Sabitlenmiş Tweet

3Jane

260 posts

3Jane

@3janexyz

The credit-based money market. Borrow against the future. Backed by @paradigm

Katılım Kasım 2021

1 Takip Edilen16.7K Takipçiler

Levering apyx positions with 3Jane's 40% unsecured line:

apxUSD PT/YT: 92% → 149% APR

apyUSD PT/YT: 46% → 73% APR

apyUSD loop: 58% → 92% APR

6% cost of capital, underwritten against creditworthiness.

wumpy crypto@wumpycrypto

take out a credit line against your @apyx_fi holdings and see your strategies increase by > 50% APR more on strategies below...

English

3Jane retweetledi

Onchain Digital Credit yield is becoming more capital efficient. 💪

Through @3janexyz, eligible users can now access up to a 40% unsecured credit line against $apxUSD, $apyUSD, and related @pendle_fi PT/LP positions.

3Jane@3janexyz

@apyx_fi is a synthetic dollar backed by $STRC, @Strategy's ~$5B credit vehicle. 3Jane now extends up to a 40% unsecured credit line against apxUSD, apyUSD, & PT/LPT's held, using Vantage3.0 credit scores. Lever up to +18% APY on PT's. US-only: app.3jane.xyz/pull

English

@apyx_fi is a synthetic dollar backed by $STRC, @Strategy's ~$5B credit vehicle.

3Jane now extends up to a 40% unsecured credit line against apxUSD, apyUSD, & PT/LPT's held, using Vantage3.0 credit scores.

Lever up to +18% APY on PT's. US-only: app.3jane.xyz/pull

English

3Jane retweetledi

Tomorrow 5pm UTC

Join @jchaskin22 and @binji_x for Ethereum Builders Live with @_yakovsky of @3janexyz.

Hear more about how 3Jane is building a credit-based money market on Ethereum that lets users borrow without posting collateral.

x.com/i/broadcasts/1…

English

Despite ~$800k in indirect Resolv exposure across $107M+ in value verified, 3Jane would have incurred $0 bad debt even without a Fluid subsidy.

3Jane extends cross-margined, recourse credit lines underwritten against the full balance sheet rather than isolated collateral. This enables financing for a broader set of productive assets without forcing lenders to warehouse concentrated single-asset tail risk. Read more:

wumpy crypto@wumpycrypto

1/ the @ResolvLabs and @StreamDefi incidents showcase inherent risks of isolated margin money markets. lenders become the synthetic senior tranche to assets underwritten by risk curators while remaining largely unaware of the associated risk with their position.

English

3Jane has added @ether_fi assets to our credit-based risk model, enabling liquidity against >$1B in novel DeFi assets.

Access up to a 30% unsecured line of credit against $ETHFI, $weETH, liquidETH, and liquidBTC.

U.S.-only. app.3jane.xyz/pull

English

3Jane has partnered with @HypernativeLabs to add 24/7 threat detection & prevention across the protocol, helping us preempt attacks before funds are at risk.

This includes smart contract vulnerabilities, operational security risks, financial manipulation, & other attack vectors.

English

3Jane retweetledi

3Jane now offers up to a 30% unsecured line of credit against $mETH, $cmETH, $MNT, and other derivatives across @Mantle_Official integrations.

This unlocks instant liquidity across $3B+ in assets with a single integration, powered by credit-score-based underwriting.

English

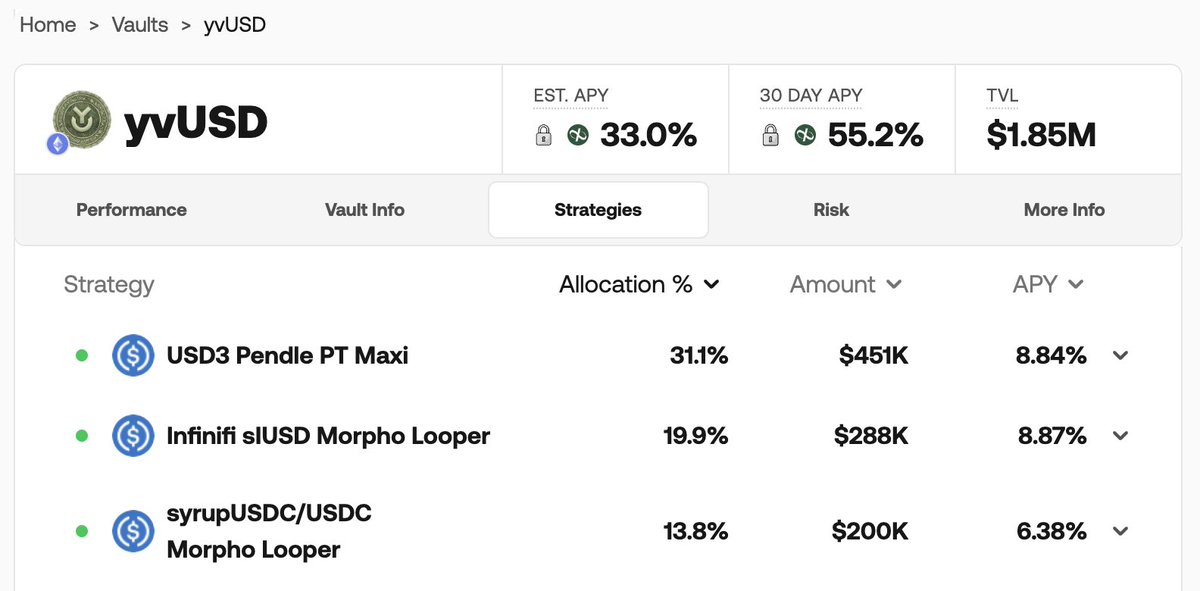

@yearnfi x @infiniFi x @3janexyz

Generating ~55% APY on $yvUSD x USD3 with a little trick the banks like to call maturity transformation.

yearn@yearnfi

Farm Everything, Everywhere all at once. Introducing yvUSD: A new cross-chain, cross-asset vault for best in class stablecoin yield. Deposit on mainnet, and let the vault optimize leveraged loops, lending, PT's and more across multiple chains, automatically.

English

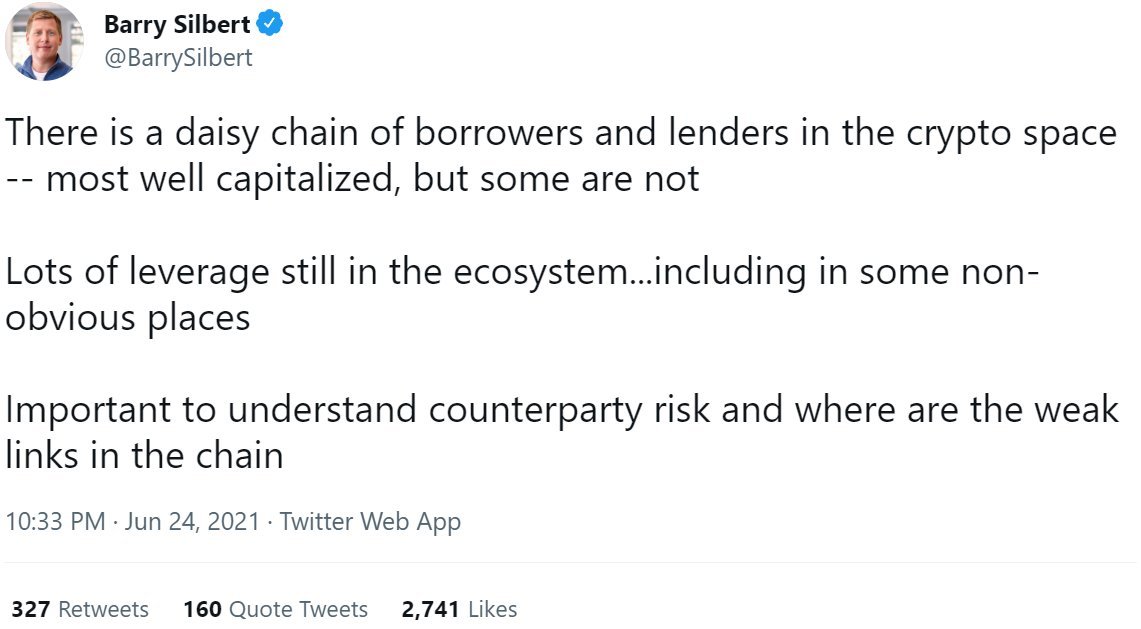

There is a daisy chain of borrowers and lenders in the crypto space -- most well capitalized, but some are not

Lots of leverage still in the ecosystem...including in some non-obvious places

Important to understand counterparty risk and where are the weak links in the chain

English

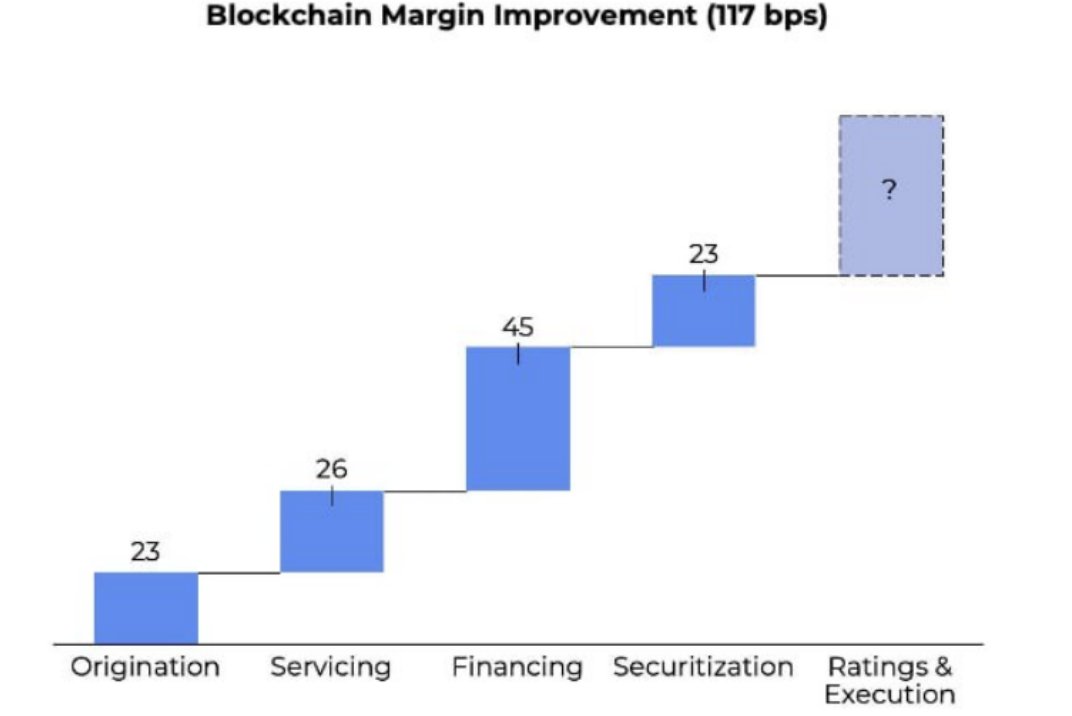

Crypto compresses credit spreads with low-overhead, programmable rails on a +$20T industry.

@Figure identified this >2yrs ago and issued a cryptonative S&P-rated HELOC securitization. Last week, Better (NASDAQ: $BETR) announced a $500M mortgage warehouse facility with Sky.

This trend will only accelerate.

PaperImperium@ImperiumPaper

Unsecured lending is still a frontier in DeFi, but it’s an enormous opportunity. The low cost of capital onchain, coupled with the automation built into blockchains and DeFi by their very nature, should make for a competitive advantage against traditional lenders (both commercial and consumer). The missing ingredient, of course, is risk management. DeFi has generally depended upon overcollateralized lending of onchain assets to skip the trickiest parts of risk management in lending. Can a liquidator instantly dump the collateral into a DEX? Are there cheap or free flash loans available for liquidators so they don’t have to sit around with idle capital? If yes to both, list it as a supported collateral. No one cares who issued the token as long as it’s marketable and doesn’t have back doors in the token contract. That’s a bit of an oversimplification, but not by a lot. But it works. It keeps credit losses low, and recovery times effectively zero. Right now, some companies and protocols are experimenting with tokenized RWAs. These generally lack secondary market liquidity, so risk management now requires underwriting the issuer of the asset. This has been a bumpy road, but things finally seem to be on a sustainable trajectory for more collaterals being eligible for the usually-low rates found onchain. Rates are usually low, of course, because DeFi struggles to originate enough debt to satisfy the demand for lending. So inevitably unsecured lending will have to become solved problem. It’s also an enormous market. In the US alone, there was about $18T in consumer unsecured debt at the beginning of 2025. That number gets much, much larger with business lending. Personally, I think consumer unsecured lending will be sustainable onchain before business lending, simply because it’s more susceptible to the Law of Large numbers. Crypto may not be great at understanding the covenants of private credit sometimes, but it has a lot of very numerate people who can deal with a large volume of smaller, granular loans to build out a risk framework. And that risk framework is important. Let’s take a look at US credit cards to understand the economics of unsecured lending. In the screenshot, you’ll see a bar chart based on 2023 data from the Federal Reserve. As you can see, DeFi can simplify a lot of this for both sides of the deal. The non-interest yield (aka fees that everyone hates) is generally not a thing in within DeFi. The non-interest expense (back office, underwriting, recovery, compliance, etc) is also considerably smaller in DeFi. If you remove those two, you already get a much cheaper product for consumers and fatter margins in DeFi. But look at that credit loss bar. It’s about 4%. And that’s kept low by a lot of those non-interest expenses, as well as legal recourse and processes to monitor credit migration (just because someone was a good credit quality a year ago when they opened their card doesn’t mean they are today). This is where DeFi has a huge hole. It’s probably the case that the non-interest expense cannot be completely stripped out without credit loss exploding. The good news is that credit losses in this graph could actually grow quite a bit and still work financially. But these things tend towards binary outcomes, since you’re dealing with large numbers of users, and any flaw in your underwriting, monitoring, and raising/lowering credit limit methodology can blow you up. And of course there’s also just things beyond your control. A borrower on Aave can lose their job and it not affect the credit quality of the loan — it just needs plenty of collateral. So unsecured is much, much more complex, even if you design it to minimize fraud. It’s a big prize though. I suspect we’ll see at least some specialized lenders coming in to use their own loan portfolios as collateral to borrow in DeFi, but the big unlock will be finding ways to screen or filter users directly at the protocol level.

English