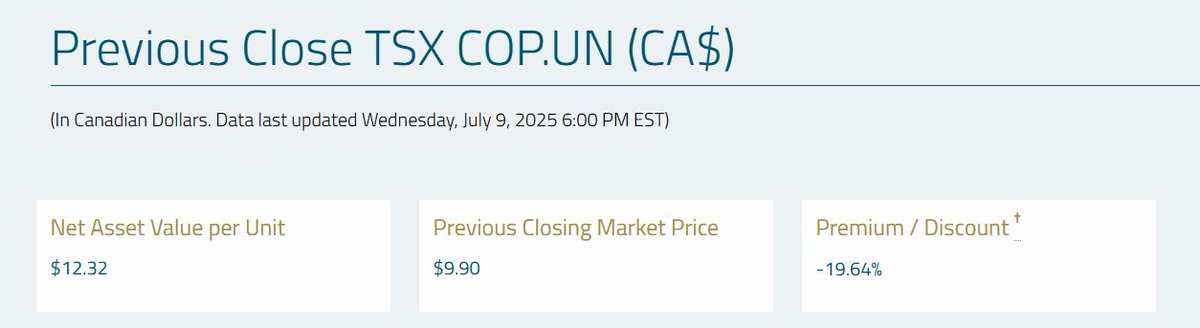

固定されたツイート

Hubon

102.4K posts

@acemaxx @bpolitics is this total China EW sales and total German car sales?

English

Last month, #German automakers saw how a sudden halt in #chip supplies from #Nexperia, a Chinese-owned firm based in the #Netherlands, could disrupt production within days — a crisis not yet fully resolved, chart @bpolitics bloomberg.com/news/articles/…

English

@InvestmentTalkk @valuedontlie History and finance?

Carlota Perez, Technical Revolutions & Financial Capital

Català

Why must there always been a deep constant reminder of deep pain? One leaves another takes it place. I don't know where I stand and I assume that means I don't really have value. I can't keep being exposed to this one. I'm going to end up hurting myself in a way irreparable.

English

English

I’ve said this many times before: a good volatility trader is never always long vol or always short vol. It’s one thing to manage a book with a directional bias, but markets are far too dynamic to approach them in a one-dimensional way on every single trade, every single time.

To succeed in the space, you need to be able to generate returns when volatility rises and when it falls. The issue is, you’d be surprised how many people either don’t care or lack the basic understanding to implement what’s outlined in the original post—something so simple, yet it significantly reduces the risk of a blowup when outlier events inevitably occur.

Yes you get paid to wear risk, but then there’s smart risk and absolutely dumb risk.

Take these two scenarios, both involve selling vol, but they’re fundamentally different.

Scenario 1

After a minor vol spike, the market is holding a significantly elevated volatility risk premium (VRP) relative to what realized vol is currently showing. I don’t believe realized vol will reach the levels we just saw, and VIX puts are now trading at historically cheap levels in implied vol terms. Given that, I want to buy an at-the-money VIX put to profit from the front of the term structure compressing.

Scenario 2

I have a target return I need to hit, so I sell volatility purely to collect theta, regardless of whether vol is cheap or expensive. VIX might be in the low teens, but I’m comfortable selling VIX 50 calls because I don’t believe it’ll ever get there. I’m okay selling 5% of my NAV in premium each month to meet my income goals.

Both are technically selling volatility, but the motivation, risk profile, and edge behind them are drastically different.

LUMILOZ@lumiloz

@noelsmith Always buy a 2 delta to sleep tight.

English

@PloutonCapLLC In other news, you have to watch this documentary on Uranium. I think the US is still importing from Russia, despite it was forbidden in 2024. Really awesome documentary.

youtube.com/watch?v=Hy4QGr…

YouTube

English