Noel Smith retweetledi

Noel Smith

9.2K posts

Noel Smith

@NoelSmith

Institutional Investor, Market-Maker/Floor Trader, 20+ years. Founder of Chicago Options Market-Making, Prop and HFT firms at the CBOE & CME | Board Member

Lake Tahoe | No Advice Katılım Temmuz 2020

2K Takip Edilen13.2K Takipçiler

@NoelSmith Gorgeous. Looks like Lake Tahoe.

English

@toiletkingcap stopped only by a well-fitted flapper (no jiggle, of course).

English

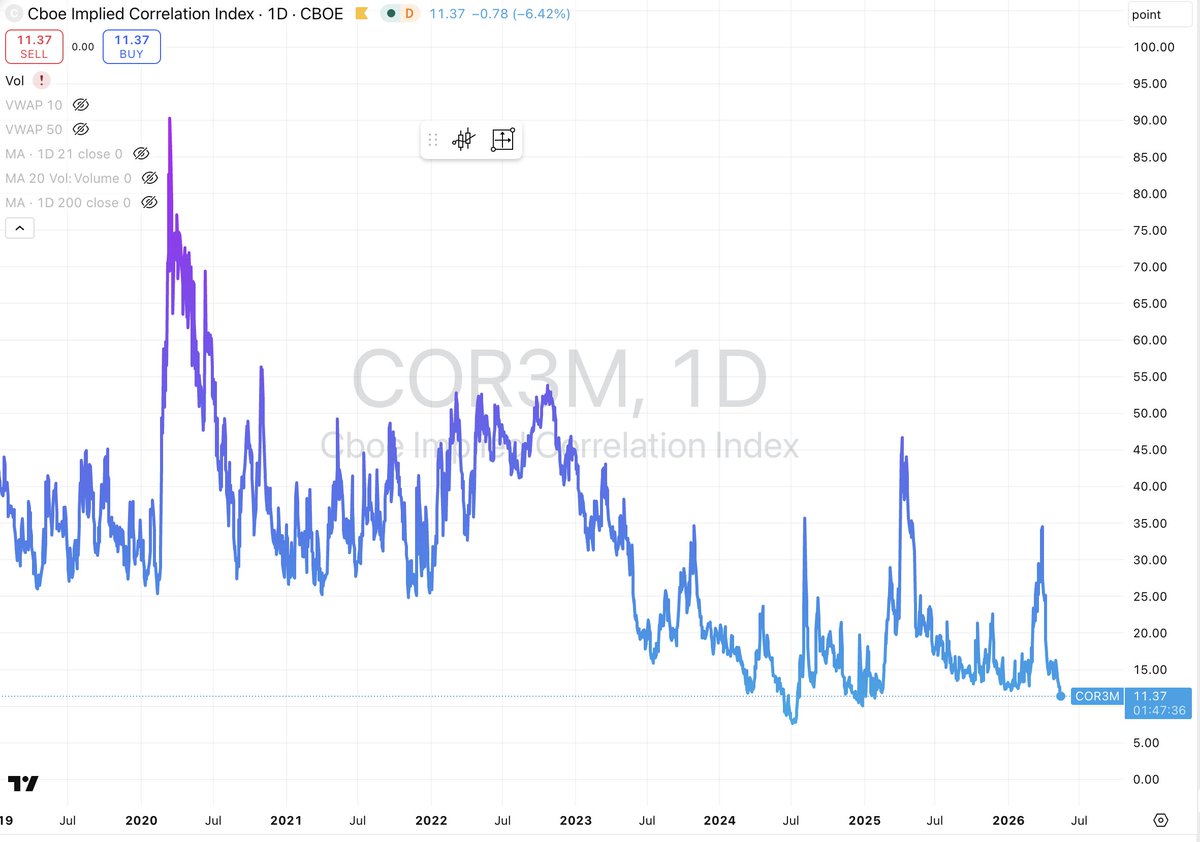

As a rough proxy for a traditional dispersion p&l you can look at the $COR3M, the lower the better.

English

@toiletkingcap I'd like to think things would go down easy and all come out in the end.

English

@NoelSmith now if someone were to sell toilets and not understand what this means, would you be willing to explain it?

English

I mean there is an actual dispersion index these days (DSPX). COR3M is not a very good proxy

Noel Smith@NoelSmith

As a rough proxy for a traditional dispersion p&l you can look at the $COR3M, the lower the better.

English

Noel Smith retweetledi

Noel Smith retweetledi

Noel Smith retweetledi

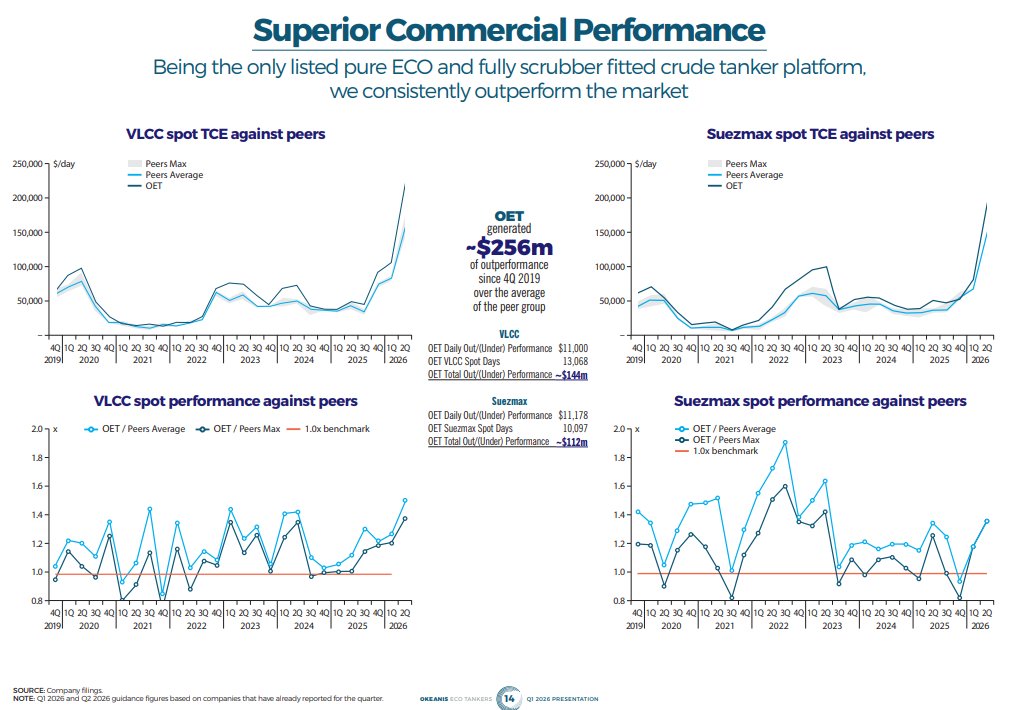

An observation: investor enthusiasm for tech earnings vs. commodity/resource sector earnings.

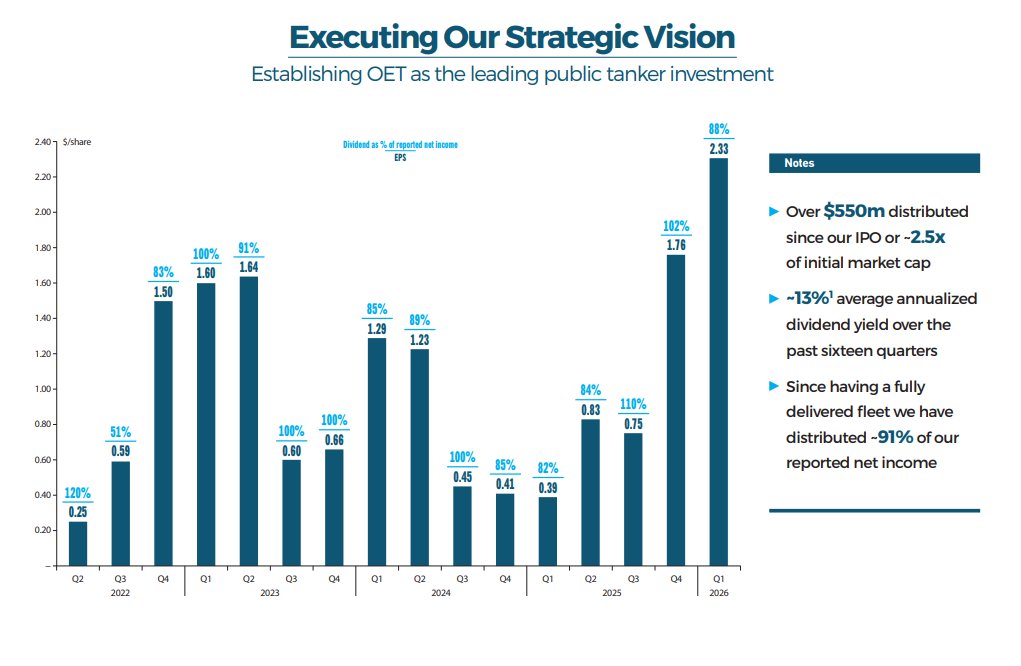

Nice quarter from $CSCO. Revs of $15.8B beat by 1.2%, EPS of $1.06 also beats by ~2%. Guide for next quarter +6% sequentially on revs ($16.8B) and +10% on EPS to $1.17. Dividend of $1.6B, for quarterly yield of 0.4%. Stock trading up 15% aftermarket.

What if $CSCO’s guidance for next quarter suggested sales +44% and earnings +110%? And then declared that their Q1 dividend, instead of $1.6B (1.6% annualized yield), would be $15B (15% annualized yield)? And that next quarter’s dividend was tracking towards $35B (35% annualized)?

Note: Those dividends would be rather hard to achieve for $CSCO, as it would require them to pay out 95% of current Q REVENUES as a dividend, and 208% of next Qs REVENUES as a dividend.

That’s what $OET $ECO just did.

Stock is trading flat/+2%.

Not a recommendation. Just an observation. Do your own DD.

English

I'll be at the @EQDerivatives conference in Vegas next week, feel free to say hello if you're there.

English

This game has transformed my life, my family’s life, my friends’ lives, and even the lives of my future grandchildren. For that, I am eternally grateful to God for the success He has given me.

At the same time, make no mistake, this game is one of the most cancerous and dangerous in the world. It can ruin and cripple you financially, socially, psychologically, and emotionally in ways you cannot imagine.

If you are playing this game at the highest level, not casually investing, you have to be willing and aching to answer its call at every second of the day. And honestly, monetary advancement alone is not enough to keep you in it. Something has to be socially wrong with you to be obsessed in a way that is difficult to even characterize. You have to be obsessed with solving this puzzle every single day.

If that is not you, it is probably a better choice to avoid it entirely. Very similar to mishandling an AK-47, small mistakes in this game can be life altering.

For my fellow lunatics, another day, and into the fray we go. Blessings and love your way 🫡

English

Noel Smith retweetledi

Here's a good way of appreciating how much diversification is priced into the options market.

The scatter plot shows the level of the $VIX versus the VIXEQ (the single stock VIX, calculated from option prices on NVDA, GOOG, MSFT, AAPL, etc.).

The VIX is always lower than the VIXEQ because on any given day, some stocks rise, some fall in the SPX, reducing the overall level of volatility at the index level. The question is how much lower should it be.

The white star shows today's level of 18.4 VIX and 44.5 VIXEQ.

Two questions. First, historically, what level of VIXEQ has coincided with today's VIX level? The blue dot shows, for example, that in early 2022, a VIXEQ of 35.3 coincided with the same 18.4 VIX we see today. Single stock volatility was nearly 10 lower to get the same VIX.

Next question, when the VIXEQ was at today's level, where have we historically seen the VIX? The second blue dot shows that in Oct'22, a VIXEQ of 44.6 saw a VIX of 30.1, nearly 12 higher than today.

The ratio of the VIXEQ to the VIX maps directly to the 1m implied correlation (IC) on SPX options (second chart, IC is inverted).

All of this makes sense in light of the low correlation between stocks like GOOG, MSFT and NVDA. A risk would be that this never seen before level of return dispersion stops.

English