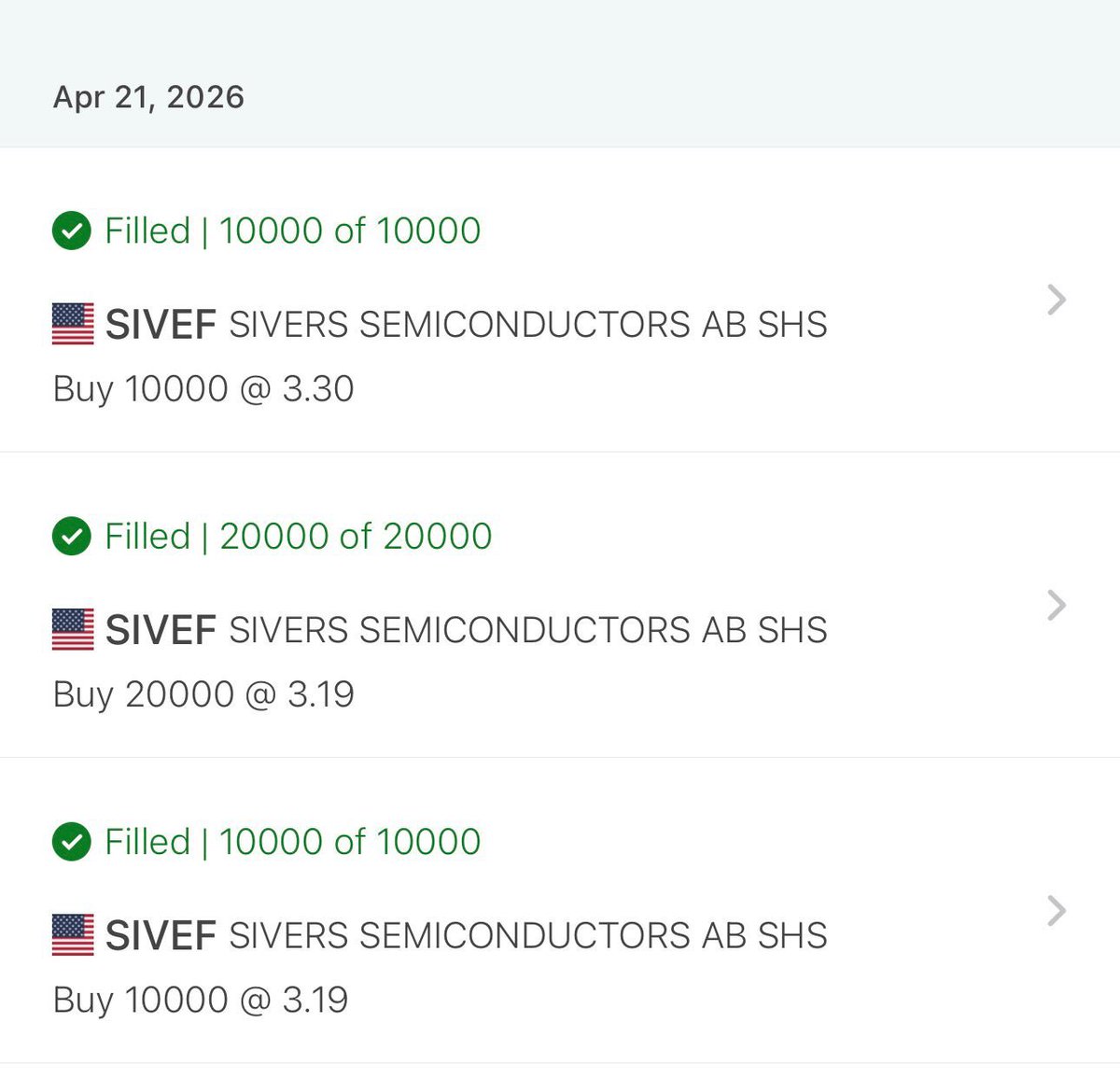

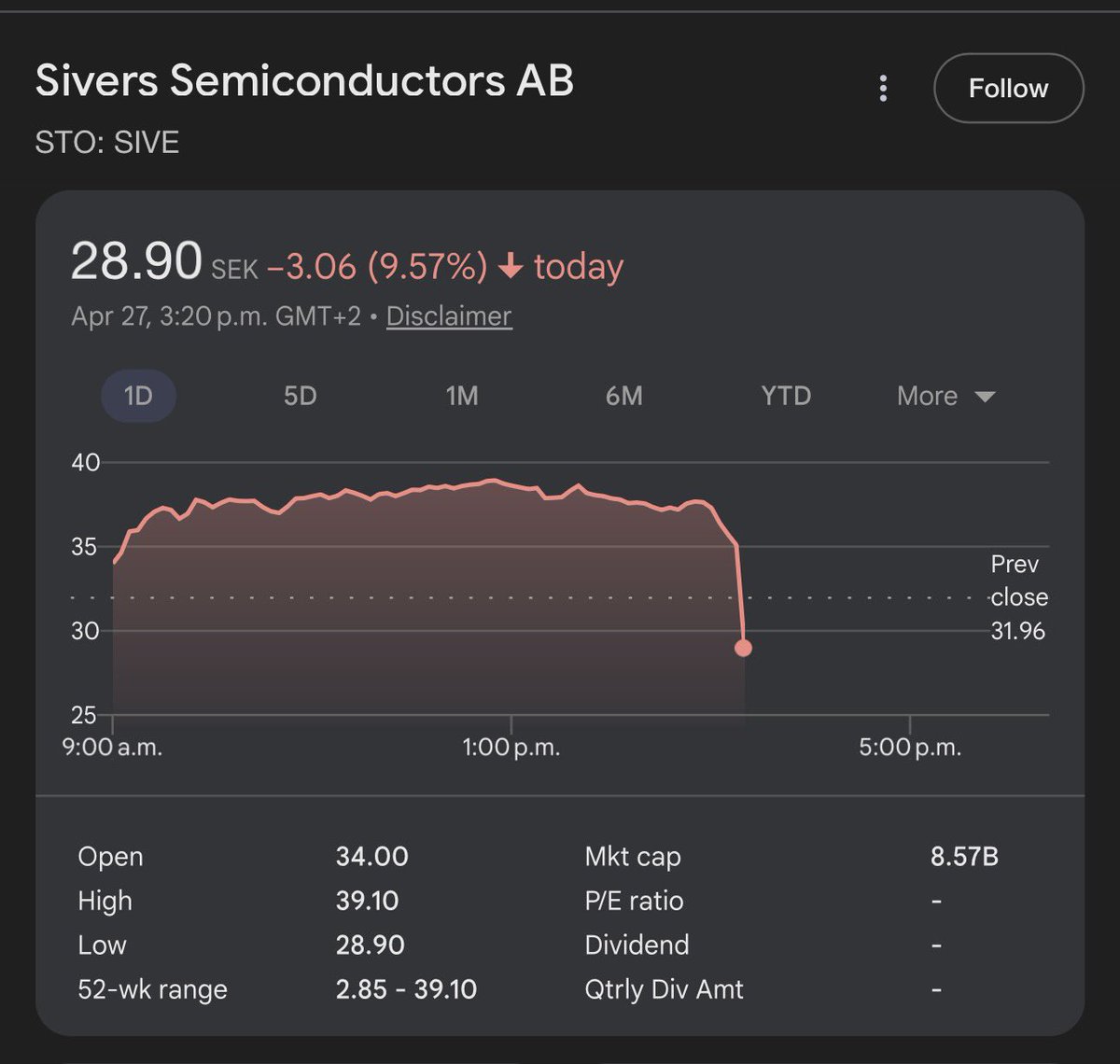

@aleabitoreddit Looks like the Swedes are selling again 🤣

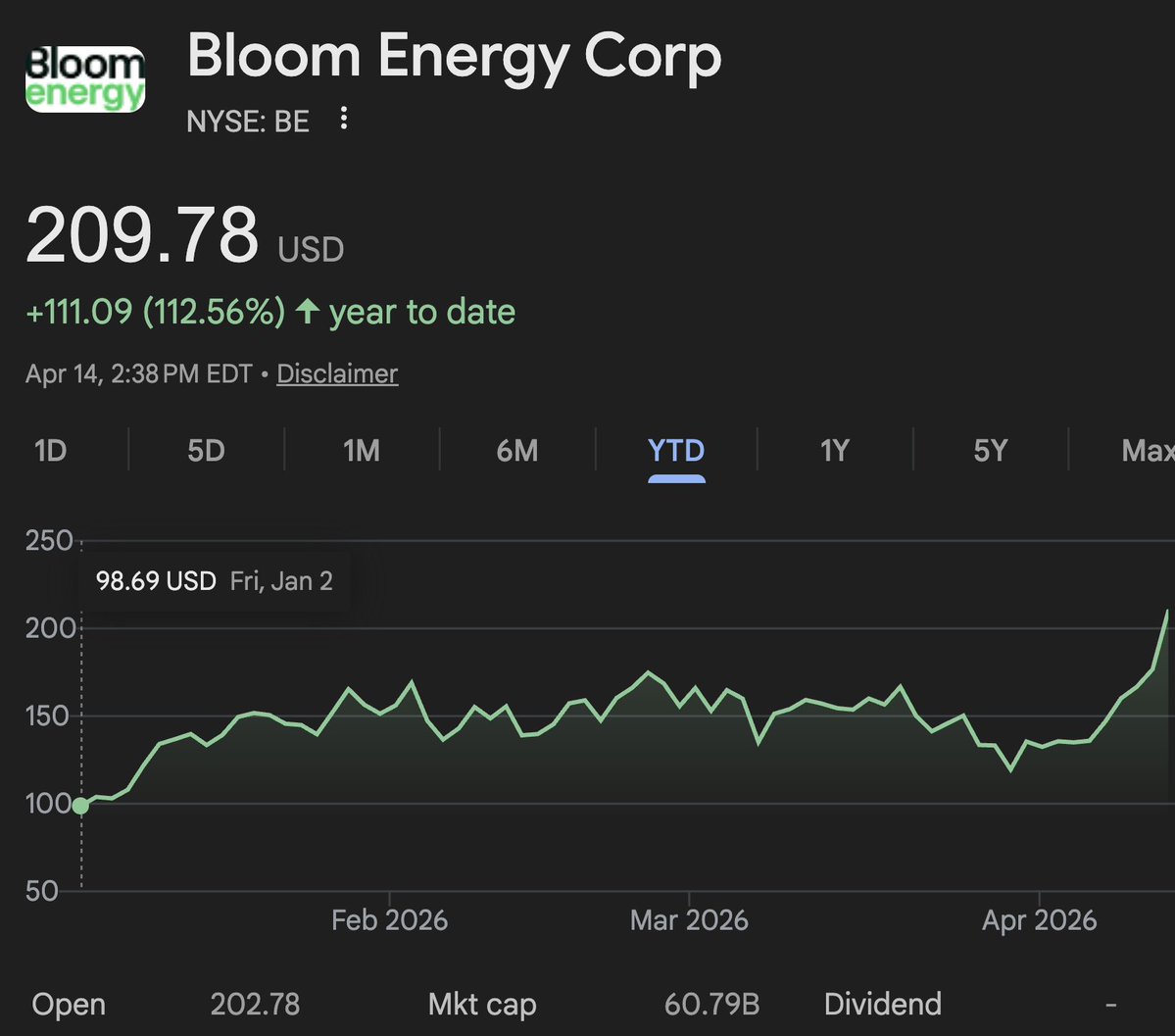

$BE got 50 MW of capacity for Oracle installed in 55 days I found the exact site using public filings and the facts are clear Engines/turbines will remain the status quo BUT permitting still takes a year. Add in backorders / install delays. 50-90 days to power is INSANE.