Bizzarrini Lucas https://registerbizzarrini.com/

1.1K posts

Bizzarrini Lucas https://registerbizzarrini.com/

@BizzarriniL

Register Bizzarrini and Iso cars

Katılım Haziran 2022

122 Takip Edilen52 Takipçiler

@FeroceResearch I did try to talk to you...no answer ...then ?

English

Please do not be shy to ask me anything

This may seem like an exaggeration, but I truly enjoy taking the time to get to know everyone individually. Hundreds, thousands, doesnt matter

I respect the time you take out from your day to talk to me, and so I want to always show that respect back

English

🚨TONIGHT AT 12AM ET IS THE ABSOLUTE LAST DEADLINE FOR THE ONGOING PROMO

Please DM me for any questions. I will be answering them all day long

Feroce Research@FeroceResearch

LIMITED TIME OFFER** 👉 Use code: “FEROCE70” on the 1-month plan for 70% OFF during your first 2 months. Completely risk-free, 2 entire months for only $25.50 before full price commitment whop.com/feroce-researc… *click on ‘promo code & details’ to apply code if using mobile

English

@GenFlynn @EricLDaugh Listen to the General...When he talk, it means that he already known the answer. Dont fight against him, he is a winner ... Tic Toc...its coming

English

@EricLDaugh 2020 was a rigged stolen election. Biden was a false president whose autopen did more work than he did because he wasn’t awake most of the time. Maybe he was fake too. Where is he now?

English

🚨 HOLY CRAP! Venezuelan whistleblowers have come forward providing evidence that 2020 election votes were RIGGED

TRUMP: “The 2020 election was rigged.”

Even Susie Wiles confirmed he won some states that he “lost”

And the FBI now has Fulton ballots 🔥

English

I’ll later today release the list of every single major quantitative positioning you need to know for Micron $MU

As well as every single significant order (short-term AND past summer) that I have been tracking before this rally even started

You should be able to then know exactly what market is expecting, as well as at what levels can you expect faster price action or some hiccups

I hope you will all enjoy it

English

@runews I did follow you for many months but you are a idiot and a morron, always critic T or his wife. Show respect if you want respect . GO TO HELL

English

How come that, after 30 years of living in the United States,

Melania still can’t speak English well?

English

@HolySmokas Just look RSI to understand that before going higgher, we will go lower ... This guy refuse to buy MICRON at 320 and now he want you to buy here AMD ? Buy when its down

English

You will never get a chance like this ‼️

"The NEXT big one is HERE"

Congratulations to $AMD shareholders! let's celebrate together today

English

QME

There is a not so small chance that MU becomes a $1,000 stock while still trading at a forward P/E of about 5.

English

QME

500 likes by midnight tonight I will share every single monster $MU Micron market positioning I have been tracking, as well more that came in today

now that you know and have proof I don't exaggerate my posts

Feroce Research@FeroceResearch

im seeing more orders on $MU Micron today that the human mind could never comprehend the type of orders that makes you believe in the unbelievable the type of orders that makes you understand why insider trading truly exists

English

@FeroceResearch RSI can go a lot higher ..not the top

English

Do you believe me now?

The move happening on $MU Micron right now is not unexpected at all

Feroce Research@FeroceResearch

im seeing more orders on $MU Micron today that the human mind could never comprehend the type of orders that makes you believe in the unbelievable the type of orders that makes you understand why insider trading truly exists

English

@HolySmokas MU PE = 5 , PLTR PE = 100 !!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

Indonesia

$PLTR is a 1 of 1 freakishly amazing stock. Unreal earnings yet again

English

@HolySmokas You cannot follow 20 stock or 30...Its dump to think that people are Superheros. Its dump to have bought paypal as X is going to replace paypal . Stan Druckenmiller never loose money for 30 years. You are more clever than him ?

English

Tonight I will release 4 Stocks to Buy Now May 2026 edition!!! What 4 stocks should I feature in your opinion?

English

@HolySmokas You dont listen..then why wasting time with you ? Never heard of Stan Druckenmiller ? Want to talk about it ? Whatsapp + 32 474 681 781, be clever call me

English

@realalexvieira Please explain ? not clear at all

English

Futures explode higher. AMD insiders share earnings with Trump. AVIS insiders used a different tactic hiring a crooked hedge fund $SPY $AMD USA is a fraud x.com/i/status/20470…

Alex Vieira@realalexvieira

Intuitive Code warned me to sell AVIS $CAR and I warned you 👇 on X in real-time; now even the Pope is short the Trump scam from today's top $847 😂 $SPY $QQQ $MU $SNDK $ARM x.com/realalexvieira…

English

@FeroceResearch You are good, thank you, send a me a PM , lets talk , will explain what I do

English

i work completely independently,

and much of that is because anytime i have reached out for any sort of collaboration in the past, i've been ignored since higher performance does not equal to engagement

since then I made it a mission of mine to go against the status-quo and grow my reach on my own terms

I want to prove to others that you can grow a platform the right way, and by putting others first.

The increase of your portfolio matters far more than the increase of my following count

so i just want to say thanks to those who seriously take the time to dig into my work

English

@dejanirasilveir Who is arrested ?

English

@GenFlynn @Blue_Eyes Go for it General...please ..You are a hero

English

Remember when James Comey admitted to setting Flynn up?

English

@Sean14978416 A idiot, but WHY ? For him the management of MU are idiots, as they built news factories as they see huge demand in the futur, but this small analyst known more than them ? Really ?

English

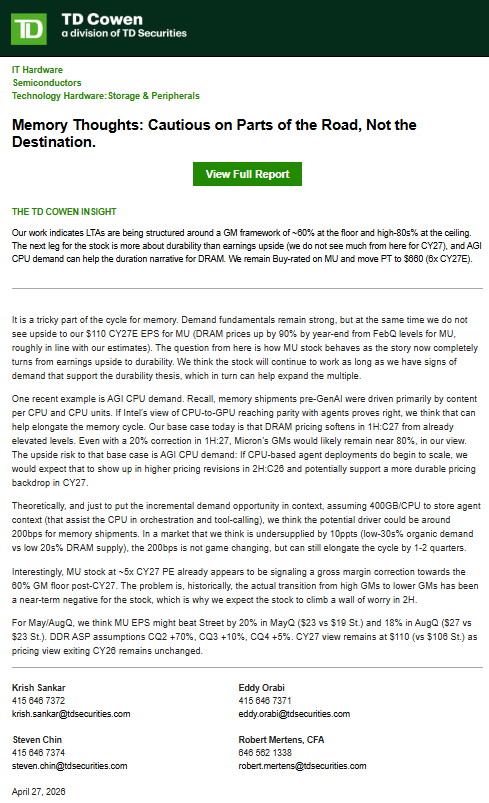

Cowen on $MU: do not see upside to $110 CY27E EPS

LTAs are being structured around a GM framework of ~60% at the floor & high-80s% at the ceiling.

~5x CY27 P/E signaling a gross margin correction toward 60% GM floor post-CY27. Historically high GM to lower GM been a nearterm neg

English

@MikeLongTerm Manipulate ? Dump idiot.. The guy follow MU for 20 years, he have the right to express his opinion

English

$AMD is a $1,000 stock & Gus is WRONG 🧵

This was a cheap downgrade with blurry comment to manipulate the stock price near-term

Not Financial Advice! Just well-researched thread!

For CY2027 (calendar 2027): He explicitly states that current Street consensus is "likely too high" (or "too optimistic"). He expects AI infrastructure spending to decline in 2027 due to hyperscaler capex discipline, cash flow constraints, data center build delays, and a shift toward usage-based pricing by companies like OpenAI/Anthropic.

This is current Street Consensus for AMD:

FY2026: $40-$46B with some higher in the $50B+

EPS (non-GAAP): ~$6.75 (range ~$5.8–$8.6)

FY2027: $55-$68B

EPS (non-GAAP): ~$7–$11+ (range ~$7–$18).

1. FY2026 basically deleted @OpenAI $META 2GW revenue. They also did not include $ORCL $MSFT $AMZN $GOOGL LumaAI, Humain, G42 and many others.

What do we know? 1GW is roughly $20-$25B. Where $NVDA 1GW is $30-35B (Helios vs Rubin)

The current street consensus is already much higher before, they were projecting 2026 to have ~15% before OpenAI and Meta.

What will FY2026 look like?

The lowest end of FY2026 projection:

AI GPUs: $40-50B (I'm very conservative already) EPYC Data center: $15-$20B(EPYC may contribute as large of revenue in 2027 due to explosive agentic AI demand)

Client Segment: $12-$13B

Gaming: $6B

Embedded: $4-$5B

Total Revenue: $77-$94B

Non-GAAP net income $19.3B-$23.5B

Non-GAAP EPS $12-$14.7

Subscribers already know $TSM is ramping up 2nm capacity and CoWoS aggressively. Will link below. so AMD will actually get the supply for 2027-2028 too.

2. FY2027: $55-$68B

EPS (non-GAAP): ~$7–$11+ (range ~$7–$18).

Basically Gus also deleted 2GW of Helios in H1 2027 and the new Upgraded MI500 & EPYC Verano. Or roughly 3-4GW for entire 2027. Newer rack is likely priced higher than Helios.

EPYC demand is so high right now that Customers are booking 2023 EPYC Gen and 2024-2025 Turin. Basically whatever CPUs AMD has, customers will buy it. The CPU:GPU Ratio already shifted from 1:4-8 to 3-5:1. Demand for EPYC Venice is projected to be 15-20m units and we have annual cadence now.

Gus basically deleted most of Rack Scale shipment, and refused to accept this massive Agentic AI demand where all Hyperscalers, Morgan Stanley, Intel, Arm, and various other equity firms already confirmed this trend. Or $MSFT CEO @satyanadella said “Every agent will need its own computer” complete with dedicated enterprise-grade sandboxes, durable state, identity, and governance in Microsoft’s new Foundry hosted agents. This implies massive scaling of per-agent compute instances, far beyond batch inference.

Gus is even more bearish than the false FY2027 street consensus without actually providing his Revenue and EPS forecast. This was clearly a cheap and manipulated downgrade. Like he projected 2024 AI Data center only $2B revenue and $AMD ended 2024 with $12.6B. When this idiot missed Revenue by $10.6B in 2024, that should be plenty of evidence.

3. What does $260 Price Target actually mean in FY2027?

$260= $420B market cap (FY2027)

This would mean:

P/S: 4-5x(implying massive collapse in AI CapEx)

AI Bears been through this since 2024. They been calling for AI CapEx collapse for about 2 years now. I rather believe in $TSM $AMD $NVDA $AVGO on this Super Cycle of 10years+ that we are only 2 years+ in instead of this moron.

P/E: 16-18x.

He is implying AMD would have a compressed P/E multiple, collapsing margin, collapsing growth, collapsing everything.

Ok we need to look at current P/E

$AMD TTM at $315 is roughly 118x

Fwd P/E: 21-26x

The average 9-year P/E is 136x

PEG Ratio is: 0.23. In what world this is expensive?

Clearly market participants do not agree with Gus P/E even with past, present or future P/E.

Clearly Gus is living in delusional land.

Dr. Su has a proven track record of more than a decade.

~EPYC is the best CPUs in the world, Turin beat all CPUs and Venice is going to be the next level

~MI455x outperforms $NVDA Rubin on Memory Bandwidth, TCO, TDP, and $ per million tokens.

~ $AMD makes better custom chips than $ARM and others, proven by $MSFT HBv series and many others. Dr. Su said custom chip is a massive opportunity to AMD long term

~AMD has the best NPU in the PC/Laptop segment

~Best performing gaming CPUs and top selling for years

~ Xilinx dominates in space-grade Chips with massive Space potential, will link the thread below.

AMD is the only company with a comprehensive, end-to-end portfolio of high-performance computing components CPUs, GPUs, and adaptive computing solutions designed for AI applications from cloud to edge. This "full stack" approach allows AMD to offer customers a complete, interoperable system rather than just individual components.

This is why AMD is trading at

TTM 118x P/E or

9-year P/E is 136x

Because Next year or Fwd P/E keep collapsing, and the potential is massive for multi-year with contracts and visibility.

Conclusion: Now you know why I been calling $AMD analysts sexiest, because they been wrong for years, and yet they insisted they will get it right with ridiculous price target and forecasts that are clearly delusional.

Under Dr. Lisa Su’s leadership, AMD’s 9-year average P/E of 136x isn’t a fluke, it’s the market’s long-standing recognition of massive, durable growth potential that Gus Richard’s note completely misses. While the Street’s FY2027 revenue consensus already sits at a conservative $55–68 billion , Gus has taken an even more bearish stance, slashing numbers further and baking in only modest growth beyond 2026. His $260 price target implies a paltry 16-18x forward multiple , the kind of valuation you slap on a mature, low-growth semiconductor name, not a fabless AI and data-center leader executing at the highest level.

That disconnect is exactly why the premium multiple has stuck for nearly a decade. Dr. Su has transformed AMD from a laggard into a high-margin, chiplet-powered powerhouse with expanding TSMC allocations, gross margins climbing toward 60%+, and superior TCO in inference that hyperscalers (Microsoft, Meta, Oracle, and others) are aggressively scaling. The OpenAI 6 GW deployment Dr. Lisa Su just highlighted on Fox Business is the latest proof point real demand, real scalability, and real margin dollars that Gus’s note simply undervalues.

Not Financial Advice!

Mike@MikeLongTerm

$AMD| Addressing Downgrade- Is "clueless" & wrong This downgrade is false and misleading, here is why I understand why he is bullish on $INTC, but there is no need to spread misinformation. 1. Intel "catching up" to TSMC is overblown / packaging overflow insignificant Intel claimed 18A node reached high-volume manufacturing (HVM) in 2025, with Panther Lake CPUs shipping and PowerVia backside power delivery providing real efficiency/clock advantages on paper. Yields have improved but still much lower than $TSM. However, TSMC maintains clear leadership in scale, yields at launch (75-80%+ for N2), ecosystem maturity, and external customer reliability. TSMC's N2 capacity is sold out through 2028 with aggressive expansions (3nm to ~180k wafers/month by end-2026; 2nm ramping to 120k+). Intel Foundry remains small, loss-making ($2.5B+ quarterly drag historically), and mostly internal. For AMD specifically, if any packaging (CoWoS overflow) to Intel is niche/insignificant TSMC dominates advanced packaging (CoWoS doubling+ to ~130k wafers/month by end-2026). 2. CY27 (FY2027) consensus is way too low! Not high with hyperscalers + CPU demand undercounted I been saying this since 2024/2025, and analysts are moving forecasts slowly to my projection. Subscribers and Followers already know. Dr. Su has guided data center >60% annual growth for 3-5 years, with AI scaling to "tens of billions" by 2027, and this was before $META and many other deals. Adding only OpenAI/Meta ignores Microsoft, Amazon, Oracle, Google, Meta expansions, plus J-Curve MASSIVE EPYC CPU demand (already ~30%+ share and climbing). Recent raises ( DA Davidson +$2B on 2026 rev) reflect this. Northland's "reset too high" assumes hyperscaler discipline bites hard but 2026 CapEx signals acceleration, this slowdown CapiEx been discussed since 2024 btw and all bears were wrong. FY2026 should have digits growth due to 2025 easy comp 3. AMD earnings far more robust than Intel's (fabless advantage shines) AMD non-GAAP gross margins hold 55-57%, likely expanding to 60-65% , vs. Intel's Q1 2026 non-GAAP GM at 41.0% (up but still dragged by foundry) and GAAP operating margin deeply negative (-23.1%) from restructuring/foundry costs. Intel's non-GAAP op margin hit 12.3% (better than prior), but it's nowhere near AMD's leverage. AMD went fabless to dodge this capital intensity. Intel's recovery is real (Data Center +22% YoY), but AMD's model scales cleaner on volume, this is why Street operating leverage forecasts favor AMD heavily. 4. Higher R&D → superior chips; Jensen copying chiplets; AMD longevity, efficiency, lower TCO AMD's playbook is paying off. Aggressive R&D (as % of revenue) funded CDNA4 chiplet designs: MI350X/MI355X deliver 288GB+ HBM3E/HBM4 (vs. Blackwell ~192GB), competitive FP8/FP4, and air-cooled 750W options. Independent TCO studies show AMD 25-40% better tokens/$$ or 3-year cluster costs in inference (memory density + power efficiency). NVIDIA is shifting to chiplets (Rubin) is a direct validation. AMD GPUs often win on longevity/TCO in targeted deployments. NVIDIA still leads ecosystem/share (~80-85% AI accelerators; AMD 5-10% butdominating in inference, especially Agentic AI where Turin is a clear winner), with better MFU via CUDA. But hardware gap narrows, and AMD's price/performance edge is real. 5. AMD pricing power rising sharply (Intel hikes reversing Milan-era discounts; TSMC modest vs. Intel's big moves) Dynamic fully flipping in AMD's favor. TSMC raising advanced/sub-3nm prices 3-10% (some reports 3-7%) starting 2026, plus CoWoS hikes. Intel executed multiple server/CPU increases in 2026 (5-20%+ already; more in May and cumulative 30%+ planned). AMD following suit amid tightness, but TSMC has better cost control(only raise 3-7%), this will allow AMD to be more flexible and steal more market share Post-Milan, Intel's discounts eroded AMD's premium but they lost share anyway. Now Intel reverses while AMD benefits from TSMC efficiencies and superior products. This directly supports margin expansion and share gains in servers/AI. 6. NVIDIA supply control was 2023-2025; TSMC now separating capacity (2nm/3nm) for fairer allocation Peak shortages eased as TSMC expands aggressively (3nm/2nm sold out but ramping; CoWoS to 130k-150k wafers/month). NVIDIA/Apple take big early chunks, but TSMC allocates "fairly" to large loyal customers like @AMD (secured meaningful wafers for MI400; reports of 40-60% on certain lines). Node separation + Arizona fabs help. AMD's supply position has materially improved in 2026 toward 2030 7. OpenAI/Anthropic IPOs → push toward owning diversified hardware (including AMD) vs. pure NVIDIA rental; pressures NVIDIA margins long-term Both targeting 2026 IPOs (OpenAI potentially late-year at $800B-$1T; Anthropic earlier). NVIDIA has pulled back private investments as they go public. Hyperscalers already diversifying (Meta, Amazon, Google, Microsoft, Oracle deploying AMD Instinct at scale). IPO capital + discipline (usage caps, token pricing) will accelerate direct ownership due to lowest TCO, TDP, and $ per million token-efficient racks like AMD. OpenAI and Anthropic want to own the data center, while Jensen is pushing for more rental, which will increase Op Ex. Going public will mean more Op Ex control and rising Op Income. Conclusion: Dr. Lisa Su has delivered on both innovation and execution. Under her leadership, AMD has secured significant TSMC supply including scaled N2 capacity for MI400 series and strong CoWoS allocations starting Q1 2026 positioning the company to meet surging demand without the constraints Northland highlights. This supply security, combined with the fabless margin advantage, rising pricing power, TCO superiority, and hyperscaler diversification, directly dismantles the note’s core concerns around NVDA favoritism and 2027 resets. Northland’s caution is understandable given past cycles, but the data from capacity ramps and management commentary shows AMD is no longer the supply-constrained underdog. With MI350/MI400 ramps accelerating, EPYC share climbing, and hyperscaler CapEx still exploding, the multi-year AI + CPU opportunity looks intact and much larger than consensus assumes. May 5 earnings will likely provide fresh color on these ramps and 2026 guidance a potential catalyst for further upside. This is exactly the kind of high-quality compounder setup that rewards long-term conviction over near term noise. Not Financial Advice!

English

@The_AI_Investor Where I can your actual portfolio ? please, I m part of yours members

English

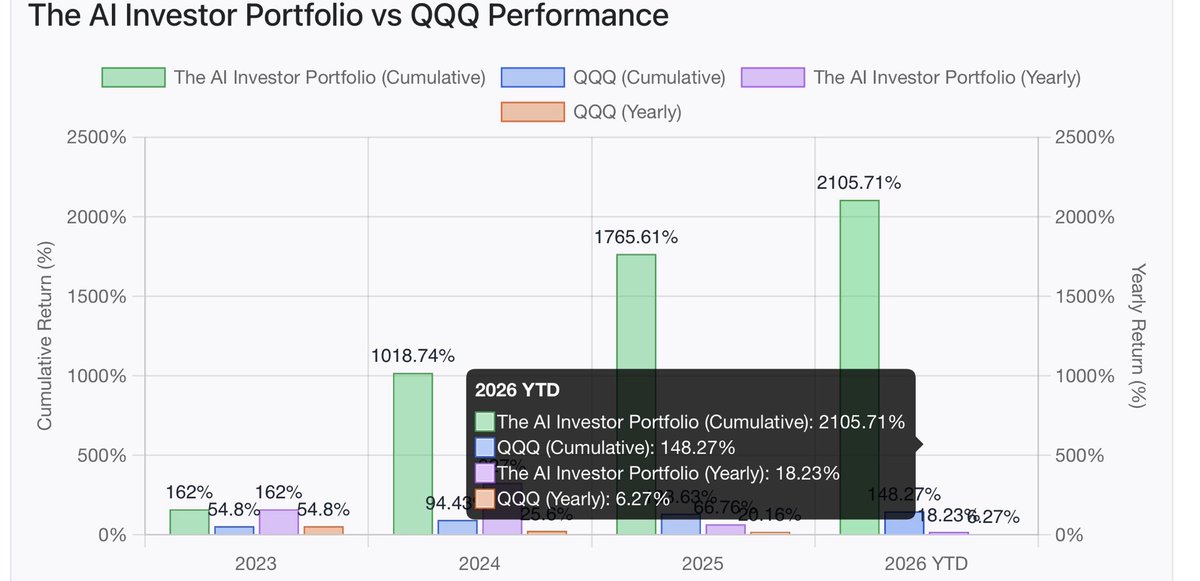

My Portfolio has just reached a new ATH

YTD % +18.23%

1Y % +228.20%

Non-NVDA AI stocks have been killing it. It could have been much higher if I had used more margin. I didn’t expect TACO to be that perfect.

Continue to 3x QQQ performance so far this year.

English

@HolySmokas RSI = 88 !!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

$AMD predictions for this week!

Who is brave enough to put an end of week number out there?

English