$CPKR is my top holding. $MFI spin-off at a bargain price. Following its IPO, large funds have been forced to sell, leaving its current valuation as follows:

PE=4.06

P/FCF=3.75

EV/EBITDA=2.41

Div. Yield=5%

Compare with similar companies: $CRWK, $JBS, $MFI, $SEB, $PBH, $TSN, $288

@h79sharesunder 400 miljoner Euro till återköp och en krossad konkurrent samt att man kanske tänker till nästa gång man försöker dra konkurrenter i leran utan rim och reson. Någonstans måste man sätta gränsen även om det kortsiktigt gör ont.

@idafegonzalez@Francis02351452@ID_Research_ También va a haber más ringfencing en Europa de lo que dicen, ya se vio en el 4Q. La visibilidad que tienes de los beneficios de la compañía es 0 y por eso seguirá bajando el múltiplo...

@idafegonzalez@Francis02351452@ID_Research_ El efecto divisa ha sido negativo cada año, y es el resultado de vender a agregadores en Asia en monedas como el KRW, algo que por supuesto nunca saldrá en las cuentas...

Era lo más sensato.

Siempre lo he dicho en esta tesis de $EVO:

Si me equivoco, el error habrá sido confiar en gente que es idiota 😂

Todo ha estado siempre alineado para que el management tomará decisiones lógicas y que beneficiaran al accionista.

Con esto me demuestran que tienen dos dedos de frente y que no estaba equivocado en confiar en ellos 🤷🏽♂️

Ya solo falta que vuelva el crecimiento (lo espero para el Q2 o Q3) y que solucionen los problemas de Asia.

#tpk#travis Perkins

Results were not spectacular but showed slowing sales decline and a reduction in net debt

Headwinds will persist in this company which makes very little money on their revenues and has a low roace

A mild recession followed by a reduction in construction

Interesting to see recently listed EU defense small caps Gabler $X4K and Vincorion $V1NC not participating in the recent sector rally.

On the other hand, nobody knows them yet.

Both rapidly growing, profitable, good b/s, decent valuations.

Doesn't matter whether Trump will exit Nato or not, EU defense has a LONG way to go. You'll probably do well over the next decade even from here owning a basket.

@RTOMCapital Totalmente de acuerdo. Un chollo a precios actuales. Le ha afectado que Lottomatica salió a cotizar en un bull market de gambling y Cirsa todo lo contrario (mira Flutter, Entain...un desastre), pero los fundamentales están intactos y los beneficios son muy estables

🎰 $CIRSA | Blackstone vende un 3,6%

Colocación acelerada a €12,75 (-6,4% sobre el cierre). Coordinadores: Barclays, DB y Morgan Stanley.

El descuento no es debilidad. Es el precio de entrada que pagan los institucionales para absorber un bloque en una noche.

Lo que importa:

→ Blackstone sigue controlando el 74%. No es una salida, es gestión de fondo.

→ El free float sube al ~25–26%. Más liquidez, más inversores institucionales elegibles y mercado calentándose.

→ Fondos cualificados han comprado a precio de mercado. No hablamos de minoristas, sino de fondos que han hecho su due diligence y han dado por bueno este precio como suelo técnico.

El playbook sigue su curso. Tesis intacta. 🎯

No descarto ampliar posición por debajo de 13€.

@InflexioSearch They have a restructuring plan driving $4m of opex savings and that's in the EBITDA guidance. They also said the Betcity revs are low margin. So when guiding to 0-3m improvement to 2025 EBITDA, is there any underlying improvement ex RX savings?

6/ given the depressed valuation, both financial and strategic parties would be interested. Matevz is a willing seller, and has been for a decade now. If they put up a few good Qs and show product momentum, this could easily sell for $5.00 USD + using 6x this year's EBITDA.

1/ $BRAG Lots of good stuff happening under the surface. Betcity is now 15% of revenue, down from 45% at its peak 3 years ago! Meanwhile both Brazil & US now represent over 20% of revenue growing 40-50%+. Despite a big anticipated decline from Betcity exiting in May...

@huntforcatalyst@Putxo92@cosasdedineros Si, pero ten en cuenta que el sharpe mide el riesgo en función de la volatilidad. Mayor volatilidad ~ mayor riesgo. Eso es un concepto teórico muy discutible. El riesgo real no es la volatilidad, sino comprar caro pensando que estas comprando barato…

📊 Rentabilidades YTD (€):

• Azvalor Internacional: +22,44%

• S&P 500: -5,05%

• Nasdaq: -6,40%

Impresionante lo de Azvalor en lo que llevamos de año, tras un 2025 ya muy sólido (+19,5%). Todo apunta a una rotación con un timing casi perfecto: la guerra de Irán ni la han olido. Están en máximos históricos 🚀

Este es el típico momento en el que entra el inversor amateur, al ver que su vecino esta cosechando una muy buena rentabilidad. Pero no es el mejor momento. 🚩

El mejor momento fue cuando nadie los quería, cuando los llamaban “Tenvalor”, se decía que el value era un timo y que esto era “un cambio de paradigma”.Ahí es donde se construye la rentabilidad: con convicción en la filosofía de inversión 💡

@huntforcatalyst@Putxo92@cosasdedineros Desde 2016 a mi me ha hecho un 14,75% cagr, el fondo estará entorno al 14% o así. Sharpe últimos 12 meses 2,27 a 3 años 0,90

@PerpetualValue Well, they could have put the company for sale 1 week before, and their share plan would be worth even more. I think they played legitimately

Working in finance makes you skeptical

Otherwise you'll be fleeced

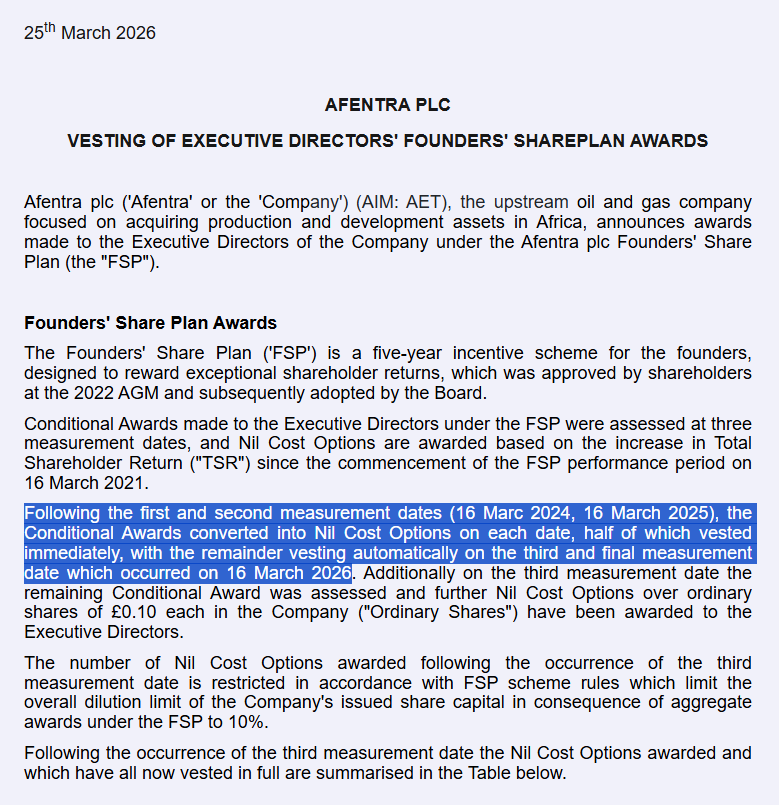

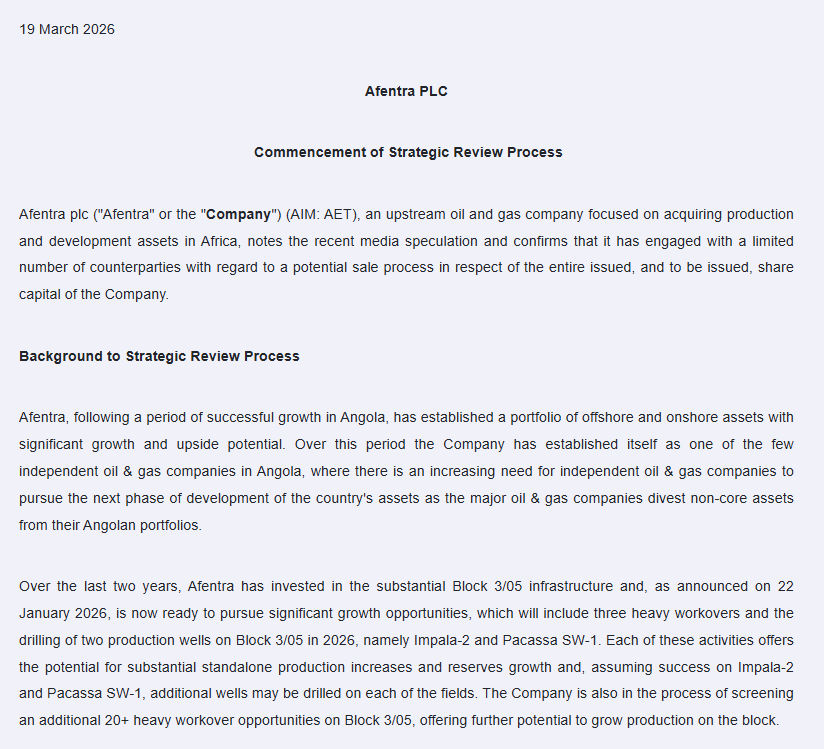

Is it a coincidence that Afentra's #AET Founder Share Plan crystalized on March 16, and then the Company was put for sale on March 19?

Did the management lose interest in building further?

$CPAC interesting situation premarket. Holcim announced they are buying 50% at a S/5100m valuation. Roughly S/1500m in net debt. Do your own homework, but I think that implies about $12.50 / ADR. I believe that under Peruvian law a tender for another 25% is mandatory.

Fuck it I might go in on the home builder that is trading for half of book.

2 year holding period at most

Size 3-5%. I don’t run that kind of book anymore

Otherwise I would size it to maybe 10-15%.

What changed Nyan’s mind?

Housing listings going HOT NOW