Web3Thug 🔺@Web3_thug

Another neo-bank project just dropped and honestly, it's yet another sign that this is the hottest narrative in crypto right now… and it's probably going to stay that way for a while. Here's why.

On-ramping and off-ramping crypto has always been a massive pain point. I remember a time when it took me four exhausting steps just to spend my crypto on something everyday, like paying for an X subscription.

First, I'd send funds from my self-custody wallet to a CEX.

Then, do a P2P trade to get fiat into my local bank account.

Next, I'd physically walk to a bureau de change to swap that fiat into physical dollars.

Finally, I'd head to the bank to deposit those dollars onto my dollar-denominated card only then could I actually pay online.

Why all this hassle? Our local currency cards were blocked from international transactions, so only dollar cards worked and you had to source the dollars yourself.

At every single step, I was bleeding money through spreads and fees. Brutal.

That's exactly the problem neo-banks are stepping in to fix. They're solving real pain points in the crypto experience, and the business model is genuinely solid. A good number of these projects with serious, committed founders will thrive.

But here's the catch: not all of them will share that success with their token holders.

What do I mean? Tokenomics is EVERYTHING.

You can have the most perfect product-market fit in the world, but if the tokenomics are trash, it's a terrible investment for your portfolio.

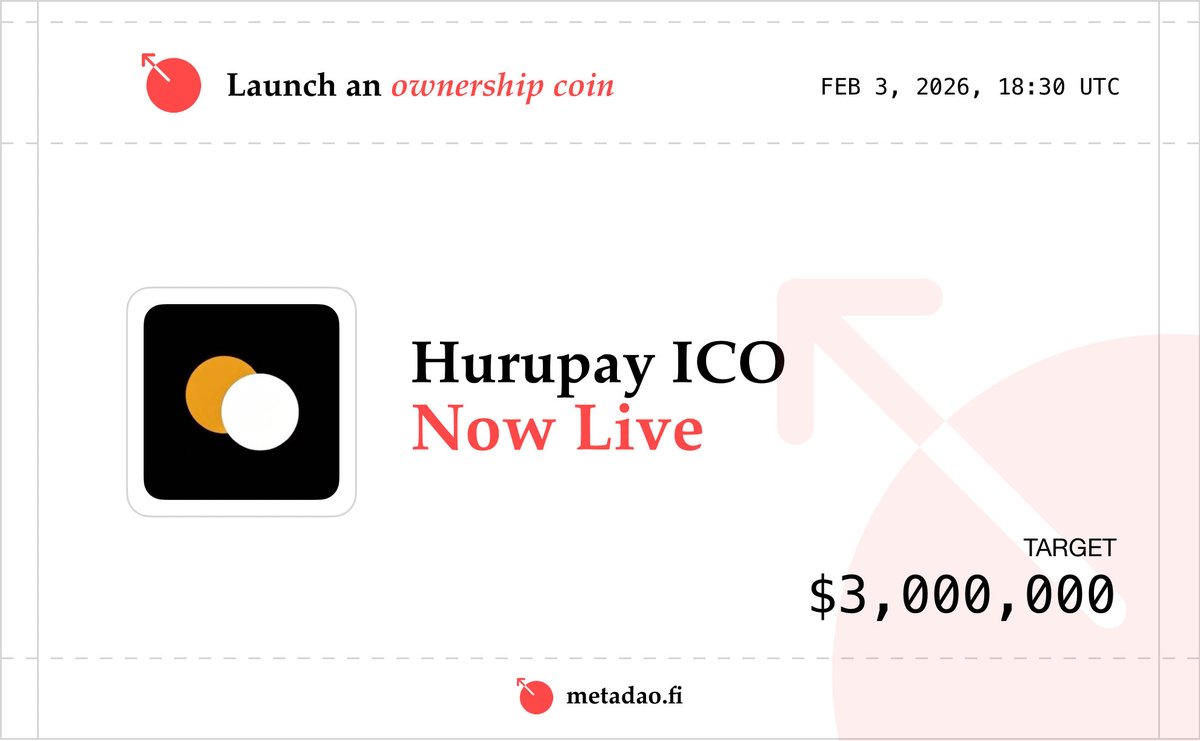

Just yesterday, someone asked my take on @HurupayApp. My immediate response? "Terrible tokenomics" especially when you stack it up against Avici's structure.

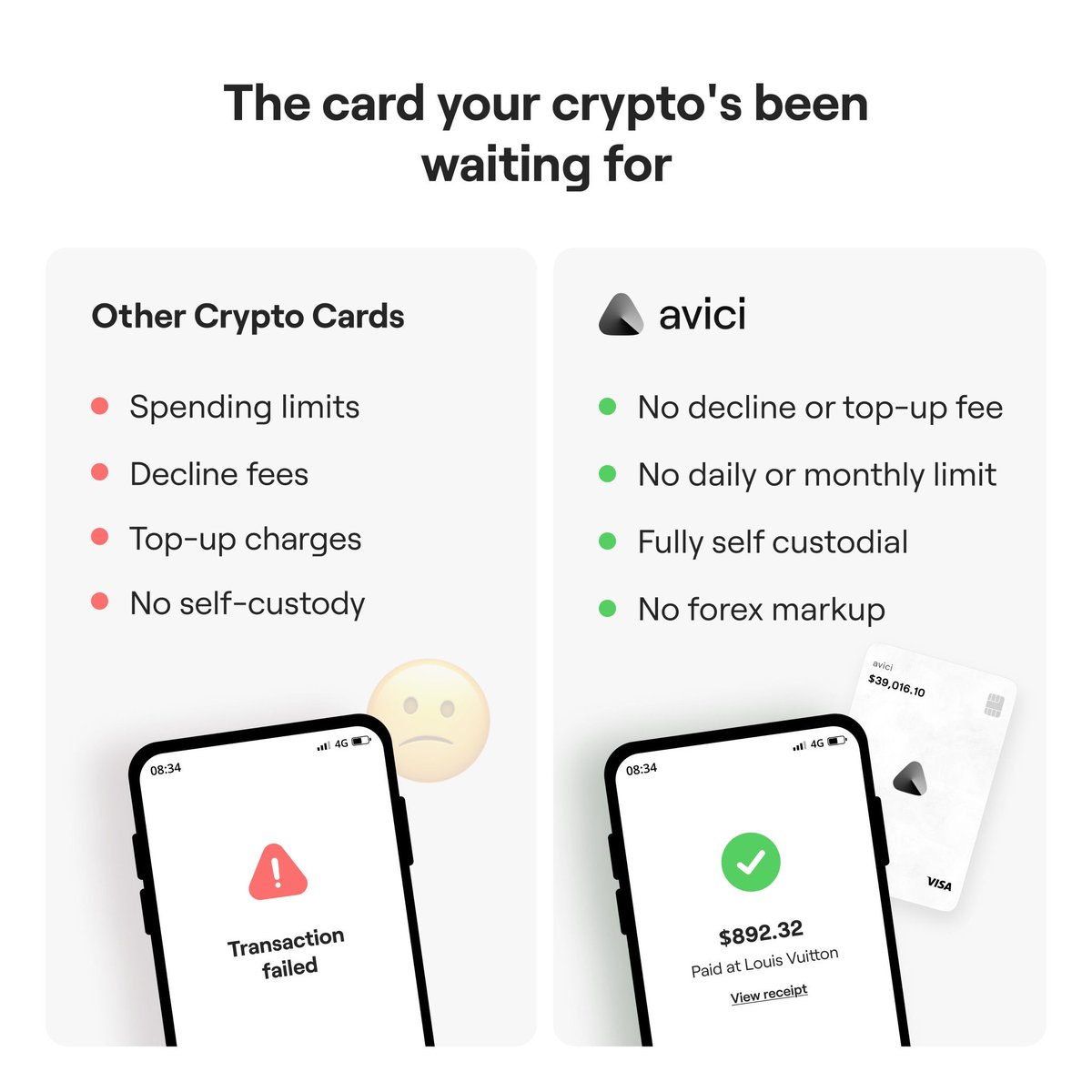

Avici's convex payout model is a masterstroke. Everyone has skin in the game especially the founders. If the team doesn't deliver results, they don't get their tokens. No free rides. That's the kind of alignment we desperately need.

$Huru shows promising early traction and solid product-market fit, decent onboarding, real users but I'm really bothered by that 50% supply unlock over three years with zero milestones or performance tied to it. Time-based unlocks like that need to go. Replace them with performance-based ones. Full stop.

Some people say Avici's team @AviciMoney took the structure to the extreme. I agree 💯 and that's exactly what this space has been crying out for. They've raised the bar so high that only the truly legit, competent, and ambitious teams will even try to clear it.

So it's simple: either you're here to build long-term value, or you might as well go home.

I genuinely welcome every new neo-bank entering the space. Bring innovation. Make crypto easier, cheaper, and more usable than when you found it.

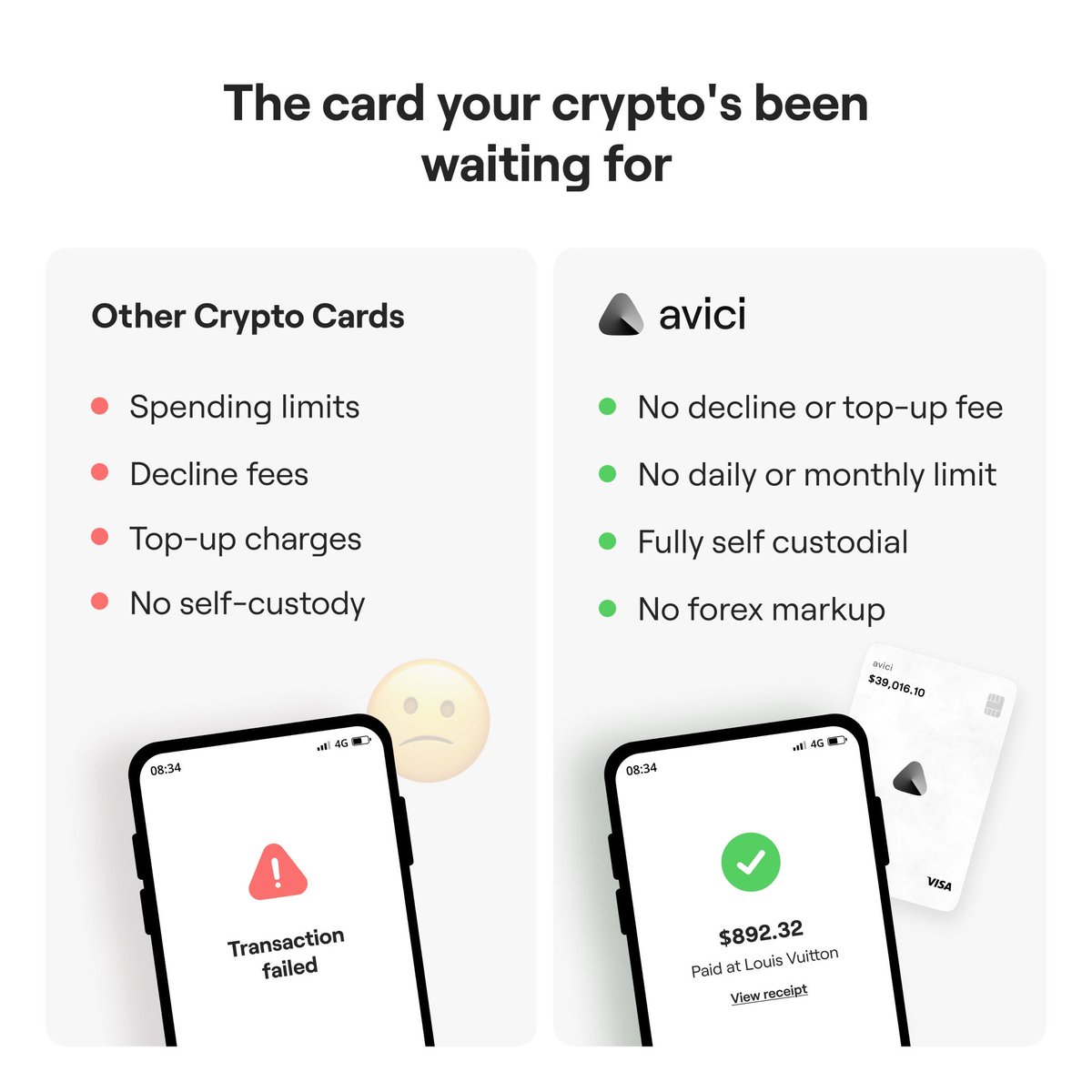

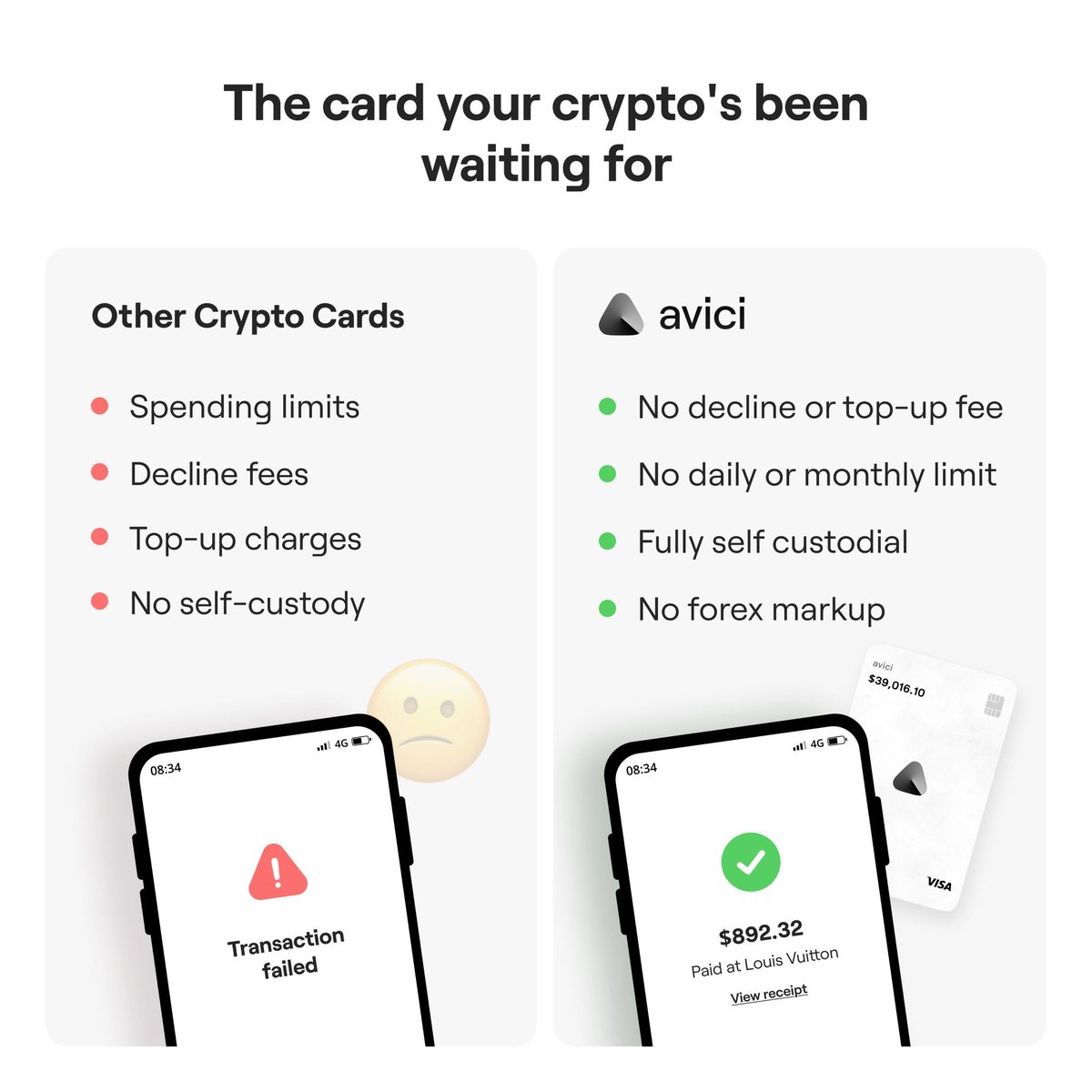

Quick tip, though: $Avici is already delivering 0% FX markup, 0% swap fees, 0% on-ramp fees, super-low ATM fees (zero for their Signature Card), and no sneaky hidden charges.

Game on. Let the competition begin…