Sabitlenmiş Tweet

Bobimala

1.7K posts

Bobimala retweetledi

Bobimala retweetledi

I still can’t understand how Keeta $KTA a chain that has run a pilot with Visa and is the only blockchain ever listed on Visa’s Global Registry of Service Providers can have a market cap of just over $100 million.

Plus not to mention direct links/connections to Bank Of America (with potential pilot as well)

Connections to Stripe, Royal Bank of Canada (RBC), City National Bank,National Australia Bank, Charles Schwab and others just to name a few.

Not to even mention already had ran/still running as the authoritative record keeping system and running the internal ledgers for banks in over 50 regions.

I guess somethings just need to be handed on a plate for some people to truly digest and understand.

English

Bobimala retweetledi

if ezra is excited for 2026, then i’m really excited! i love what we’ve built in discord for open dialogue between the team and community about everything $KTA

join us discord.gg/keeta

English

Bobimala retweetledi

Bobimala retweetledi

Most financial institutions don't touch crypto because they can't.

Banks need private flows and verified accounts with full transaction attribution, which is opposite to what public blockchains offer.

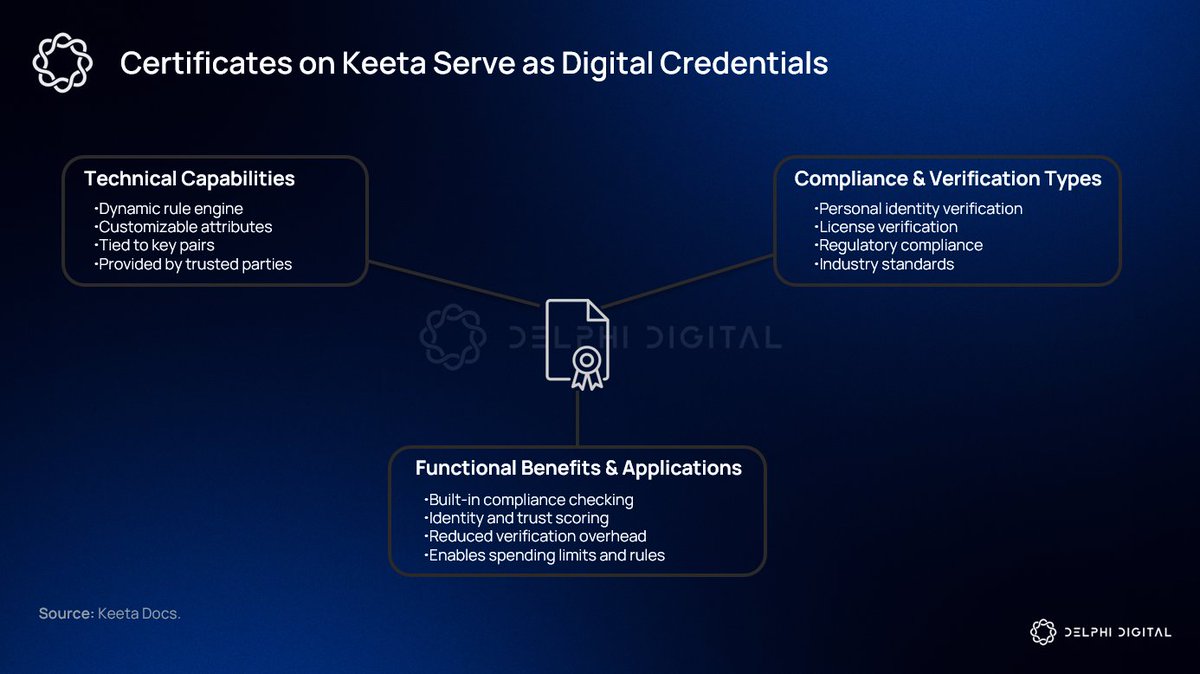

@KeetaNetwork is building for this gap. Their approach uses onchain identity certificates via the X.509 standard, the same cryptographic framework used across internet protocols). Wallets get tied to verifiable identity attestations without exposing the underlying personal data.

With selective disclosure, users can prove specific attributes (KYC status, jurisdictional permissions, business licenses) to counterparties without revealing everything else. Compliance is enforced at the protocol level while pseudonymity is preserved on the public ledger.

Keeta has also built a permission system around asset issuance that includes jurisdictional restrictions, KYC-gated transfers, and role-based permissions for custodians. These features are standard in traditional finance but still missing from most crypto infrastructure.

Keeta is building the compliant rails institutions need before they can move onchain.

English

Bobimala retweetledi

Keeta is building the compliant rails institutions need before they can move on-chain.

$KTA

Delphi Digital@Delphi_Digital

Most financial institutions don't touch crypto because they can't. Banks need private flows and verified accounts with full transaction attribution, which is opposite to what public blockchains offer. @KeetaNetwork is building for this gap. Their approach uses onchain identity certificates via the X.509 standard, the same cryptographic framework used across internet protocols). Wallets get tied to verifiable identity attestations without exposing the underlying personal data. With selective disclosure, users can prove specific attributes (KYC status, jurisdictional permissions, business licenses) to counterparties without revealing everything else. Compliance is enforced at the protocol level while pseudonymity is preserved on the public ledger. Keeta has also built a permission system around asset issuance that includes jurisdictional restrictions, KYC-gated transfers, and role-based permissions for custodians. These features are standard in traditional finance but still missing from most crypto infrastructure. Keeta is building the compliant rails institutions need before they can move onchain.

English

Bobimala retweetledi

Bobimala retweetledi

2025: Take a look at all the product, company, thought leadership, and customer blogs we shipped this year ↓

2026: in development! goo.gle/4pYqD88

English

Bobimala retweetledi

Bobimala retweetledi

as i said, we’re just getting started ;)

Keeta@KeetaNetwork

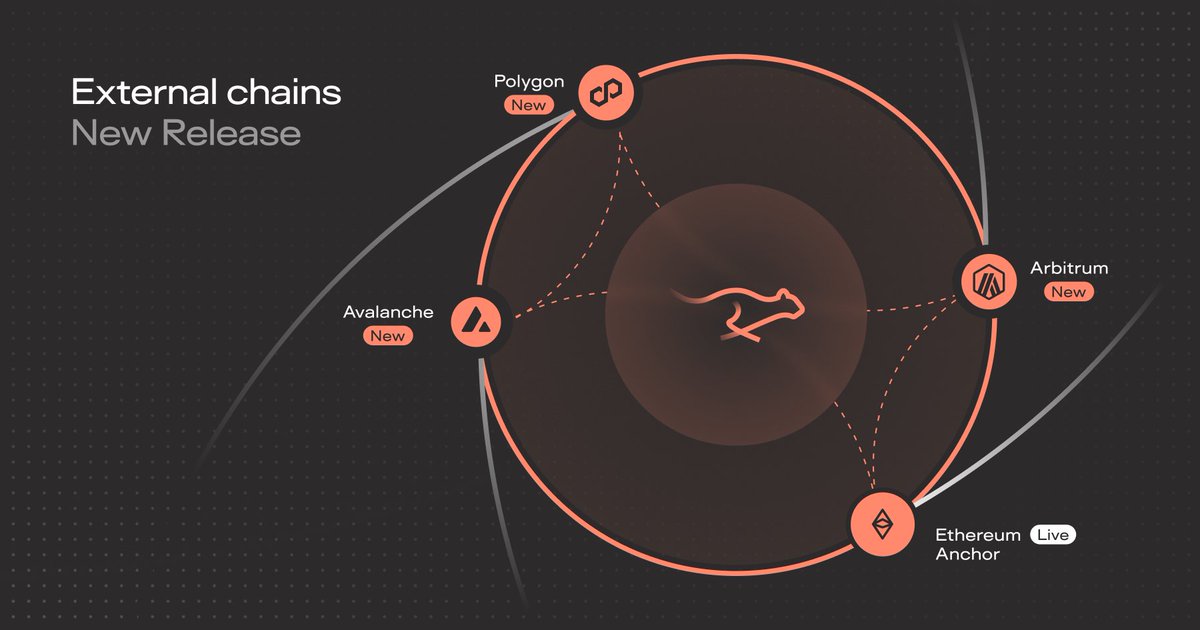

Keeta Network continues to grow. USDC on Keeta Network can now be sent to and from Avalanche, Polygon, and Arbitrum. USDT and PYUSD on Ethereum can now be sent to and from USDC on Keeta Network. More routes. More liquidity. More coming soon. $KTA

English

Bobimala retweetledi

Coins have received no bid since 10/10. Many speculating a large entity is unwinding billions, when that is over the coins will be bid again $BTC $ETH $KTA

English

Bobimala retweetledi

Keeta stands tall here, positioned directly in the middle as an enterprise grade institutional blockchain

$KTA

Delphi Digital@Delphi_Digital

The majority of financial institutions are still hesitant to approach crypto despite the change in sentiment and regulation. The main barrier is the mismatch between public, pseudonymous ledgers and regulatory requirements like KYC and private transfers. For example, the Bank Secrecy Act requires institutions to know the sender, the recipient, and the purpose of every transfer. They must maintain the ability to audit records that tie every transaction to a verified customer or legal entity. Financial institutions also require private payments. Banks cannot send client flows where counterparties and random observers can analyze every activity on a public ledger. What's required is private flows and public accounts. As it stands today, most existing chains are not an option with public flows and anonymous accounts. An institutional blockchain would need to fall somewhere in the middle.

English

Bobimala retweetledi

Bobimala retweetledi

Great partnership for $KTA

@reppo x @KeetaNetwork 🔥

Reppo@reppo

Quick update on the private subnets: Accepting USDC as payment turned out to be far more painful than expected. Almost every major centralized API provider (*retracted*, *retracted*, etc.) requires a US entity, which we don’t have. We were told last minute that there is a compliance bottleneck, even if we wanted to accept USDC without an onramp.... In the short term, we’re integrating NOWPayments now so we can move forward without blocking users. In the medium term, we’ll use @KeetaNetwork to build our own payment stack, removing reliance on centralized gateways altogether. Why Keeta? 1. Non-custodial 2. No US-entity gatekeeping 3. Protocol-level settlement 4. Fewer compliance chokepoints Not ideal, but this gets us shipping — and long-term, it’s the stronger architecture. Also if someone has a intro to Keeta team, slide in our DMs. Appreciate everyone’s patience. 🚀

English

Bobimala retweetledi

What keeps me interested in Keeta ( $KTA ) isn’t price action, it’s the design choice.

Instead of trying to be everything at once, Keeta focuses on one thing: fast, efficient settlement. No layers, no extra narratives, just moving value cleanly. That restraint is rare in crypto.

The risk is obvious, adoption has to follow. But if on-chain finance eventually values simplicity and speed over complexity, Keeta’s approach makes a lot of sense to me.

English

Bobimala retweetledi

@The_WhalePod @BankofAmerica Buying $KTA here is like getting $LINK at ICO. Easy bet. Ignore short term noise and buy.

English

Bobimala retweetledi

Keeta’s foundation is coming together. Here’s where we are today and what’s ahead:

Public partnerships

• Footprint: Verified, reusable KYC certificates on-chain

• SOLO: First blockchain-native credit bureau, unlocking on-chain credit and real-world lending

• Agora: Compliant, fiat-backed stablecoins on Keeta Network

• Bridge: Bank-to-Keeta connectivity for fiat deposits and withdrawals

Live in the Keeta Wallet

• Non-custodial wallet with full user control

• Send & receive on-chain payments

• Atomic swaps & token manager

• On-chain KYC certificates

• Fiat on/off via Bridge

• Fast, low-fee transfers

What’s coming next

• More partners & anchors

• DEX for on-chain asset exchange

• Keeta Pay: Mobile & web banking experience

• Keeta Card: Spend assets anywhere

• And more, built on Keeta’s high-throughput, low-fee network

This isn’t about one feature. It’s about building a complete financial network. 2026 is going to be epic.

$KTA

English

Bobimala retweetledi

@Brown_Thunder76 Also, Keeta offers all partners to participate equally via the anchor concept.

If you are a fintech, an issuer, or a bank, you may simply connect to the @KeetaNetwork. The independent interoperability network, the most scalable out there.

English

Bobimala retweetledi

Good time to load up on $KTA

Absolute bottom is here

Community is full of whales that will support the chart

KTA is one of those layer 1 projects that will bounce back even if we enter a full blown bear market that takes us to 20k

Make sure to join the $BASE call channel for more gems. Going private at 1000 members.

t.me/BASECALLCHANNEL

English

Bobimala retweetledi

@juancenacrypto @ericschmidt With growing use cases and adoption, $KTA will grow a lot.

With Binance/Robinhood listing or Eric's mention/tweet, $KTA would grow exponentially.

English