Sabitlenmiş Tweet

Angle 📐

3K posts

@AngleProtocol

The stablecoin protocol behind EURA and USDA. Now winding down. 👉🏼 The adventure continues at @merkl_xyz

There are two broad classes of tokenized stocks today: - Natively tokenized shares, where the token is a direct claim on the underlying security. @Securitize notably works this way. - Wrapper tokens, where the token represents a claim on an SPV that holds the shares. This is the @xStocksFi or @BackedFi model. I won't dwell on the legal implications of each model, rather, I want to focus on the part that's directly relevant to what we do at @merkl_xyz: dividends. In the wrapper model, there are two ways to reflect a dividend or a stock split onchain: - A rebase that changes token balances directly. This is how xStocks is usually described. - A multiplier that moves the exchange rate between the token and the underlying, leaving raw balances untouched. With dividends only, the multiplier starts at 1 and grows over time. This is effectively what the SPV provider is already doing internally. Rebasing is the more problematic option for dividends because it breaks DeFi composability. A balance that shifts under a protocol's feet corrupts AMM pools and lending positions that assume it is stable. The multiplier approach only updates a single value, and thanks to ERC-8056, oracle providers can consume that multiplier natively, so composability holds. But the multiplier has a cost: it forces reinvestment. The dividend compounds into the token's value rather than being paid out, which means the issuer is buying more of the underlying instead of distributing cash. That leaves the native model, where the token is a direct claim. The obvious question is: if the token is spread across layers of composability, how do you distribute a cash dividend? This is what Merkl solves. We can identify the beneficial holder of a token wherever it sits. Picture a vault of tokenized stocks used as collateral on Morpho: Merkl traces the end user across every layer of composability and across chains, so holders receive the cash payments they are owed for holding the token. Forwarding is fully customizable, so a protocol that wants to keep its share of the dividend can do that. TL;DR: the multiplier mechanism preserves composability, but at the cost of forcing reinvestment instead of a real distribution. Picking an SPV wrapper only because splits and dividends look hard to handle is the wrong reason to pick it. Distributing dividends precisely and in auditable manner across DeFi is exactly what Merkl unlocks.

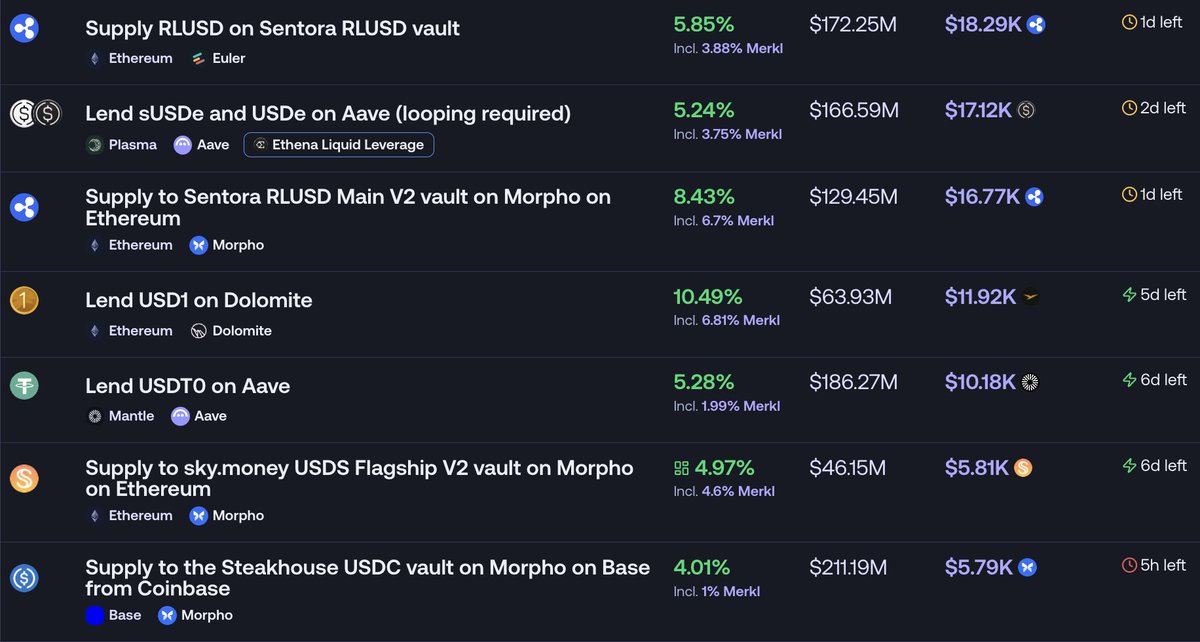

Don't know where to start with incentives? Our new Guides section is for you. Setup walkthroughs, optimization tips, and best practices on budget sizing, LP retention, and more. Built from 60,000 campaigns across 250 teams. studio.merkl.xyz/guides ⤵︎

The CLARITY Act's threat to yield distribution caused Circle's stock to drop 20% in a single session. That's a policy event with capital market consequences. @GuillaumeNervo of @merkl_xyz tracked it in Cannes. Don’t miss his solo talk on institutional stablecoins ↓ youtube.com/watch?v=QRSDfm…

⤵️ $CRCL drops 20.98% on developments surrounding the Clarity Act, a bill that may restrict yield offerings on stablecoins.