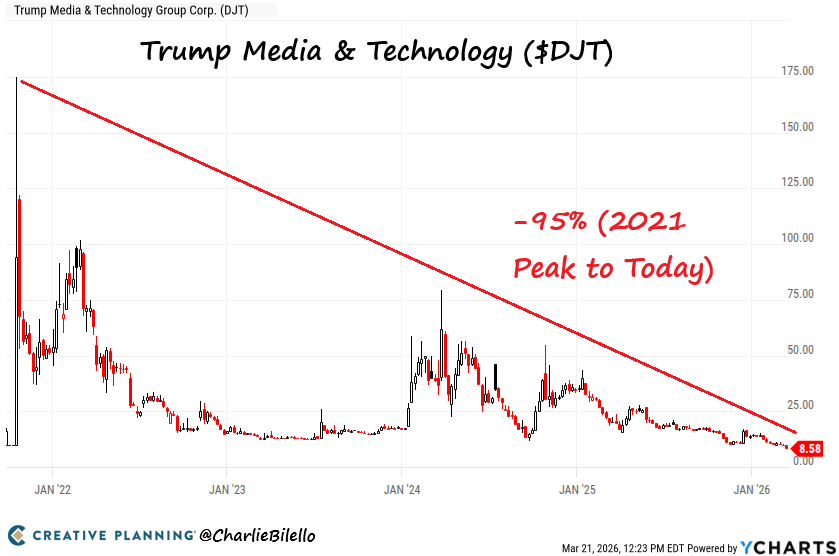

@CoachMacHTX @charliebilello You missed the minus sign

English

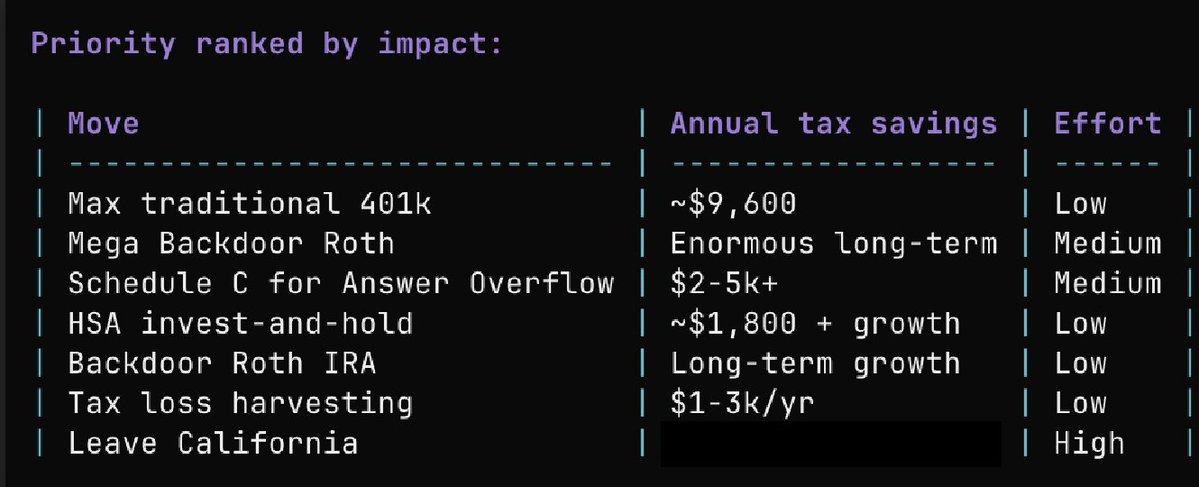

Ryan Odom | Personal Finance

5.3K posts

@ryanmarkodom

💰 Helping Solo Business Owners and High W-2 Earners Plan/Save on Taxes ⭐️ Ex-Financial Advisor 👨🎓 Free Course with 12 Tax Saving Strategies⬇

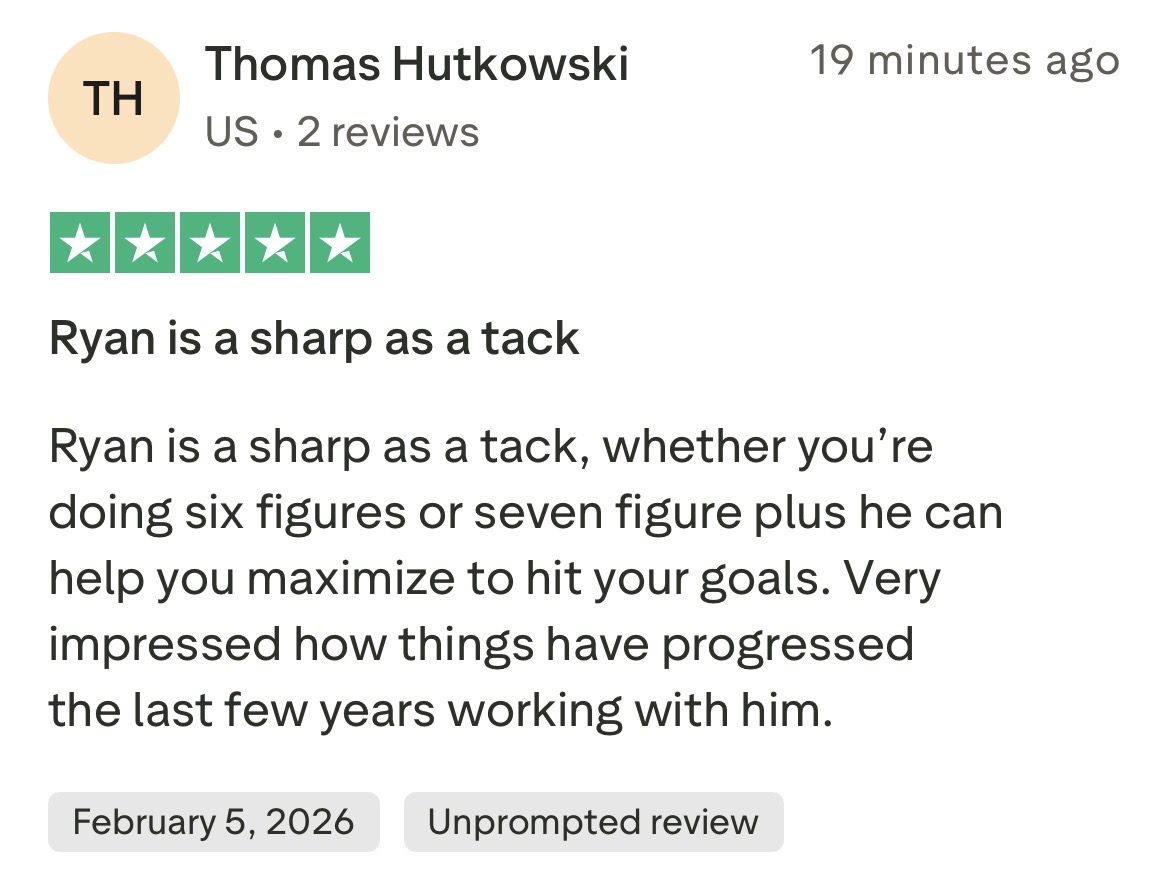

Name a job harder than this

Torrey Pines High School just emailed parents saying “there has been significant conversation on social media” about the suspension of a conservative student who posted a sign reading: “We ❤️ ICE ~ Real Americans.” Yet “ICE is KKK” is allowed on school property. The school claims no discrimination

LAX bosses approve steep fee hike on rideshare companies to curb airport congestion trib.al/TXCflir