Phathom@PhathomResearch

Here are my initial thoughts on the $PATH Q4 '26 earnings report.

PATH's Operating Margin Expansion is Extremely Impressive

- Achieved 23% operating margins in FY26, up from 17% in prior year. They raised their long-term target to 30% operating margins. This means that the internal machine is working.

- The most exciting part is that they attributed the internal use of their own agentic platform (a.k.a. Maestro) across the company as a main reason for the operating leverage.

- This is a huge Maestro proof-of-concept playing out right in front of us as we see PATH expanding their margins using their own product.

Agentic AI Flywheel is Primed and Ready

- As of 1/31/26, 90% of customers with >$1M ARR are using UiPath's AI products.

- As of 1/31/26, 42% of customers with >$100K ARR are using UiPath's AI products.

- While these numbers are encouraging, we have to take them with a grain of salt as it's unclear how they are defining use of an AI product

- The fact that Q4 Net Revenue Retention was flat at 107% shows that much of this AI adoption is early-stage and has not yet resulted in significant revenue growth

- The flywheel is now primed to continue upselling those customers into more agentic automations

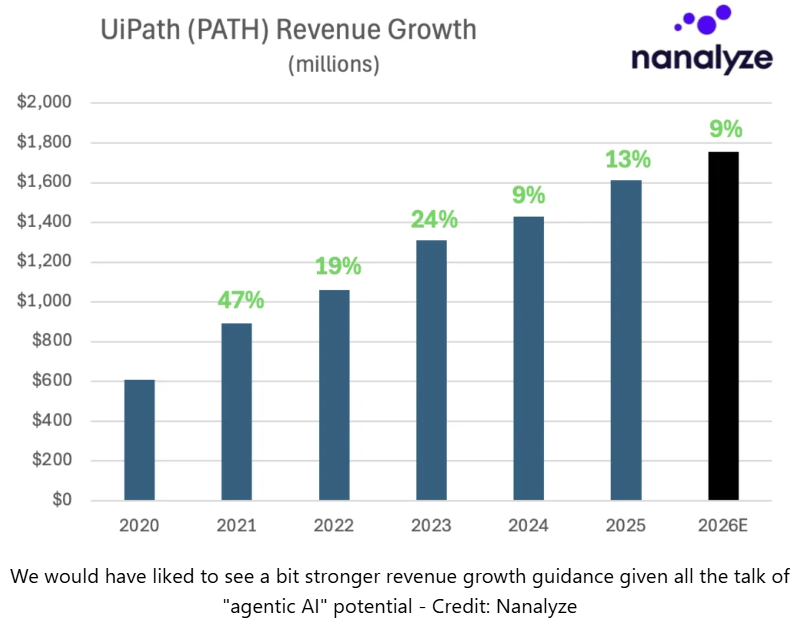

FY27 Guidance is Clearly Conservative

PATH just guided for a FY27 revenue growth rate of 9%. On the surface this looks underwhelming reflecting a deceleration from 13% in FY26; however, if you take into account the history of conservatism, the story looks much different.

First off, Ashim Gupta, UiPath's CFO/COO, stated the following two quotes during the call:

"We base our guidance on what we see in the pipeline, and we apply prudent assumptions."

"With AI and agentic, we do feel bullishness, but given the macroeconomic environment continuing to be variable, we do layer the appropriate prudence in."

In addition to management flat out telling us it's "prudent", anyone that has been following the stock for a while knows that sandbagging guidance is management's M.O.

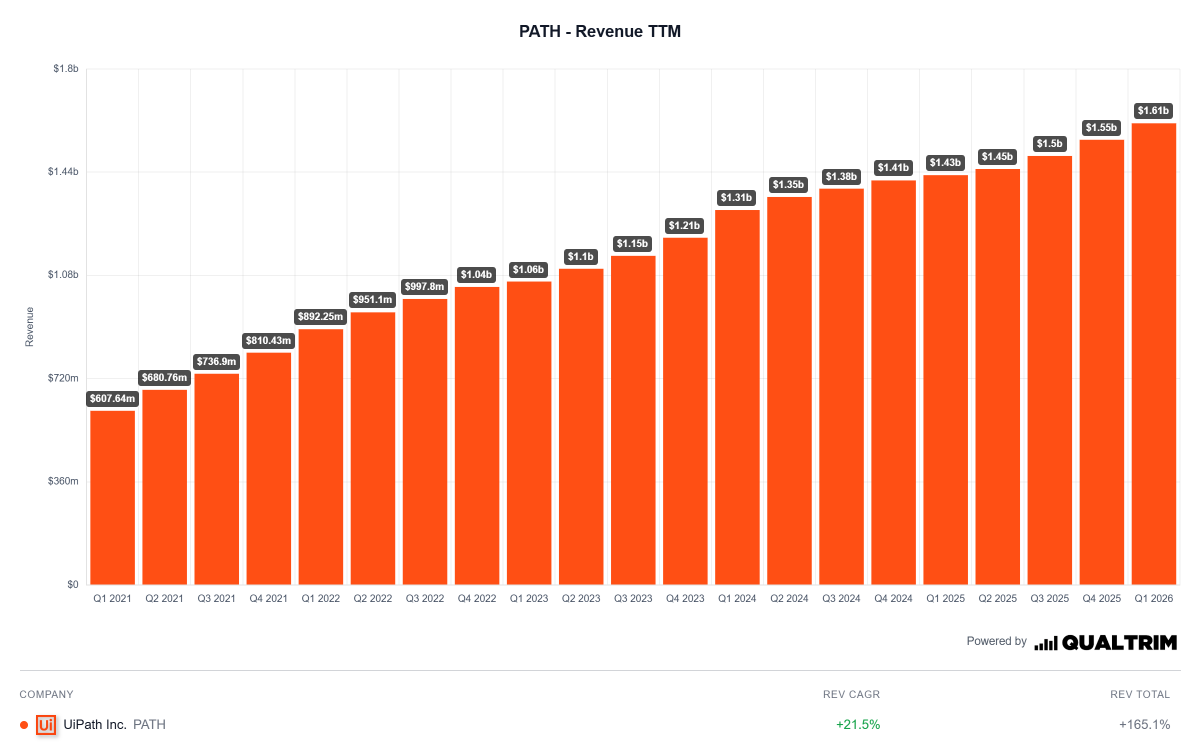

Look back a year ago at what they initially guided for FY26: 7% revenue growth. Well guess what? They crushed that guidance. The actual revenue growth was almost double at 13%, beating FY revenue projections by $84M.

If we assume they beat FY27 guidance by the same margin of $84M, that would put a more "realistic" guidance at $1.843B or up 14% Y-Y. This tells a much different story as it shows continued revenue growth acceleration in FY27.

What We Need to See This Year

- Net Revenue Retention rate needs to start accelerating showing that the agentic upsells are gaining momentum.

- Customer counts with >$100K in ARR and with >$1M in ARR needs to continue to grow highlighting focus on higher-ticket customers.

- On top of aggressively upselling, they need to be aggressive in winning new logos and keeping the pipeline full.

AI Coding Agents Will Be a Gamechanger

- In his prepared remarks, CEO, Daniel Dines said that UiPath coding agents will be launched within the next two months.

- He made it very clear that these coding agents are going to be aggressively used to quickly build and deploy customized UiPath agents.

- I expect this to speed up the rate of agentic adoption in the second half of the year.

- As barriers to building agents within UiPath drops, the number of agents will increase thus driving demand for orchestration

Final Thoughts

- PATH delivered a solid FY26 with revenue up 13% Y-Y and reaching GAAP profitability for the first time in company history.

- Operating leverage is being rapidly built within PATH by using Maestro internally - this is great validation of Maestro's ability to create efficiencies and deliver ROI when used at scale across a business.

- Customers remain very loyal to $PATH's products as evident by 97% gross retention rate.

- The FY27 revenue growth guidance of 9% is clearly sandbagged. I believe a more realistic projection is 14%.

- I have yet to see a competitor gaining share in agentic orchestration faster than PATH. $PLTR recently announced entrance into the orchestration market, so it will be important to monitor how quickly they gain share relative to PATH.

- I expect the PATH's launch of internal coding agents to be a massive catalyst in speeding up Maestro adoption

- With 90% of >$1M ARR customers beginning to use PATH's AI products, there is a large flywheel of sticky existing customers that are beginning to be upsold. Once the floodgates open, PATH's revenue growth rate will rise quickly.

- In the meantime, PATH is continuing large share buybacks showing management's conviction that the stock is undervalued and mitigating dilution risk for shareholders.

- They continue to generate FCF and ended the year with $1.7B of cash putting them in an extremely strong financial position to make more bolt-on acquisitions in FY27.

- I continue to the view the stock as a very exciting asymmetric setup with upside potential far outweighing downside risk.