@absforeever @ethena @AbstractChain Both apps on abstract and MegaETH are just shitty gambling games, abstract has even more stupid NFT scams

English

rmL

55 posts

@0xLRM

MEV bot feeder, gwei optimizer || prev @Citadel @UChicago

MegaETH, Ethena, and $400M Ethena built USDM for MegaETH - a stablecoin backed by tokenized US Treasury bills yielding 3.7%. The partnership happened largely because of the hype around the network As part of liquidity bootstrapping, Ethena minted $400M USDM, generating around $12.5M in annual yield for MegaETH. That revenue will cover network operating costs, bringing gas fees close to zero, and fund $MEGA token buybacks The low-gas idea is interesting, but it raises a question: where's the actual technological edge of MegaETH's super-centralized sequencer if the network has to subsidize gas? As for the buybacks - that's a trap for investors. No buyback program will offset the selling pressure from token unlocks I don't see a long-term future for MegaETH. Once the hype fades and stagnation becomes obvious, Ethena will pull that $400M out Abstract, on the other hand, has missed a real opportunity. In a year and a half, the team hasn't built anything like a native yield mechanism for users - despite it being a perfect fit for consumer crypto. A lot of that comes down to an early mistake of ignoring DeFi Right now, Ethena has no reason to partner with Abstract - there's no liquidity, no attention But with Project Quantum and other initiatives in the pipeline, Abstract will have its chance - and I hope to see native yield for users materialize, whether through a partnership with Ethena or their own implementation. @0xCygaar

Hope MegaETH succeeds: Mega still targets crypto natives with CT cultured marketing, airdrop terminal, token allocation to core communities etc. While Tempo, Canton and other corpo-chains target institutions, payments RWAs while totally sidelining crypto natives. If Tempo or Canton does well, does an average CT person profit much? Nope. Mega is our opportunity.

The existing financial system neither reflects the culture nor addresses the economic realities of this upcoming generation of financial participants. Our team, composed of emerging market citizens and perma-online Gen Zers are here to build the financial operating system for the internet-native generation. We’ve spent the past two years building MegaEVM, the fastest execution environment in the industry. The MegaEVM withstood a 11B tx stress test in mainnet production, averaging 40k TPS, while consistently charging lower fees than all others competitors. Our technical milestones paved the way for a collaboration with @chainlink to begin building the first real-time oracle, providing unparalleled speed and security to the DeFi ecosystem. The past two years has seen a notable and eventful ecosystem grow through MegaETH. Today, some of the most interesting new applications sit on Mega. The points program on Terminal has allowed crypto-native users to further explore the initial Mega Ecosystem, but we believe it has run its course. We will be providing boosted USDm rewards to all eligible participants in the program. Moving forward, we will double down on sourcing and accelerating the best applications on MegaETH through personalized GTM, targeting users beyond crypto. We are momentarily launching the MOSS SDK, a self-custody wallet that unifies liquidity between applications while maintaining top in class security through smart approvals. These pieces lay the foundation for M(OS)S to become the financial OS built for users born to this generation. Live Q3, MEGA blends finance and entertainment with primitives and risk preferences that have never been available to everyday users. The MOSS SDK is uniquely positioned to solve the embedded wallet <> generalized wallet dilemma by giving best in class security guarantees to users across all apps while still maintaining one unified account. MOSS SDK builds on the foundational work of Porto by Ithaca, providing a user-first mentality to product. We look forward to working with applications to integrate Moss and provide users with a solution to the crypto UX problem. The legacy financial system merely adopted the internet, it was not born in it. M(OS)S is being built by people who understand the culture of internet-native users and how finance, entertainment, and identity are converging online.

We’ve raised $50M led by @dragonfly_xyz to go all in on RWAs and bring TradFi liquidity on-chain. Today, we're launching Phase 1 of our RWA rollout to stress-test our infrastructure before bringing 100+ TradFi markets on-chain this summer.

果然金融到最后就是过桥 这篇 @3f_xyz 创始人 @sonyasunkim 的文章讲了RWA Looping的困境与3f目前的解决方案,有感而发,也想记录一点自己的思绪和理解: 很多人不理解Looping,觉得风险很高,但其实传统固收类资产都是加杠杆的,最大的杠杆市场就是国债逆回购。 RWA 想要在链上实现规模增长,绕不开这件事,毕竟如果不能被高效加杠杆,那机构为什么不留在 TradFi?那边的借贷基础设施已经跑了几十年,没有理由搬到一个连杠杆都做不好的链上环境。 那链上怎么加杠杆?最直觉的方式是抵押 → 借稳定币 → 买更多 RWA → 再抵押 → 重复。但这里有一个前置问题:RWA得有DEX流动性,以允许闪电贷一个 Block 里 Swap 完。 但大部分 RWA根本没有这种链上流动性。想给Tokeniznized Asset一个深度足够的交易市场,成本不低:CLOB 需要专业做市商挂单,AMM 需要给 LP 足够的激励来承担无常损失。对很多新上链的 RWA 来说,这个启动成本是不现实的。 那直接走一级市场 申购赎回呢?不好意思,跟 Crypto 原生资产不一样,链上原生资产是基于区块即时结算的,而传统资产是基于工作日的,申购赎回T+1。 ------------------- Sonya提到了目前的解法基本是两类,但都有隐性成本: 一是 Curator 管理的Looping Vault,Vault帮 LP 加杠杆。所有摩擦都由 Vault 内部消化,为了应对赎回,Curator必须留好流动性,这也意味着拖累收益,因此没有办法获得理想的杠杆敞口。 二是包装成稳定币,项目方亲自下场管理Collateral资产,坏处是可能碰到像 @StreamDefi 那样的没有良好风控,为了收益不管不顾的项目方,成为整个市场的系统性风险。 -------------------- 传统金融里面是怎么做的? 有大投行给提供专额信贷,你告诉高盛 我要 5x,高盛直接给你信用额度,一笔订单买入全部头寸,等一个 T+1 全部结算到账。建仓从 N × T 压缩到 1 × T。 高盛本质上是在资产结算之前先垫钱给你,用信用关系打断了"有抵押品才能借钱 → 有钱才能买资产 → 买了资产才有抵押品"这个串行依赖链。其实也就是所谓的过桥资金。 ---------------------- 3F 做的事就是把垫资搬到链上。 1)Bridge Facilitator:主要解决建仓/平仓的结算延迟 用户存 $100 万本金要 5x 杠杆 → bridge facilitator 一次性垫 $400 万 → 一笔交易买入 $500 万 RWA → 等一个结算周期 RWA 到账后在 Morpho 上做抵押借贷 refinance → facilitator 收回垫资 + 赚利息。建仓从 N × T 压缩到 1 × T。平仓同理。 Facilitator 赚的是短期垫资的利息:一个结算周期的资金成本。资金用完立刻回收,可以服务下一个仓位。多个 facilitator 之间竞争,利率自然趋向市场均衡。 2)Liquidity Integrator:主要解决退出端的流动性 Bridge Facilitator 把建仓/平仓压到一个结算周期,但有些 RWA 结算周期是季度级别的。用户今天想快速退出,不想等三个月。 3F 的方案是把"即时赎回"外包给专业整合商。短期 RWA 由原子 swap 提供商处理(类似 @multiliquid_xyz),长期 RWA 由专业定价商处理(类似 @FissionXYZ,根据资产风险和到期时间定折价)。用户选择:等一个结算周期按面值退出,还是立刻退出但接受市场定价的折扣。 整合商的商业模式跟 Bridge Facilitator 本质上一样,都是垫资。用户要退出,整合商先垫 USDC 给你,自己持有 RWA 等赎回结算后收回本金,赚的是垫资期间的利息加上折价差。一个垫建仓的钱,一个垫平仓的钱,都是过桥。

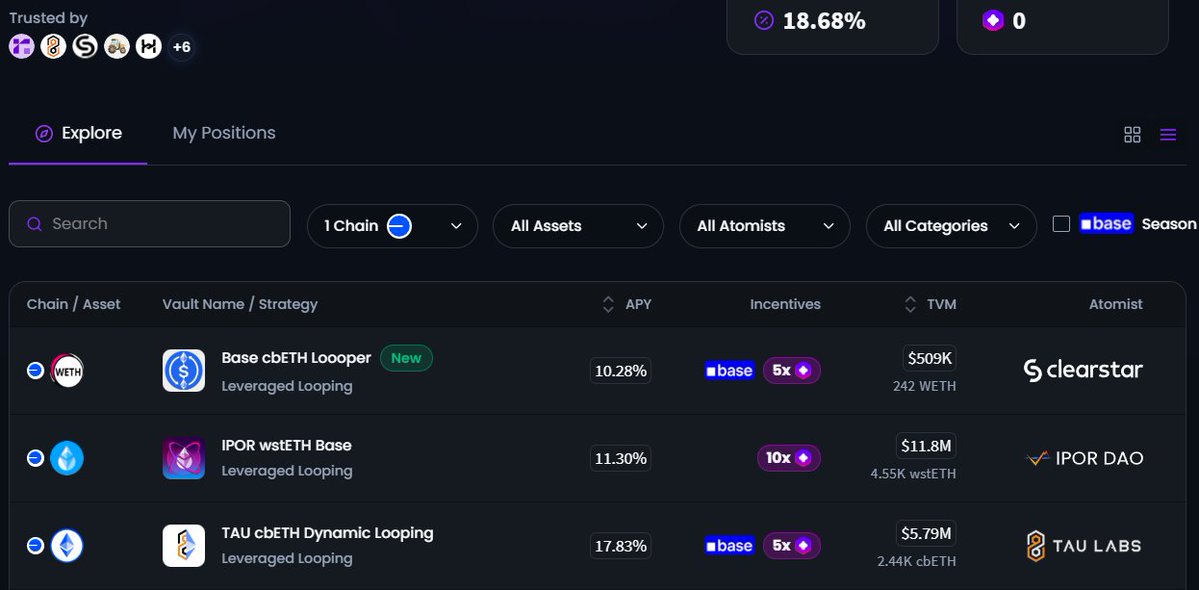

The @base season is shaping up.

This is Klaus. He could save $51,870/y by moving his loan to @LiquityProtocol How about you? Check here: rate-comparooor.vercel.app

I mean, it's just been two weeks 😂 USDm supply already down ~50% from ATH They spending 3x more on incentives just to sustain USDm TVL on Aave (per @Naeven_0) No offense to anyone who jumped to farm Mega or was bullish on it But I really think the industry has enough chains It's time for dApps like HL and Poly to lead Agree or disagree?

Been diving into the fixed-rate defi landscape for the past few weeks and trying to understand the different architectural approaches forming. Variable rates bootstrapped onchain liquidity. They cannot scale it. Institutions don't underwrite against utilization curves. BTC-collateralized stablecoin borrow rates ranged 2–16% across major protocols over the last 18 months, no treasury models against that. The market is already showing the demand: for eg, 5–6% fixed on 1–3 month maturities clearing via OTC right now (cc @MacroMate8), @Fira_Lend skyrocketing with $420M+ in loans. @pendle_fi was the early experiment here; splitting yield-bearing assets into PT (fixed) and YT (variable) tokens proved demand for fixed yield onchain. But that was a yield derivative layer on top of someone else's variable rate. DeFi wasn't mature enough yet for native fixed-rate origination, no sophisticated curator base, expensive blockspace, no proper variable-rate primitive to sit on. Three preconditions that killed earlier attempts are finally resolved: 1) deep liquidity, 2) sophisticated curators (30+ active on @Morpho alone), 3) cheap blockspace The architectural split forming now is interesting: 1) Native origination: @Morpho Midnight (intent-based ZCBs), @TermMaxFi (FT/GT token model), @loopscale (orderbook on Solana), @term_labs, @Fira_Lend, @D2_Finance 2) Solver / swap layer: @iris_credit isolating rate risk to a third party while keeping variable-rate origination 3) Collateral utility: @Cassa_fyi + @eulerfinance + @infiniFi making fixed-maturity assets usable as collateral with a credible exit path The unresolved question: asset-liability mismatch when fixed loans sit inside vaults promising instant liquidity ( @AnthonyBowman43 has the sharpest critique, altho @Crotts__ had a solid pointers on duration management). Worth noting: the variable-rate base layer is also evolving. Tranched risk tiers in connected markets like @LotusFi_, @roycoprotocol and similar concentrated-liquidity designs are building the kind of efficient variable-rate benchmarks fixed-rate solvers need to quote tightly against. The two layers reinforce each other. Writing a long-form piece on this, would love to chat if you're building or have strong views (DMs open). (p.s. threw this together with claude on a lazy sunday, happy to be corrected)

Another week of @3f_xyz private beta! Now $3.1 million of total exposure sits with the JAAA tokenized fund sub-managed by @JHIAdvisors and tokenized by @centrifuge Yesterday's 3F auction cleared the full stack. Same RWA, three risk profiles, three different rates: 🟧 Leveraged LP (8x): 21.7% APY 🟦 Bridge Facilitator: 8.95% APR overnight 🟩 Morpho lender: 3.3% APY To be continued next Wednesday!

Onchain digital credit yield is taking over @pendle_fi. 🚀