@saketh1998 Yes everyone is building it these days.

You can check mine at vantagecapital.co.in

English

Atul

2K posts

@Atul4ward

CFA | FRM | IIMB | 10+ yr experience in Investments

Completely deployed, No cash left 🙏 Okay to see pain in the near term. Personal finance is personal. Happy to live with some drawdown without worrying too much given horizon is Multi year in nature 🙏

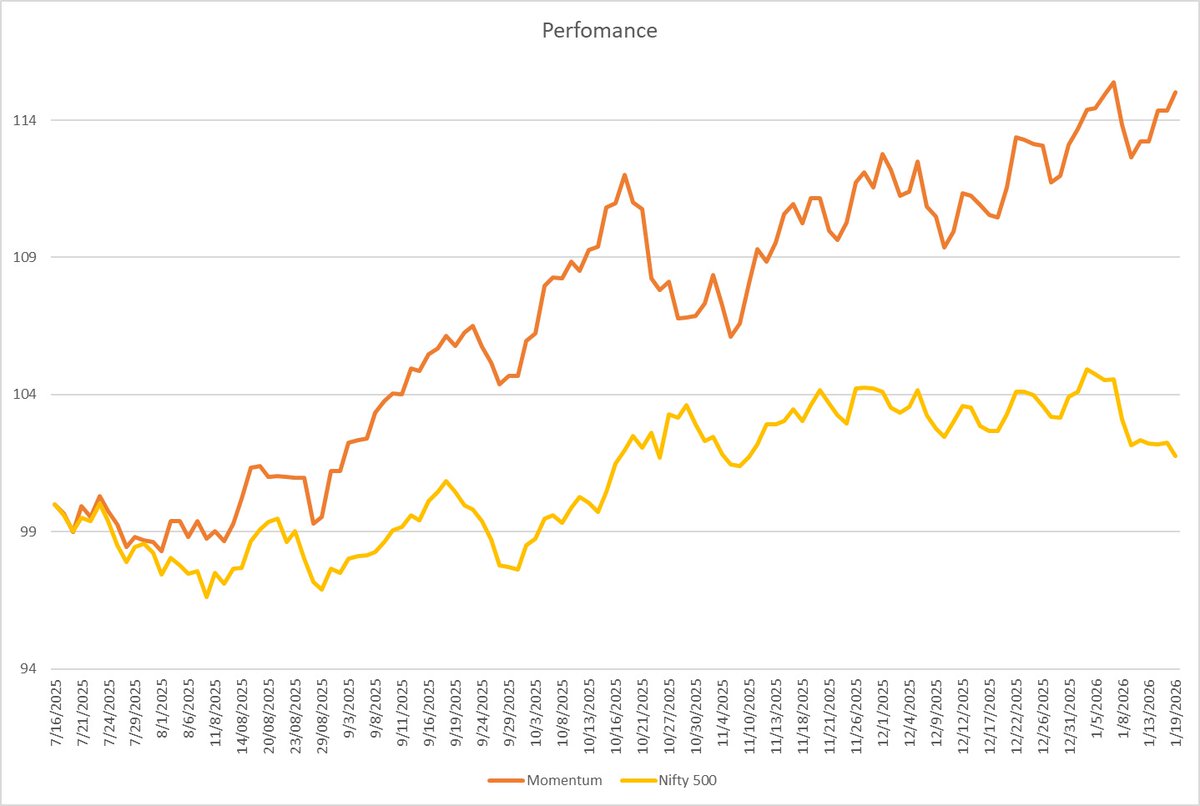

It’s been about 3 months since we started running the full momentum portfolio and it’s still going strong! 3 months is still a short window, but so far, the performance looks decent

10-minute delivery in India isn't magic. It's really good engineering. @albinder and @letsblinkit built tech that most people never see. We went deep on how it works.

JPMorgan: Anthropic is eating the world Jabroni: Buy $ZM