Alan Edgett

12.8K posts

Alan Edgett

@ACEdge

CEO The Gig Agency — Just Launched https://t.co/qYs6FXUMXL an Agent Control Platform for SAAS

Irvine, CA Katılım Nisan 2008

2.2K Takip Edilen1.2K Takipçiler

@JordanSolace I like this and $usar. Thought this a good read too: x.com/ctindale/statu…

🇦🇺Craig Tindale@ctindale

English

$UAMY

Listened to the call this am.. still a good bit of execution risk but I will continue to add on dip for a few reasons..

Mkt overeacting to the loss where it’s mostly non cash.. the biz is just building/scaling.

Mark to mkt from larvotto equity & Stock comp..

Gross margins dipped from 34% to 16% bc ore is flowing thru cogs at higher Rotterdam prices while sales were a bit softer.

Domestic montana ore & DLA deliveries will fix this and 16% margins is likely the bottom.

There were $12M in orders placed for DLA that were not recognized and once these ship in q2.. that will hit the income statement.

Thompson falls is coming online in stages.. 80% nameplate targeted by July.. this will triple domestic processing capacity… Also I like the fact inventory is climbing… the feedstocks will be ready to run once Thompson falls gets up and running.

Q2/Q3 are set for big operational inflections…

Most important line of the call. The US govt wants more antimony than UAMY can currently produce.

This co isn’t chasing demand.. demand is contracted, govt backed, and exceeding supply. They just need capacity.

Gary broke down revs on the call. $75-$95M will be fed govt shipments of antimony ingots. Again. Demand is not the issue.

Btw.. this isn’t only an antimony play.

Cobalt. Gold. Tungsten. Zeolite.

Tungsten gross in ground value at $9.3B.. even when you discount this… something worth watching.

Hydromet facility is targeting half the entire US antimony mkt by 2028.

Nolan Creek Alaska.. got that asset on the cheap

Liquidity is solid.. market sees $3.2M in cash when they really have $118M pro forma liquidity.

$19M credit line and $270M in govt grant applications pending. Look thru vs snapshot is very different.

Overall… lots of non cash losses, no DLA revs, smelter is days/weeks away from being online.. govt needs more antimony than they can produce… and tungsten, cobalt, gold, zeolite are beginning to inflect… many of them not in the share price today.

English

Great stuff here if your interested/invested in $usar $uamy $arec $mp etc

🇦🇺Craig Tindale@ctindale

English

@AishwaryaDevv @Jesse_Livermore I’ve got a few client SAAS at 30-50k lines of code that were vibed (hate the word). Lovable/supa, managed by an Openclaw and Codex, but also a shit ton of my time. Hanging in there and still enjoy speed of iteration but maintenance is hard no doubt.

English

Am I the only one getting vibe coding fatigue?

Building landing pages in 30 seconds was fun, but maintaining a complex codebase where half the logic was “vibed” into existence is an absolute headache.

Feels like we traded 1 hour of typing for 5 hours of architectural debugging later. I’ve started manually writing core logic again so I actually know where the technical debt is hiding.

Is anyone successfully managing large production projects with AI agents, or are we all just building disposable software?

English

Just a lot of words of bullshit. They already had insurance and your whole pt rests on insurance not the financing. Yes, the new vehicle can be used but you had no idea THAT was the bottleneck. Note: it wasn’t. It would have been solved already if so. There is no demand for their batteries/solution.

English

$EOSE

Q1 quick reflection…

Everyone wants to know where the order is…

Wrong question. Reframe.

Eos just solved the reason big orders weren't converting in the first place.

The #1 barrier to LDES isn't technology.

It isn't demand.

It's one question nobody could answer:

What happens to our loan if the batt stops working in year 8?

Before yesterday ..nobody could answer it.

So the loan didn't happen. Project didn't get built. Pipeline didn't convert.

To understand why Frontier Power USA is vital.. you need to understand how these projects get financed.

Think about this Illustration…

Frontier builds a $50M battery storage project.

Puts in $15M of their own equity.

Borrows $35M from an infra fund or pension.

Utility pays $12M a yr for 15 yrs

That contracted revenue pays back the loan.

The lender gets paid from the cash flows. Not from Eos's balance sheet.

Infra funds and pensions WANT to lend against contracted infrastructure cash flows. 🔑

Here's why:

They need steady predictable returns over 15-20 years to match their long-term obligations to retirees.

A 5.5%+ locked in return secured against a real physical asset with investment-grade offtakers (THE PROJECT) is exactly what they need.

They have billions ready to deploy.

They just needed one thing answered first.

What if the batteries fail in year 8?

If batteries fail .. revenue drops.. loan can't be repaid … lender loses money.

Banks don't lend against questions they can't answer.

This single unanswerable question has kept billions of infra capital on the sidelines.

Enter the room Ariel Green

Lloyd's of London. Rated AA- $1.5B framework… 15 yr NON-CANCELLABLE coverage..Sized at the project level.

Their job is simple:

If Z3 batteries underperform in year 8.. the Ariel Green insurance structure is designed to preserve project cash flows for the lender 🔑

Watch what just happened.

Before TPI:

Lender asks: What if batteries fail in year 8?

Answer- We don't know

Result- No loan. Project dies.

After TPI:

Lender asks: What if batteries fail in year 8?

Answer: Lloyd's of London can pay the claim

Result: Investment grade loan. Project gets built.

One substitution. Dynamic changes.

This is NOT a performance bond.

Performance bonds cover the project getting built…

They expire at completion.

The TPI covers something completely different:

Will the batteries keep working for 15yrs

That's the question that killed LDES project finance.

That's the question Ariel Green is addressing

Now let's talk about the capital stack

200 MWh Z3 system. $50M total cost

Layer 1 Equity: $15M Frontier Power USA (Cerberus + Eos)

Layer 2. TPI wrap: $1.5B framework -Ariel Green / Lloyd's AA-

Layer 3- Senior debt: $35M - Infrastructure fund at 5.5%

Every layer serves a purpose.

Every layer is now filled.

Here's how the cash flows every single year:

Utility pays: $12M

Operating costs: -$4M (includes Ariel Green premium + Eos O&M)

Debt service to infra fund: -$3.4M

Infra fund gets their 5.5% locked in. Every year. For 15 years.

What's left for equity: 3-4M

With a small buffer probably between the infra fund and equity (escrow) but think bigger picture.

On $15M invested.

The power of leverage is unlocked by the TPI

And here's what happens if the batteries DO underperform in year 8:

Revenue drops $3M below projection.

Frontier files a claim with Ariel Green.

Ariel Green pays $3M or xyz$

Revenue restored to $12M

The infra fund is not getting *as* impacted by the underperformance.

That's insurance backed credit.

That's why lenders will now show up for LDES.

Why did ariel green write this? DawnOS

The st. Dev around RTE = insuranble risk

English

@Bjorn_Wigforss @YourAlphaTesla @PoweredByEos Even if a bot, it’s the same time of crap/abuse from the rest of this community when you accurately analyze Joe and $eose. Good post.

English

$eose

This is not a typical post from me. However, @PoweredByEos should pay attention.

Yesterday's stock price bungyjump isn't a coincidence. First we got excited about the headlines, then we started looking at the details.

To keep it as short as possible.

The trust issue is the real killer here.

Past behavior doesn't inspire confidence: multiple guidance misses, heavy dilution history, lawsuits, and repeated short-seller scrutiny that keeps resurfacing related-party and accounting questions.

Even if this technically complies with GAAP, it looks like channel stuffing to hit milestones in a pre-profit, capital-hungry business chasing PTCs and AI tailwinds.

The market's quick fade (huge volume, but no sustained pop) suggests plenty of investors not buying the "execution story" at face value when the biggest revenue chunk smells off.

Bottom line: This does feel like management papering over execution or financing gaps with aggressive recognition and related-party maneuvers. Make us unfeel it! The burden is now on EOSE to provide concrete evidence: Cash collections from that UK revenue, detailed contract/shipping disclosures, or actual Q2 delivery proof. Without that, the bear case strengthens and a "hiding the inconvenient truth" narrative will only be reinforced. We can't wait until the Q2 filings.

Comments welcome.

English

I need to talk about $KRKNF.

The small cap underwater drone stock supplying Anduril that launched my name on FinX is down 20% in a month.

From its ATH of $7.56 it's now down 30%.

Granted $KRKNF Krakheads are WAY better off than peers 🦑. In the last 6 months:

$KRKNF +41%

$AVAV -45%

$KTOS -26%

Been noticing some people have been in my comments frustrated/curious as to why I haven't been talking about Kraken as much as I used to.

So I wanted to give a quick recap and where I stand on the stock currently.

My discord went in with me at $3. My viral video hit the world at around $4. Stock peaked at $7.50/share. I can't speak for everyone's cost basis. But at $5.20 that's an S&P crushing investment especially compared to the other defense names.

I helped popularize a banger, undervalued drone stock in a super unique niche of subsea with the purest Anduril revenue exposure. It has built an incredibly passionate contingent.

The banks covering the stock, who are notoriously conservative, have price targets at roughly 2x upside from here.

Macro wise, defense has been a miserable pocket of the market lately. A classic case of buy the rumor, sell the news.

I know it sounds illogical but this is how you make money. Most retail investors would think to buy a defense stock when Trump bombs Iran or ocean mines make $KRKNF look like a hero but the smart money is selling it...

As to why I'm covering it less there's a few reasons why.

1) There genuinely isn't that much news on the stock and the defense sector isn't where the money is being made right now. The thesis is completely unchanged. Of course, I could come up with more post ideas as a morale booster and thesis reminder, but I also don't want to give the impression I'm a pumper/cheerleader to get my own bags back up.

Further, this may sound harsh, but I'm not a babysitter whose job is to manage expectations around a name 24/7. If a stock is going down with the macro I am not in control of it and can not fully explain why other than the fact that stocks go up and down. I've emphasized before that the thesis is unchanged. People are very educated on the story now and it's their decision whether they want to load the dip or chase AI infra. Everyone must do their own research and manage their portfolios accordingly. I've been posting about tons of winning ideas beyond Kraken.

2) OTC access locks a ton of investors out who can't participate, meaning a lot of this exciting story can't be shared by many people who may see the thesis but don't want to switch brokers. Because of this OTC thing too I can't add Kraken on @joinautopilot. I've developed a huge following on there ($30M following my ports, 3 of my ports 70-110% in 3 months). So people get super confused as well when I talk about Kraken and they ask why it's not in any of my actively managed funds.

3) I always made very clear $KRKNF wasn't a full port trade for me and have always covered multiple stocks. I have only ever made one video on Kraken, and have covered 30+ stock deep dives on my YouTube plus at least 6-10 stocks on X consistently.

My original gambit was 70% portfolio. I specifically did this so I had enough capital (30%) to play with other stocks as I never went into the finance media sector hanging it all on one trade. Some of the other stocks I concentrated into this year exploded, vastly outperforming Kraken. From buying $AAOI at $50 or $BE at $90 or $SOI at 50 euros, I made multi-bagger returns and in some cases used leverage and options to amplify them. Because of this and the fact my business has taken off recently (more cash to grow my total portfolio size) Kraken has naturally become a smaller share of my holdings though it is still a large concentrated position for me. I don't want to mislead people since my original video and X post were specifically calling out a 70% portfolio number. As a result I removed that % call out from my bio and unpinned the video to not mislead my followers who may blindly match my allocations (which tbh can change on any given day so it's not accurate to post anyway). To be honest, I'm still learning how to do this stock influencer thing, and while I talk a big game, I'm also just figuring shit out and how to best add value to this ecosystem of people from many walks of life, experience, and net worths. I care deeply about everyone who follows me and I have no interest in misleading people, pumping stocks etc.

I look forward to continuing to cover Kraken Robotics as a core equity position in my portfolio, as I do believe this company has an incredible multi-bagger future. My discord is still very active and a great place to connect with the fellow tribe to stay engaged.

Kraken is profitable, well run, fast growing, has a huge band of revenue projections from the greatest startup of this century (Anduril), and benefits from all the major geopolitical events happening in our world like countries disintermediating from U.S. defense or the idea China would deploy mines around Taiwan. Shoutout my friends @spacanpanman @SpacBobby who continue to cover the name with me and there's more too.

I am still in love with the stock and think it is highly undervalued here.

When it wakes back up, the Kraken will return with a vengeance. Just watch!

English

@Browpeak Joe is one of those guys who is inherently a BS artist. He truly talks the book as if the best scenario will always unfold (ie Nyserda rev this year; 100% of the realistic $350m backlog converting). Instead of over delivering.

English

@Browpeak This strikes me as both an exit and cover on their investment. They bring in new mgt to JV, fire Joe and Nathan and see how it works for a year. Not a great look IMO but perhaps only solve for this pathetic sales team and bad prod mkt fit (so far).

English

@FinanceHandsOn @bert_gilfoyle Maybe worst sales and marketing team I’ve seen. And that is all on Joe and Nathan. Both should be released ASAP. As you said, perhaps this JV enables that. Cerb covering their investment so much is a bad sign, ironically, in short term.

English

@bert_gilfoyle This is matching Fluence model…somewhat to manage orders. The JV gathers the orders and Nathan is eventually released cause he can’t close an order although fluence signed two hyper scaler agreements, I like the change as maybe Eose sales team is damaged goods

English

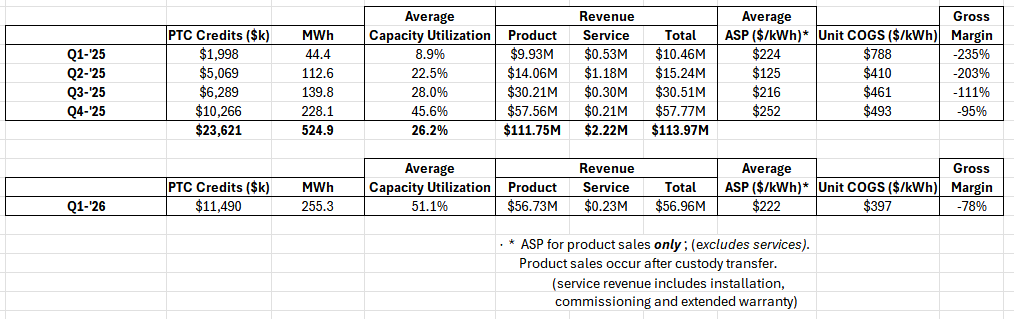

$EOSE

Best Unit COGS quarter so far. But still can do much better, even in Turtle Creek, if capacity utilization is increased. Existing run rate currently gated by customer delivery windows and process improvements that occurred in Q1.

However, the Frontier Power USA agreement appears to be designed to solve that very problem with a capacity planning mechanism to accelerate project timelines. "Same playbook GE used with GECAS and EFS. Proven model, new industry. Smooths out orders too." - @somerset877

No new significant orders were booked in Q1. But the Frontier Power 2 GWh is a firm order added to the backlog post Q1.

English

@jiahanjimliu @MarkosAAIG 30k shares of $inv for me that says “you’re right”!

English

Datacenters: Liquid Cooling

I read through @MarkosAAIG's market report on liquid cooling for datacenters. Among the pack, there are two leading companies that are ahead in two stage liquid cooling but one that Markos and I both see better risk-reward. I have started a position and am working on add to it. Markos' research paper is 42 pages and is his IP so I will not leak his work. I've done some more research and have some views of this market overall and will provide them to supplement Markos' market research paper.

Liquid Cooling Bottleneck

From tracking datacenter buildouts, one of the difficult parts is the liquid cooling. Designing the liquid cooling incorrectly can lead to 3-6 months delays in build times.

Chiller plants and high pressure pipes needed to have high flow rate are both high risks to uptime as they need remain operation for GPUs to remain operational.

Nvidia Vera Rubin Cooling Specs

Vera Rubin is on a higher power density rack and needs a higher rate of cooling. However, there is confusion as Nvidia recently spec Vera Rubin at the intake to need warm-water liquid cooling or 45C (1). I will explain how higher intake temperature increases the need for two stage liquid cooling. Nvidia specs 45C at intake to remove the need to have chiller plants and reduce the pressure on pipes because these do not scale well. As you scale single phase liquid cooling, the requirements on the chiller plant and pressure on pipes increases which is up-time risk!

Because 45C is a higher intake temperature, the delta between the intake and GPU surface is smaller. In order to have sufficient cooling rate on a smaller temperature delta, you need to have better coolant which relies on liquid-gas-liquid phase transition to dissipate the heat. Furthermore, water and water solutions are no long sufficient. Liquid cooling will need specialized chemistry in their coolants to produce higher liquid flow rates at the same CDU pressure.

Technology Constraint

In terms of technology complexity GPU > HBM > Cooling. However the market cap of Nvidia > SK/MU/Samsung > Two Phase Liquid cooling companies.

What I'm trying to say is that HBM is less complex than GPU but is sufficient complex enough that it has carved itself out a bottleneck position for AI compute.

Chemical engineering is not a fast moving field and the technological leads here suffice to potentially hold some bottleneck advantages.

HBM manufacturing is harder to scale and requires very experienced fab engineers operating every new site. I don't think two stage liquid cooling companies will reach the same magnitude of market cap but the the much lower starting market cap of a well chosen two stage liquid company make it interesting investment.

Markos@MarkosAAIG

Liquid cooling pick💧 full investment paper live✍️ (It is in my portfolio also) I already talked a while ago about liquid cooling and what’s happening in that sector. As you can see below, we think the importance and cruciality of this trend is still not recognized well enough by the market, especially when you look at the different cooling techniques now emerging. We are still at the very beginning of a major adoption curve for liquid cooling. As most people interested in the AI sector already know, upcoming AI infrastructure generations explicitly require liquid cooling to function efficiently. Cooling is increasingly becoming a crucial layer in the AI build-out from performance guarantees to reliability, insurance, uptime, and everything in between. We found and thoroughly investigated a very overlooked company in this space, and we just published a 40+ page deep dive on both the company and the broader industry. I personally own it also. Inside: • Bottom-up TAM build two-phase sub-segment alone: $25M → $9.1B by 2030 • The physics: why single-phase breaks and two-phase doesn’t • PUE/WUE economics: same grid connection, ~71% more deployable GPU capacity • The $24–25B data center insurance market by 2030 that quietly mandates two-phase for actuarial reasons • why this company has a unique positioning • full valuation and TAM capturing • aquisition comparison in a aquisition heavy sector And much more. Full Pdf available on our discord which you can acces trough SS. Link in bio👆 $IREN $NBIS $CRWV $VRT $NVDA $AMD

English

@asymmetricinfo You need ask others for help with logic, possibly use AI, as you are incapable on your own.

English

People who want to blow off Hantavirus because COVID turned out to be no big deal: COVID had a fatality rate of 1%, concentrated among the elderly. Hantavirus has an incubation period of up to 8 weeks and kills 30-40% of people who show symptoms. Whole different beast. It’s not pandemic yet and probably won’t be, but if it were, the rational action would be—lockdown

English

@PalanTesla A year.

I’m selling more leaps now. Puts and calls.

English

Hi everyone, my name is Bobby.

I walked away from a $300k executive sales role. I’m unemployed by choice.

I pay the bills by selling calls and puts against my portfolio.

I have real expenses — bills don’t stop just because I retired. So I have two choices: sell stock or sell premium. I choose premium.

Sure, I wish I didn’t have to pay bills or the IRS. I wish I had an infinite money printer so I could just keep buying more shares and never sell any. But that’s not reality.

I’ve decided to live off my portfolio.

Glad we could meet. This is my journey

English

@JTLonsdale @johnrea Get real. It won’t change. It only gets worse.

English

@johnrea It’s not time to give up on Austin. The state can crack down on it to fix it, and the electorate can wake up as they did on the homeless camping policy.

This is a boomtown seat of the capitol of Texas - it’s worth fighting for.

That said, we do live outside of downtown for now!

English

It's incredibly sad to see what the 'easy on crime' policies have done to Austin.

My wife and I have decided to move, and a huge part of that is that the people running this city care more about violent criminals than the safety of our children.

For shame to every one of you who voted for and supported these policies. Have fun with your cesspool once the rest of the productive economic base leaves too.

Joe Lonsdale@JTLonsdale

We could jail a small number of criminals in every blue city and massively reduce crime, making everyone safer. But the left thinks it’s racist to enforce the law. So we all suffer. If your windshield was smashed, or your family hurt by a repeat offender, how would you feel?

English

@johhnyWalkerAZ Congrats man! I own, but not like you! Very good day to you sir.

English

Girlfriend and I at coffee shop. We shed tears. 😭 $RKLB

English

The geometry of thought.

Every LLM on earth can speak fluent English. None of them think in English.

I have been trying to find a way to explain this to a non-technical friend for about a year, and I have mostly failed, because the standard explanation requires the listener to picture an abstract space they have never seen. The breakthrough I finally landed on came from an old map.

In 1569, a Flemish cartographer named Gerardus Mercator published the projection of the world that bears his name. The Mercator projection takes the surface of a sphere and prints it on a flat rectangle, in a way that preserves angles but distorts areas.

Greenland looks the size of Africa even though Africa is fourteen times larger. Antarctica becomes an enormous strip along the bottom of the map. The proportions of the world, in the Mercator projection, are confidently and consistently wrong.

We kept using it anyway, for four hundred years, because it has one priceless property. If you draw a straight line on a Mercator map, that line is a constant compass bearing. A captain in 1600 could plot a route from Lisbon to Recife with a ruler and a protractor and arrive somewhere close to where he intended.

The Mercator projection is wrong about what the world looks like. It is right about how to navigate the world.

We agreed, collectively, to lie about the shape of the planet in exchange for being able to find our way around it. This is what LLMs do with thought.

Inside any modern frontier model, concepts do not live as words. They live as positions in a very high-dimensional space, with a particular geometric structure.

Goodfire's recent work, which is the clearest public demonstration of this, shows the shape directly. Colors form a different shape, more like a sphere. Spatial concepts curl into manifolds that match physical space. The concept of a car is a complicated multidimensional surface that connects, in geometrically meaningful ways, to the concepts of motion, of metal, of road, of journey.

The model does not store these concepts as text. It stores them as geometry. When you type a question to it, the model maps your words onto positions in this internal space. It then performs operations on the geometry, which produce new positions. Then, only at the very end, it translates those new positions back into English on the way out to your screen.

The English is the Mercator projection. The geometry is the globe.

This sounds abstract until you realize what it implies for almost every interaction you have ever had with a model.

Why does GPT sometimes give a brilliant answer in one phrasing and a mediocre one in another, even though both phrasings mean the same thing to a human reader?

Because the two phrasings land on slightly different positions in the internal geometry, and the geometry near one position is richer than the geometry near the other.

Why does a model sometimes confabulate confidently? Because the position it lands on has the geometric texture of an answer even though the answer it generates has no factual grounding. The shape of an answer and the truth of an answer are different things, and the model is trained on the shape.

Three implications follow from this and they reach much further than most of the discourse about AI suggests.

1. for product builders. If you have ever wondered why the same model produces wildly different outputs on prompts that seem semantically identical, the answer is geometric. The most reliable way to improve model output is not to tinker with the words. It is to find the regions of geometric space where the model behaves well, and engineer your prompts to land you there. The best prompt engineers, without knowing it, are reverse-engineering the topology of the model's internal world. This is also why fine-tuning works better than prompting for many use cases. Fine-tuning literally reshapes the geometry. Prompting only steers within it.

2. for the safety and interpretability community, which has spent two years looking for circuits and individual neurons that correspond to specific concepts. That work has been valuable, but it was looking at the shadow on the wall. The actual structure is at the manifold level, not the neuron level. The next leap in interpretability is going to come from learning to edit the geometry directly, not by adjusting individual weights. We are about to move from steering the words to steering the shapes that produce the words. This will make some kinds of safety work much easier and other kinds much harder.

3: for everyone else, and it is the strangest one. The early evidence from neuroscience suggests that human thought may have the same kind of geometric structure. The hippocampus appears to encode spatial relationships on manifolds that look uncannily similar to what we see inside language models. Concept representation in the human cortex appears to be geometric in roughly the same sense. If this holds up, and the evidence is still preliminary, then the conventional framing of the difference between artificial and biological minds is wrong in an interesting way. It is not silicon versus carbon. It is two different physical substrates that have independently discovered the same mathematical language for representing the world.

We built something that thinks the way we think. We just never noticed, because we were too busy listening to it talk.

The Mercator projection is wrong about what the world looks like. It is right about how to move through it.

The model is wrong about what thought looks like, in some technical sense. It is right about how to do thought, which is the only thing that has ever mattered.

Goodfire@GoodfireAI

Neural networks might speak English, but they think in shapes. Understanding their rich *neural geometry* is key to understanding how they work – and to debugging and controlling them with precision. Starting today, we’re releasing a series of posts on this research agenda. 🧵

English

Finally undid the damage caused to the portfolio from the disaster that was Joe and $eose. 3 mos and A LOT of work/re-positioning. Thanks to $mu, $rklb, $iren, $inv $almu, for pitching in….

English

the fact that codex uses the language "fat fingered" to explain a mistake is both alarming and heartwarming:

"The asset copy missed because I fat-fingered the destination path. I’m rerunning that cleanly, then I’ll patch the code."

English

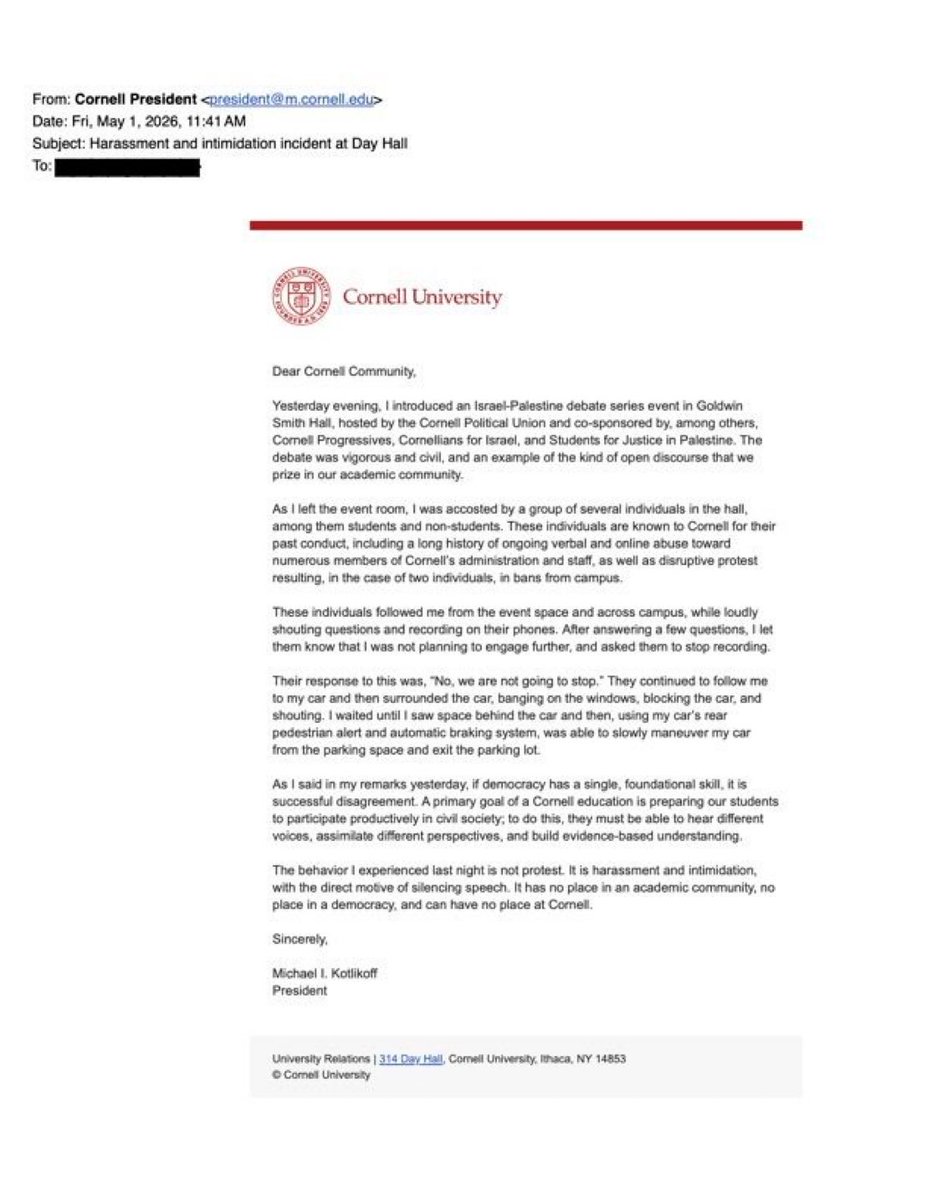

@EYakoby @Joshmedia You reap what you sow and they sowed this for years. Sucks for Michael. Perhaps he should have manned up earlier?

English

BREAKING: The Cornell President just obliterated the extremist students who surrounded his car.

Rather than surrendering to them and apologizing, he directly called out their unlawful behavior.

This is what true leadership looks like.

English