@StockMKTNewz Same energy as every other “this time it’s different” moment that ended up being a buying opportunity

The market always recovers and better be invested

@TrumpDailyPosts Easy: ignore Iran's blockade of the Strait of Hormuz, and ships can pass through the strait as usual. If the Iranian IRGC attacks any ship and causes damage, Iran will seize twice the amount of its assets as compensation. In other words, Iran will provide insurance compensation.

We've uploaded a fruit fly. We took the @FlyWireNews connectome of the fruit fly brain, applied a simple neuron model (@Philip_Shiu Nature 2024) and used it to control a MuJoCo physics-simulated body, closing the loop from neural activation to action.

A few things I want to say about what this means and where we're going at @eonsys. 🧵

To ensure the safety of shipping in the Strait of Hormuz, the U.S. military had to gain control of the Iranian island of Qeshm, which could require tens of thousands of ground troops.

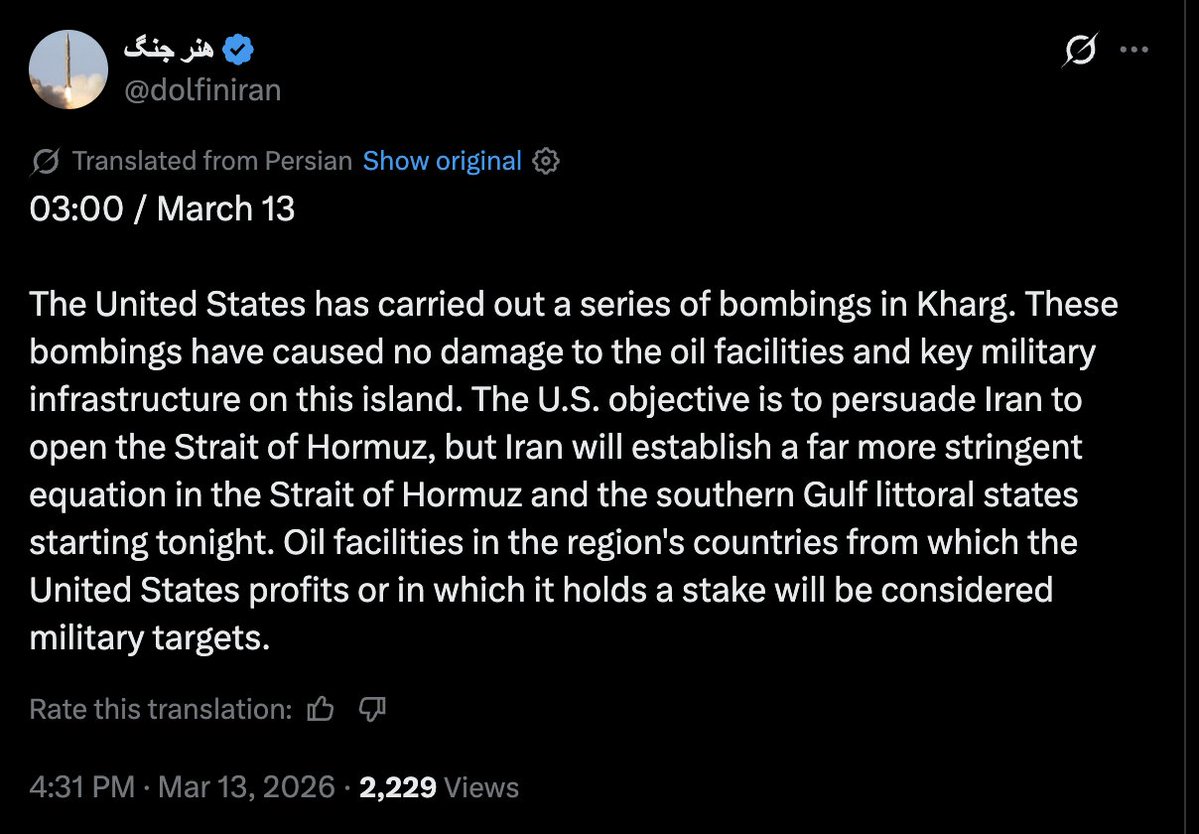

The quoted account is run by an adviser to Qalibaf who is in charge of the war in Iran. It appears the Iranian government is threatening to escalate the conflict by attacking oil facilities in the region.

@MarioNawfal It's useless. After Israel (and the USA) invented the "decapitation strike" model, where leaders are sent first, dictators in authoritarian countries will have to think twice before starting a war. From now on, wars will be battles between leaders, not sacrifices of people.

🇰🇵 With the world glued to the Middle East, Kim Jong Un apparently got FOMO, so he fired cruise missiles off his new 5,000-ton destroyer just to remind everyone he still exists.

Because nothing says “don’t forget about me” like a strategic weapons demo.

🔥🎇Next Tuesday night is Chaharshanbe Suri, Iran's annual fire festival. Large crowds come out and the fire crackers are intense. This could be a major test of whether people would reclaim the streets again and potentially an opportunity.

@michaelxpettis So the current government of the PRC is a barrier to healthy growth and must at some point be replaced with the triple and indivisible liberties of free markets, freedom of expression, and free elections.

The Economist argues here that China should set a higher GDP growth target because the current target (4.5-5.0%) is too low and will make the economy’s current problems, including surging debt, worse. “The proof,” it says, “lies in China’s prices. They have been falling, by some measures, for three years. This persistent deflation is a worry in itself—it increases the burden of debt, limits the room for monetary easing and mutes price signals, given the reluctance even in China to cut wages in money terms. It is also a sign of a deeper problem. It suggests that output is falling short of what the country could produce if its capital and labour were more fully employed.”

But this is the wrong way to look at the Chinese economy. Chinese deflationary pressures are not an unexpected aberration but rather a consequence of its current growth model.

Falling prices suggest not that there is a shortfall in output but rather that output is growing faster than what domestic – and, increasingly, foreign – demand can absorb. In a system in which excessively high GDP growth targets are met mainly by increasing investment in infrastructure and manufacturing (and, not too long ago, in the property sector), it seems a little perverse to argue that boosting output in a system already suffering from excess capacity in property, infrastructure and manufacturing will cause prices to rise.

If anything, increasing investment in an already investment-heavy economy will tend to worsen the very imbalances that have produced falling prices in the first place. When production capacity expands more rapidly than the purchasing power of households and businesses, prices must adjust downward to clear inventory that banks are increasingly reluctant to finance. In China’s case, the imbalance is reinforced by the structure of the economy, which systematically channels resources toward investment and production rather than toward household income and consumption.

The article also argues that a higher GDP growth target will make it easier to manage the country’s debt burden. But this assumes that there is no connection between GDP growth and the debt burden.

In fact, the opposite is true. The overwhelming majority of lending in the Chinese financial system is used to fund investment, with a very small share going to fund consumption. If investment were healthy, it should be impossible in such a financial system for the debt-to-GDP ratio to rise – except occasionally in the very short term – because the investment itself would generate faster increases in economic value than in debt-servicing costs.

But over the past fifteen years China has suffered from among the fastest increases in the debt-to-GDP ratio in history. This is strong evidence that a rising share of debt is funding non-productive manufacturing capacity, infrastructure and property. More generally, there is a pretty strong correlation between the investment contribution to Chinese growth and the rise in the country’s debt-to-GDP ratio.

To put it another way, China can only set GDP growth targets much above a sustainable GDP growth level – perhaps around 2–3 percent – by accelerating credit creation. In that case, a higher GDP growth target would require even faster growth in debt, and would raise the debt burden further rather than reduce it.

The article does hedge against the likelihood of increasing non-productive investment by arguing that a higher GDP growth target could be achieved by directing resources to households to boost consumption. While this sounds attractive on paper, and while China has spoken for nearly a decade about the need to rebalance with an acceleration in consumption growth, there is a reason why this has proved so difficult. There is also a reason why no country in China’s position has ever managed to rebalance without a slowdown – or even a contraction – in growth.

In rapidly growing economies where high investment is powered by even higher savings, low consumption is not an accident or an oversight. It is fundamental to the way the economy is structured. Businesses and governments receive a disproportionately large share of GDP, while households receive a disproportionately small share. These imbalances are embedded in the mechanisms that drive growth.

If China is to boost the consumption share of GDP, it would require reversing the transfers implicit in the national distribution of income. This could be done by raising wages, raising interest rates, increasing the value of the currency, raising current social-safety-net payments (future promises will not affect current consumption except after many years of credibility building), and/or increasing other forms of household income. In each case, however, the policies that increase household income simultaneously reduce the resources available to subsidize investment and manufacturing.

What many analysts fail to grasp about Chinese manufacturing – just as they failed to understand Japanese manufacturing in the 1980s, is that while China’s very large manufacturing sector is globally competitive, it is also far less efficient than most analysts assumed. If it were genuinely efficient, it would be profitable without subsidies. Yet in many cases it is only marginally profitable despite large transfers that directly and indirectly subsidize its costs.

Among these transfers are an undervalued currency, abundant and cheap credit, artificially low interest rates on household savings, and government overspending on logistics, infrastructure and transportation networks that reduce costs for manufacturers. These policies boost manufacturing competitiveness, but they do so by transferring income from households to producers.

If the global competitiveness of China’s manufacturing sector depends on these direct and indirect transfers, reversing those transfers in order to raise household income would necessarily undermine that competitiveness. The process of rebalancing therefore requires a structural shift away from investment and manufacturing toward consumption and services.

Japan provides a useful example. Between 1991 – when Japan’s consumption share of GDP bottomed out – and 2008, Japan succeeded in increasing its consumption share by roughly 10 percentage points of GDP. But during that same period Japan not only lost roughly half its share of global GDP, it also experienced a decline of roughly one-third in the manufacturing share of its economy. This implies a drop in its share of global manufacturing of roughly two-thirds.

These were not coincidental; they were the nearly-inevitable consequences of rebalancing income toward households.

For China, the implication is straightforward. Increasing the consumption share of GDP necessarily implies slower overall growth and a smaller manufacturing share of the economy. The idea that China can simultaneously dedicate resources to increasing output while dedicating even more resources to increasing demand is hard to reconcile with either logic or historical experience.

My conclusion, therefore, is the opposite of the Economist’s. Chinese deflationary pressures, its huge trade surpluses, its surging debt burden, and its increasingly unviable investment in property, infrastructure and manufacturing are all direct consequences of a political obsession with too-high GDP growth targets. Maintaining these targets requires ever-increasing credit expansion and ever-greater investment in sectors that are already suffering from excess capacity.

It is not an accident that no country with Chinese-style imbalances has ever adjusted without a slowdown – or even a contraction – in GDP growth. Rebalancing toward consumption requires shifting income from producers to households, and this necessarily reduces the pace of investment-driven growth.

For this reason, raising China’s GDP growth target would almost certainly make the underlying problems worse rather than better. The real challenge for Chinese policymakers is not how to increase growth targets, but how to accept lower growth – and a smaller share of global manufacturing – while restructuring the economy and rebalancing the domestic drivers of growth.

economist.com/leaders/2026/0…

Will the war between the US/Israel, and Iran pose a spillover risk? That depends on how long it takes to end. If, as Trump has stated, it ends in four weeks and middle east regions return to pre-war conditions, then it's fine; otherwise, the spillover risk exceeds 50%. No WW3!