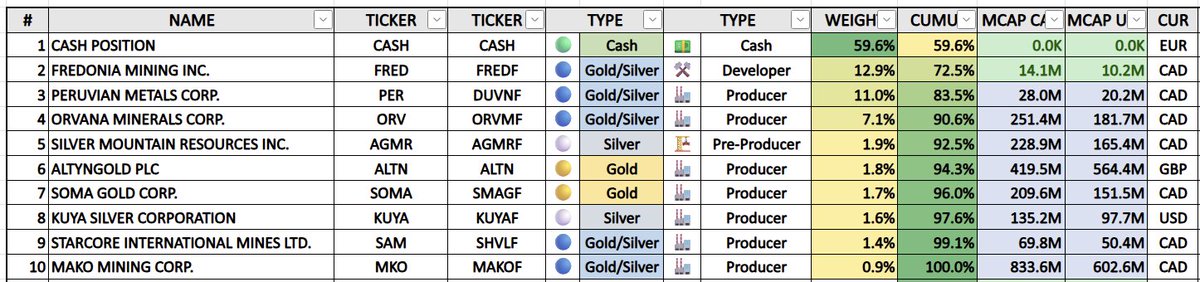

$ORV.TO $ORVMF - ORVANA MINERALS

US$235M market cap. Two producing mines. $54.4M in quarterly revenue — a new all-time record. $19.6M net income. $29.9M operating cash flow. Zero equity dilution.

Orvana just posted a record quarter and the market barely noticed. Gold-equivalent production is on track to triple from ~35k oz (FY2025) to ~106k oz (FY2027) — organically, with no dilutive raises — while consolidated AISC could collapse from $2,700/oz to deeply negative territory as Don Mario's copper and silver credits overwhelm operating costs. At $4,565 gold, illustrative FY2027 free cash flow of $130–165M implies the entire company trades at ~1.5× forward FCF.

The stock sits at C$2.22. The in-situ metal value of the Bolivian oxide stockpile alone is $1.33 billion — 5.7× the market cap.

In Argentina, 15 km from ATEX Resources' C$1.3B Valeriano porphyry, drill hole TADD-278 has logged A/B veins and molybdenite at 1,332m — textbook porphyry indicators — with critical assays still pending. A hit could be worth multiples of the entire company. A miss is already priced in.

Three assets. Three countries. One stock trading like a single-mine junior.

@abl_trader Antingen är bolaget helt fel prissatt eller så är det skyhöga risker. Kommer dom bara igång så borde inte silverpriset spela så stor roll, det kostar ju inget ta upp metallerna.

Absolicon Solar Collector

Ser att bolaget är ute och tigger om pengar nu igen.

Sedan tidigare 352Miljoner från aktieägare och 30 miljoner från skattebetalarna.

Hur mycket ska dom ha den här gången?

Tidvattnet påverkas inte av lokalt väder, vattenströmmarna är förutsägbara så Minestos elproduktion är planerbar och saknar behov av bränsle precis som en evighetsmaskin.

Minesto, en perpetuum mobile

Vattendrake 1.2MW

1,5miljarder (aktieägare 1 miljard och EU 500miljoner) och 20 år senare och med ett stigande oljepris.

Är det dags nu?

Edison Investment Research initiates coverage on $LEM with a risked valuation of US$0.9bn - approx ~17x our current market cap of US$53m. On an unrisked basis, @Edison_Inv_Res values the Norra Kärr project at US$1.8bn.

#NorraKärr is unlike any other Western #RareEarths project:

· 52% Heavy Rare Earth profile

· #Dysprosium & #terbium forecast to contribute to ~40% of revenue

And we are advancing - In March 2026, the Swedish Mining Inspectorate formally recommended approval of our exploitation concession. The application is now with the Swedish government for a final decision.

Updated pre-feasibility study on track - the next major de-risking milestone.

Read full report here: bit.ly/4sOEhvi#RareEarths#CriticalMinerals#HeavyRareEarths#LeadingEdgeMaterials#EuropeanMining#Sweden

@quantsisco@LeadingEdgeMtls@Edison_Inv_Res Finns väl kanske en risk för att omfattande investeringar och långa segdragna projekt blir nödvändigt för att övertyga alla parter att dricksvattenkvaliteten till en miljon svenskar inte äventyras på kuppen.

Men jag är ingen expert, och det verkar inte du heller vara.

@Andreas44444444@LeadingEdgeMtls@Edison_Inv_Res Vilken tur att Leading Edge planerar att minimera det kemiska fotavtrycket vid gruvan genom att exportera den miljöfarliga hydrometallurgin till en annan plats

@Silver__Santa Now it's debt-free, drilling in two places, and cash for almost two years and even cheaper than when you wrote about it. And I can not find any negative news