Public markets love a benchmark. That’s why the smartest private companies are using secondaries to shape their IPO before they file.

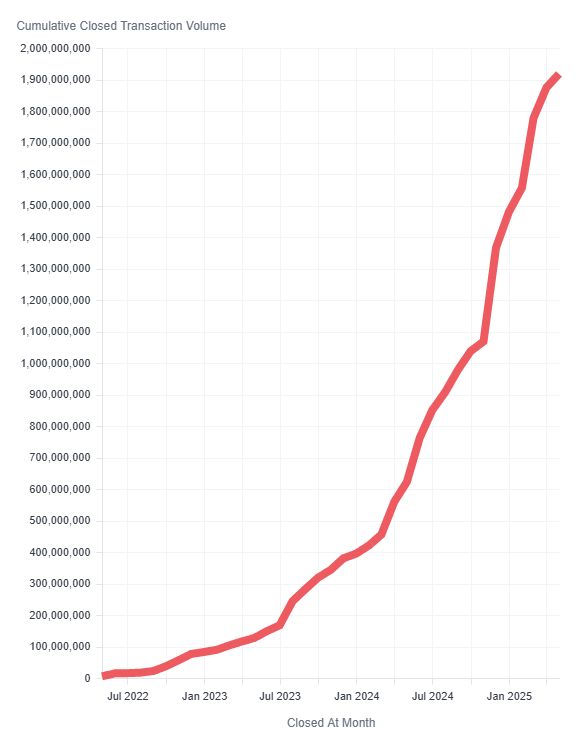

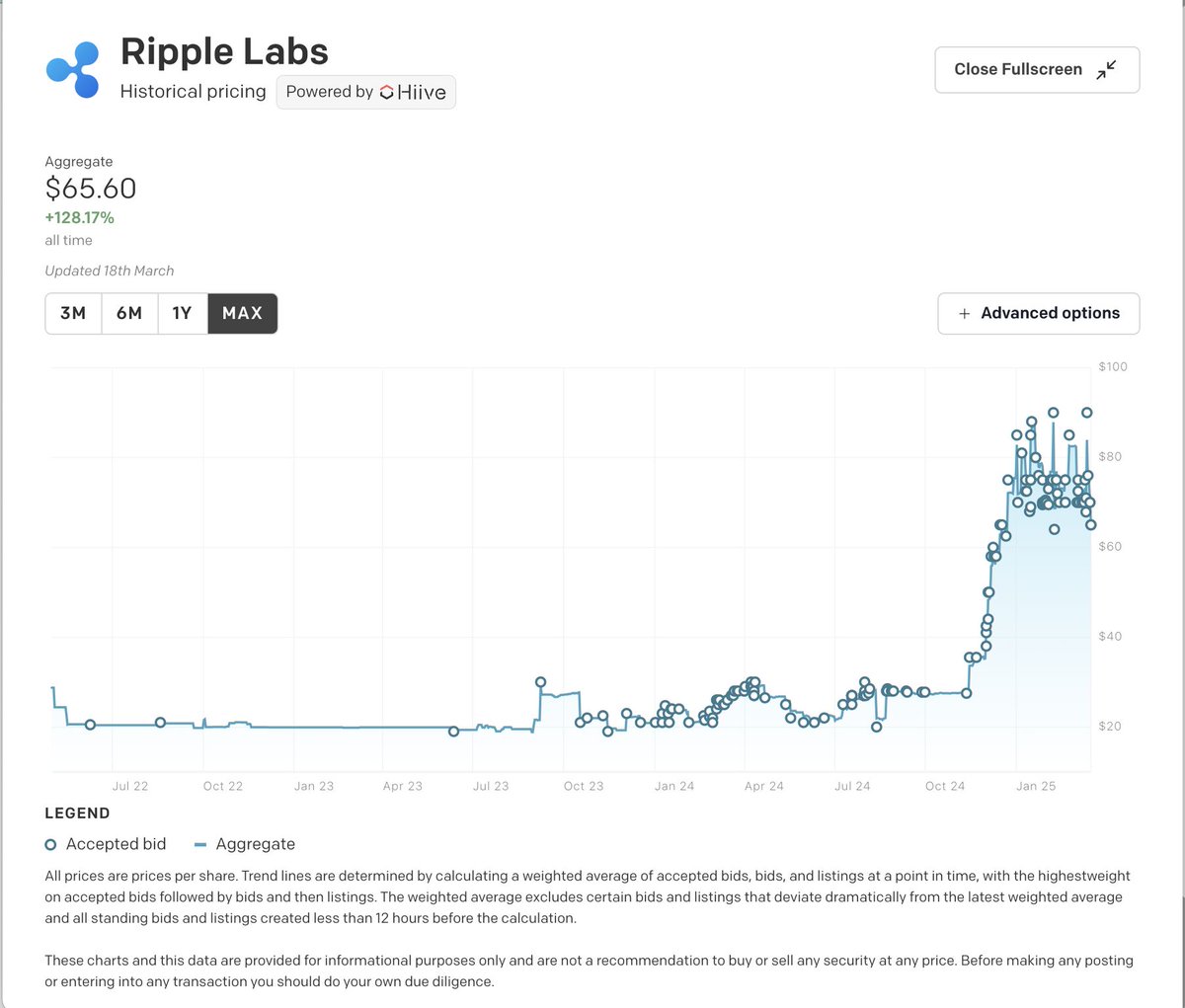

These charts show the trading histories of @rubrikInc and @Chime on Hiive, their IPO prices, and their closing prices a few weeks post IPO.

In both cases there was meaningful, controlled secondary trading ahead of the IPO. Not fire-sale liquidity. Not hype-fueled bidding wars. Just real price discovery: buyers and sellers aligning on value over time.

Instead of the roller coaster ride many companies experience upon going public, it’s easy to see the market already had an understanding of the intrinsic value these companies had, possibly due to the secondary trading both companies allowed on @Hiive_HQ (and other platforms).

That process does more than move shares around. It actually builds structure into the market:

→ A trading range emerges, anchoring expectations

→ Overhang gets absorbed, further reducing day-one downward trading pressure

→ Cap tables consolidate, improving post-IPO float quality and providing confidence to new institutional investors

In other words: secondary trading becomes a quiet rehearsal for the main event, providing the market with information it never had before. This isn’t anecdotal anymore—it’s a repeatable pattern. And it’s rewriting how companies think about IPO prep.

Liquidity is no longer just a late-stage employee benefit or investor pressure valve. It functions as a pre-listing signal, a market primer, and a cap table optimization strategy—especially for companies planning to list in the next 6–18 months.

As the IPO window cautiously reopens, this may become a defining feature of the strongest offerings: companies that went public with a price, not just a guess.

#liquidity

English