@RWAFoundation_ @WALLY_DAO @solana @plumenetwork @ethereum @BNBCHAIN @RobinhoodCrypto Solana leading rwa onboarding 🎖️

English

Allez Labs

788 posts

@AllezLabs

Data and risk experts, in DeFi risk management since 2019 We’re hiring data engineers and analysts

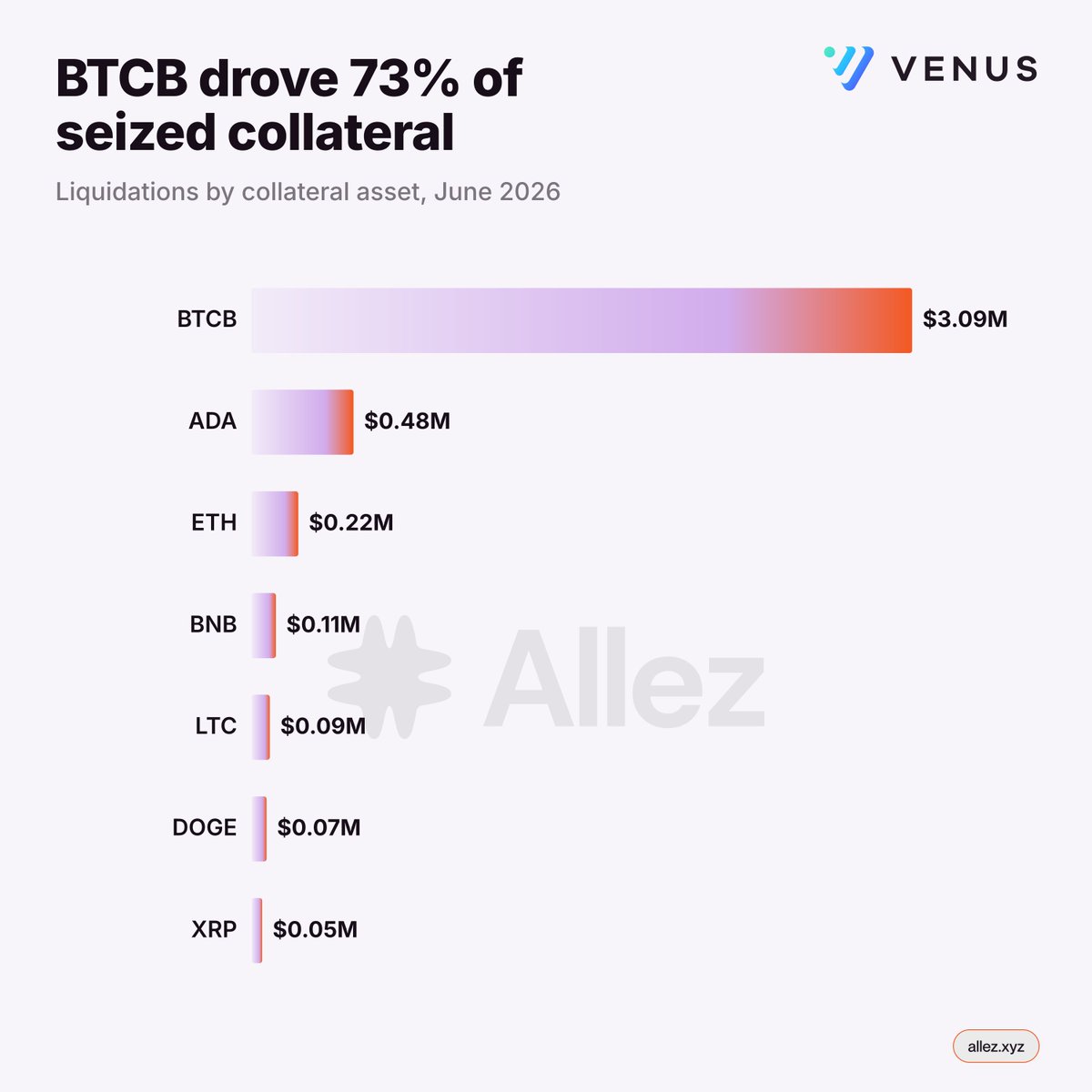

Monthly @VenusProtocol Insights - June 2026 As markets contracted to their lowest levels in years, Venus Core Pool absorbed the shock cleanly. BNB fell 23%, 1,697 liquidation events seized $4.24M, protecting protocol solvency along the drop. Continues 👇

Vault stayed PYUSD-heavy, reflecting the same rotation: → @SentoraHQ Ethena PYUSD Prime: $250.3M (new) → @SentoraHQ PYUSD: $142.3M (-26.7%) → @RockawayX RWA USDC: $26.0M (-40.3%) → @SteakhouseFi USDC: $22.5M (-26.5%) → @AllezLabs USDC: $16.0M (+23.0%) The new PYUSD Prime vault funds the Ethena Multiply strategy; the prior USDG Ethena Prime shrank to $7.5M.

Lending stablecoins here = the senior tranche: over-collateralised by ONyc, ahead of borrower equity. @onrefinance underwrites catastrophe reinsurance and holds low-risk assets like T-bills and yield bearing stables for its yield. Only ~half the book is currently deployed to reinsurance, which limits drawdown risk and leaves potential redemption capacity. A supplier loss needs both a ~30% ONyc NAV drop and a liquidation failure. @kamino has passed no bad debt to date, across ~$230M of liquidations cleared (280k+ events since 2023).

Steady lads, we are raising the cap limit! @solsticefi Yield Looping Vault has crossed $2M TVL and capacity just increased. Let's take a look at the strategy details 👇

Stablecoin yields in the OnRe Market are outperforming DeFi benchmarks and 3M U.S. Treasuries. Earn up to 8.21% on USDG and 6.91% on USDC (30D avg), with diversified, risk-adjusted yield sourced from reinsurance premiums, stablecoin markets, and T-bills. Risk-adjusted stablecoin yield, powered by Kamino.

A reasonable criticism of RWAs like OnRe is that the real stress sits upstream of the chain, so all you can lean on is monthly attestations. Worth adding some nuance to that. The transparency limit here is structural, not @onrefinance choosing to be opaque: reinsurance losses are off-chain events that only crystallize when a treaty settles. What matters is how an issuer mitigates that, and OnRe does it two ways: a liquidity buffer deliberately kept unallocated (they cap their own yield to hold it) and a well-diversified underwriting book, both public on their transparency dashboard (app.onre.finance/earn/transpare…). That is what lets you actually stress-test the asset, simulating potential NAV drawdowns from treaty concentration and cat exposure against the buffer. On the reserves: about half sit on-chain and are readable continuously (stablecoins + T-bill proxies), and the rest is the monthly cadence, BNY Mellon / Clarien custodian statements confirming the balances, plus an Apex attestation on the NAV. That stress-test lens is exactly what a venue like @kamino works through before listing it as collateral.