@giga_bull @RohOnChain Maybe blocked in your country idk. Try to open in the browser or in private browser

English

Domi | Algo Trader

4.1K posts

@AlgoTrader90

CEO @aurora_tech_io | Algorithmic Trader | NO FINANCIAL ADVICE!

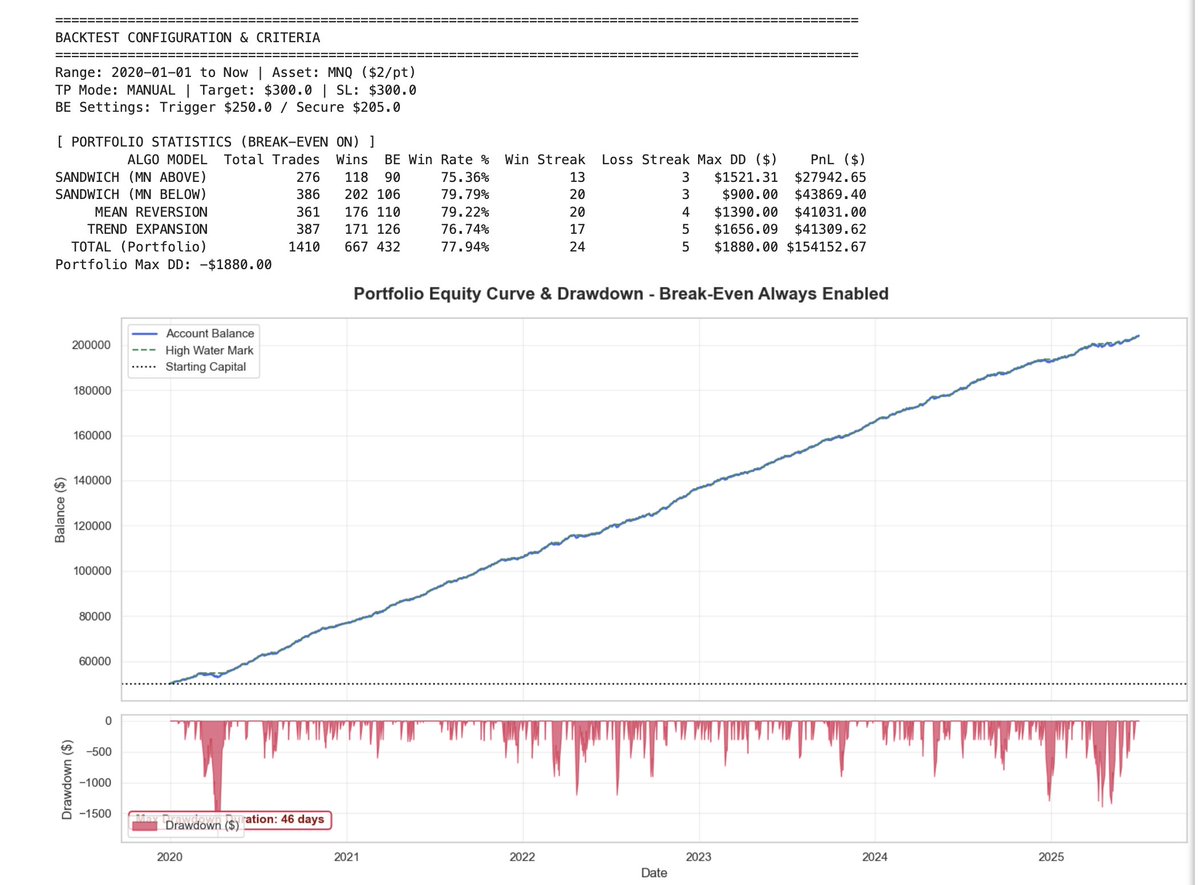

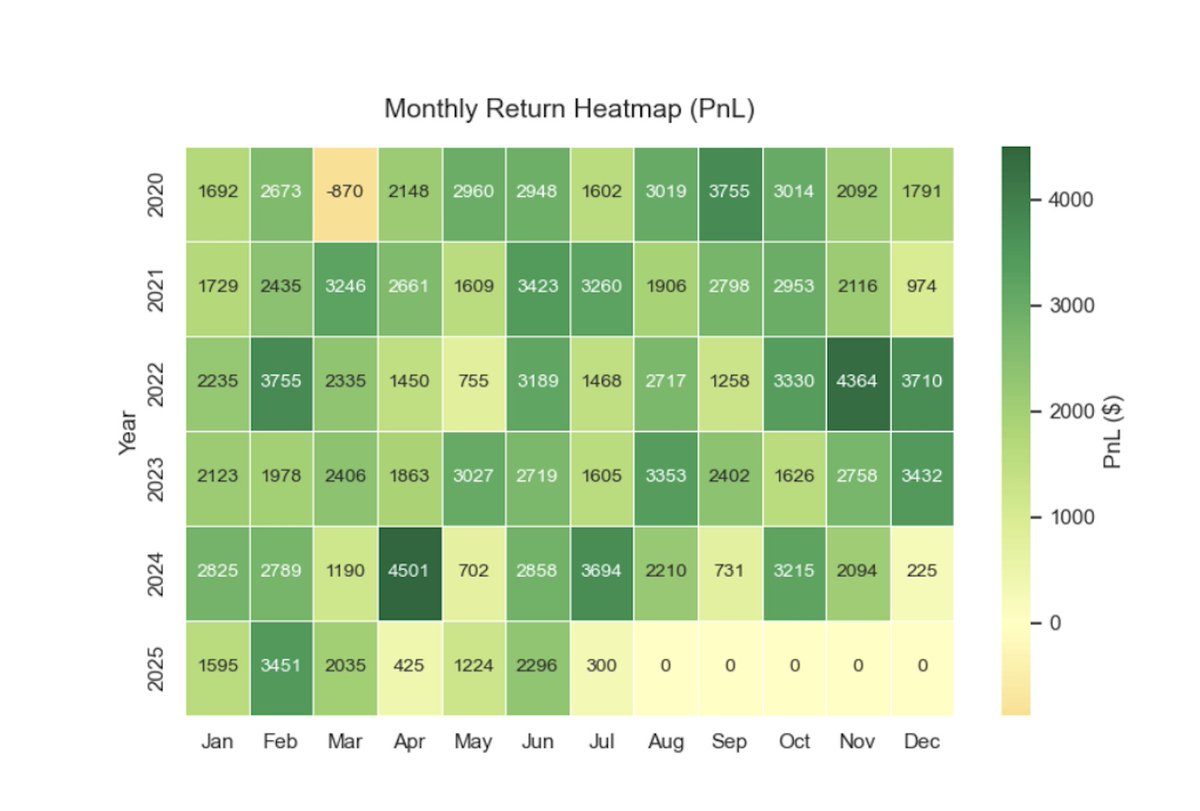

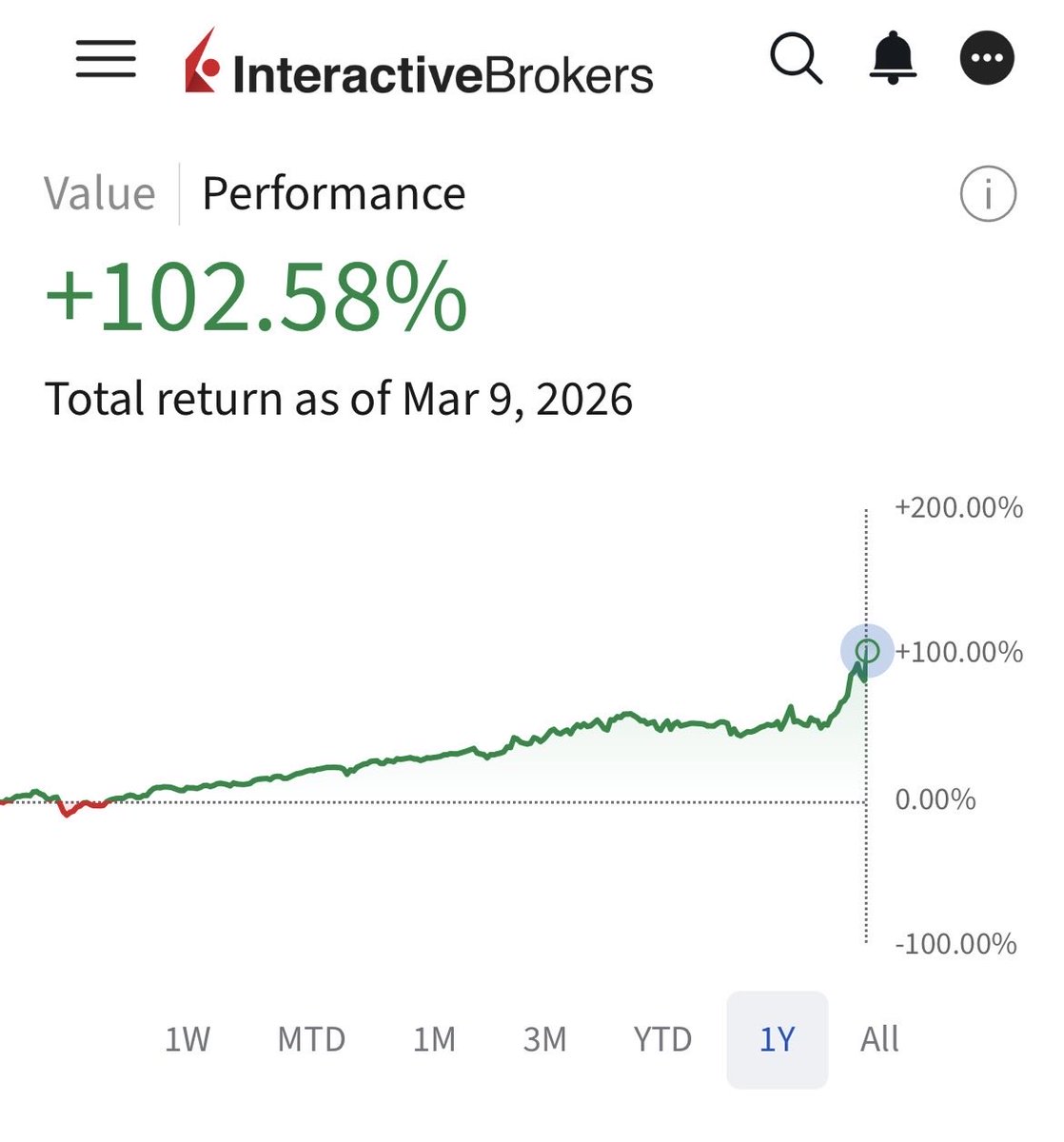

I got interested in algo trading recently. And I think I may have found a real edge. It’s 100% mechanical on $NQ Every day at exactly 2:00am New York time, the system gives a trade automatically. No prediction. No overthinking. No emotional bias. The indicator shows: long or short entry exactly at 2am. stop loss take profit break-even trigger It also has built-in alerts. The framework is simple: TP: 150 points SL: 150 points On 1 mini contract that means: +$300 win -$300 loss If the price reaches +$250, I will stop to BE in profit at +$205. That’s the whole model. What makes it interesting is this: In backtesting, it delivered 75%+ win rate and the historical drawdown never reached a level that would have blown a $50k prop firm account. So now I’m doing what most traders avoid: forward testing it on a live market with a dedicated eval account Because backtests are not enough. But when a model is: mechanical repeatable risk-defined time-based simple to execute …it deserves to be tested properly. Too many traders lose money not because their idea is bad… but because their execution is inconsistent. This experiment removes that excuse. Now the question is simple: Does the edge survive real conditions? That’s what I’m about to find out. Would you run a system like this live? #AlgoTrading #PropFirm

🚀 Auroraverse Beta Launch soon 🔎 What to expect • AI-driven stock discovery • Powerful filtering and screening capabilities • Fast insights across global markets • Built for all stock market enthusiasts 👉 Join the waitlist: aurora-tech.io/auroraverse

One of our most ambitious projects will enter the next stage. Our innovative stock screener „Auroraverse“ is soon in its beta phase. Over the next three months, we will stress-test the logic and optimize the user experience together with our beta community. Stay tuned!

Sigma Score is an MT5 indicator that standardizes the latest bar’s log return into a z-score, showing how many standard deviations it deviates from the recent mean. Values near zero reflect typical noise; readings beyond configurable bands (commonly ±2) flag statistically unusual moves, with the caveat that real returns have heavier tails than a normal model. The implementation focuses on practical MT5 engineering: one plot buffer, level lines at 0 and thresholds, and a rolling calculation in OnCalculate using prev_calculated for efficiency. It computes mean and variance inline (no extra arrays), skips invalid prices, uses EMPTY_VALUE for non-computable regions, and adds a small stdev guard to prevent divide-by-zero artifacts. Traders can use extremes as context for mean reversion or momentum decisions, and as a risk meter when volatility regimes shift. #MQL5 #MT5 #Indicator #Strategy mql5.com/en/articles/20…