Sabitlenmiş Tweet

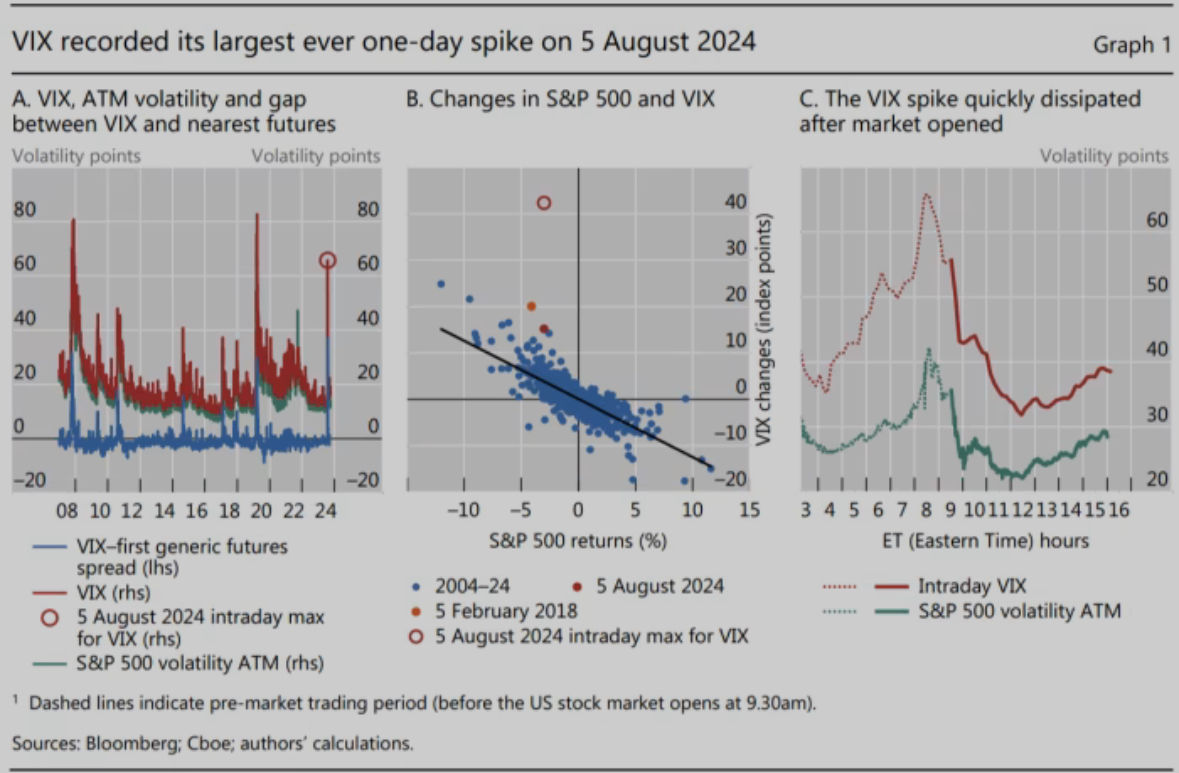

“On Friday August 2nd, 2024 the Market was hugely mispricing risk, we tweeted live that we were going Massively long volatility (x.com/bankofvol/stat…) as our analysis revealed risk was underpriced by market makers and professional investors.

The following Monday was the biggest one day jump in the spot VIX in market history (+181% from Friday close to Monday high). We made +35% on our massive VIX futures long position and several million dollars of PnL in a single day (x.com/bankofvol/stat…) . In our Substack we dive deep into volatility term structures and dynamic to uncover these rare opportunities just before volatility spikes.

If you are serious about protecting your capital, these are signals you can’t afford to miss.” "2ly.link/2CYQg""

#VolatilityTrading #RiskManagement #LongVol #VIX #OptionsTrading #Hedging #MacroRisk #TailRisk #VolatilityStrategy #MarketVolatility #TradingStrategy #QuantTrading #FuturesTrading #MarketCrash #FinancialMarkets #InstitutionalInvesting #AlphaSignals

BankofVol Grift¹⁰⁰⁰🤖🤖¹⁰⁰⁰⁰⁰⁰@BankofVol

Hedge off. VX_F long massive.

English