Sabitlenmiş Tweet

Clare Capital

7.3K posts

Clare Capital

@ClareCapital

Investment Bankers. Tweets from Mark Clare...

New Zealand Katılım Ocak 2009

553 Takip Edilen1.1K Takipçiler

This is definitely 'chart of the day'... It covers a wide range of potential outcomes.

Marc Andreessen 🇺🇸@pmarca

English

Clare Capital retweetledi

For the first time in venture history, three distinct channels share the liquidity burden roughly equally.

A decade ago, secondaries barely registered. They accounted for roughly 3% of exit value in 2015. Today they claim 31% : nearly $95b in the trailing twelve months.

The shift accelerated after 2021’s IPO bonanza. When public markets closed their doors in 2022, investors found alternative routes. Secondaries absorbed demand that would have flowed to traditional exits. When Goldman Sachs acquired Industry Ventures, the transaction signaled secondaries have arrived. Morgan Stanley followed with EquityZen, then Charles Schwab announced its acquisition of Forge Global. Wall Street recognized the structural change before most of venture did.

This matters for founders & investors. When IPOs dominated exits, fund models assumed a small number of public offerings would generate the bulk of returns.

Now liquidity arrives through multiple doors. A founder might sell secondary shares to patient capital while the company remains private. A GP might move positions through continuation vehicles. An LP might trade fund stakes on an increasingly liquid secondary market.

The 830 unicorns holding $3.9t in aggregate post-money valuation cannot all exit through IPOs. The math doesn’t work. At 2025’s pace of 48 VC-backed IPOs, clearing the unicorn backlog would take seventeen years. Secondaries provide a release valve that traditional exits cannot.

Companies like OpenAI have embraced this reality, running employee tender offers while voiding unauthorized secondary transfers. The largest private companies now manage their own liquidity programs rather than waiting for public markets.

Today, secondary liquidity concentrates in the top 20 names. SpaceX, Stripe, OpenAI. For the founder of company #50, the secondary market remains largely theoretical. For secondaries to succeed as a broad asset class, buyers must underwrite positions in companies without household recognition. As the market grows, this coverage gap becomes opportunity.

For LPs starved of distributions since 2022, the expansion of secondary channels offers hope. The $169b in cumulative negative net cash flows needs somewhere to go. More exit paths mean more opportunities to return capital.

When a Series B employee asks about liquidity today, the answer isn’t “wait for the IPO.” It’s “we’re planning a tender offer next year.”

A decade ago, secondaries were a footnote. Now they’re infrastructure. Liquidity flows where it can, not where tradition suggests it should.

tomtunguz.com/a-third-a-thir…

English

Clare Capital retweetledi

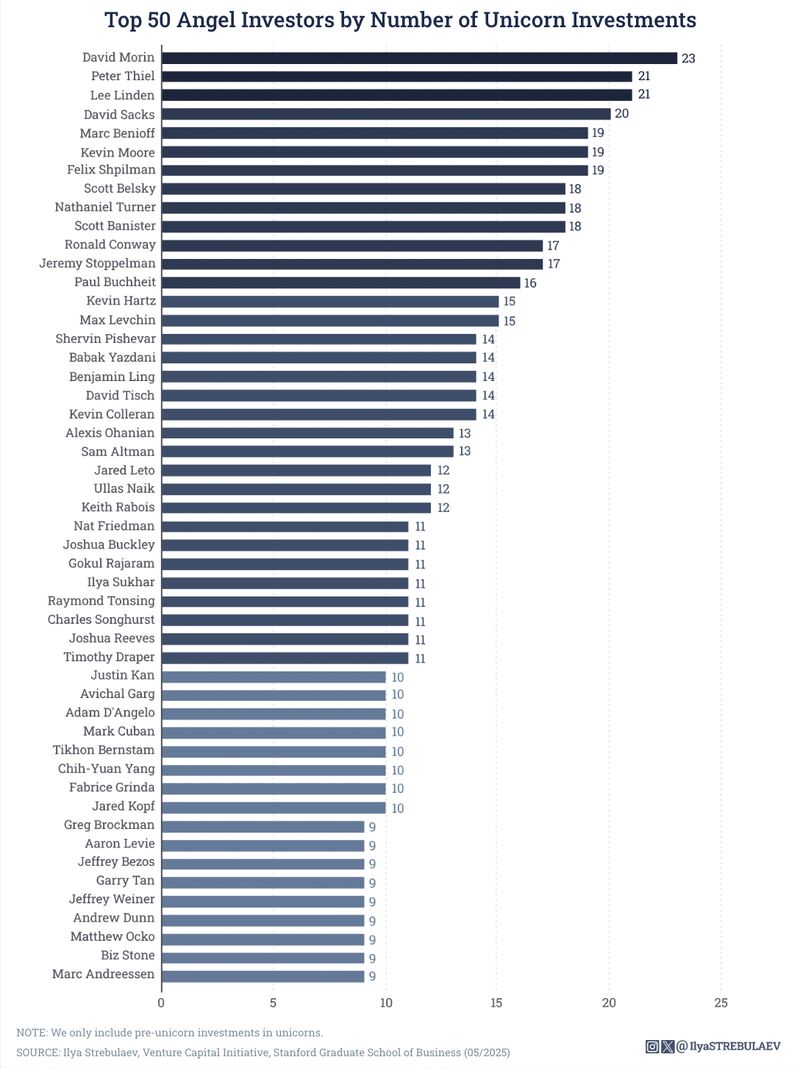

A Stanford professor analyzed 1,000's of angel investments to find out who's had the MOST unicorns.

The results are fascinating.

- David Morin tops the list with 23 unicorns

- Peter Thiel and Lee Linden follow with 21 each

- David Sacks at 20

- Marc Benioff at 19

A few things that stand out:

1) Almost every top angel was a founder or exec at a large tech company first. The clear signal here - they were mostly operators who earned their access.

2) Many co-invested together repeatedly. Thiel, Sacks, and Levchin all overlapped at PayPal and went on to back the same unicorns (Facebook, Airbnb, Palantir Technologies, SpaceX).

3) No women appear in the top 50. Sad.

4) The entry threshold to make this list is 9 unicorns (nuts!). The average unicorns across the top 50 is 13 (more nuts!).

I share this for folks to have inspiration to angel invest themselves!

There has NEVER been a better time - we are at a major tech inflection point.

If you're thinking about angel investing and forming angel syndicates, you should check out Verivend. Automated capital calls, one-click funding for co-investors, real-time visibility into who's in. Seamless software with a great team to hold your hand through it.

Try it yourself: lnkd.in/grrJxqxq

Full credit to Ilya Strebulaev and his team at the Stanford for this research.

English

Clare Capital retweetledi

Josh Harris bought the Washington Commanders for $6.05B

Here are the top slides from the deal:

English

Clare Capital retweetledi

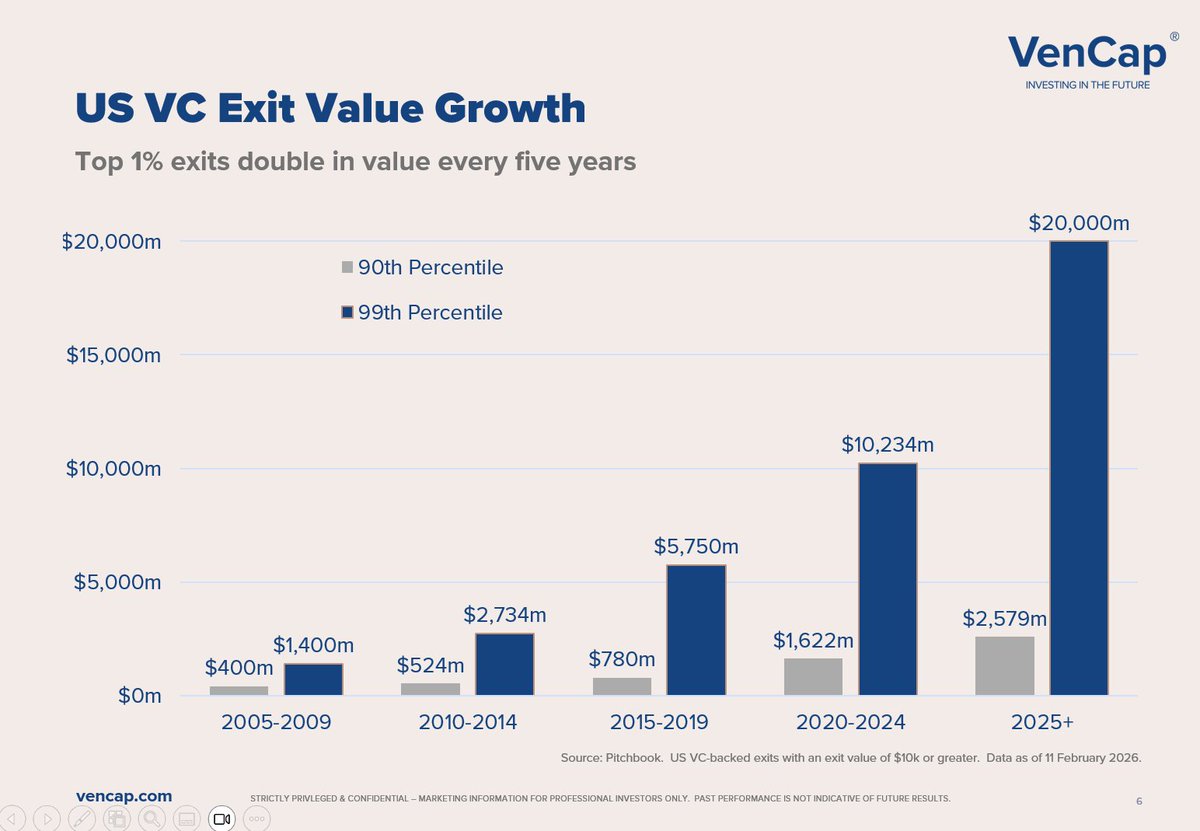

Thought it was worth updating our analysis of top 1% exits post 2024. The trend is continuing and may even be accelerating by the time we hit 2029...

English

Clare Capital retweetledi

Sequoia distributed over $50B while Roelof was the steward running Sequoia US since 2017

One of the first things @roelofbotha coached me on when I joined Sequoia was to look at each fund’s “write off rate”

Any fund with a write off rate below 40% wasn’t taking enough risk

Scott Kupor@skupor

Is it too much to ask that @WSJ reporters who cover finance actually understand the asset classes they purport to report on? @roelofbotha and @sequoia are world class investors who have generated amazing returns for their LPs. VC is not a downside minimization asset class, but an unlimited upside capture one.

English

Clare Capital retweetledi

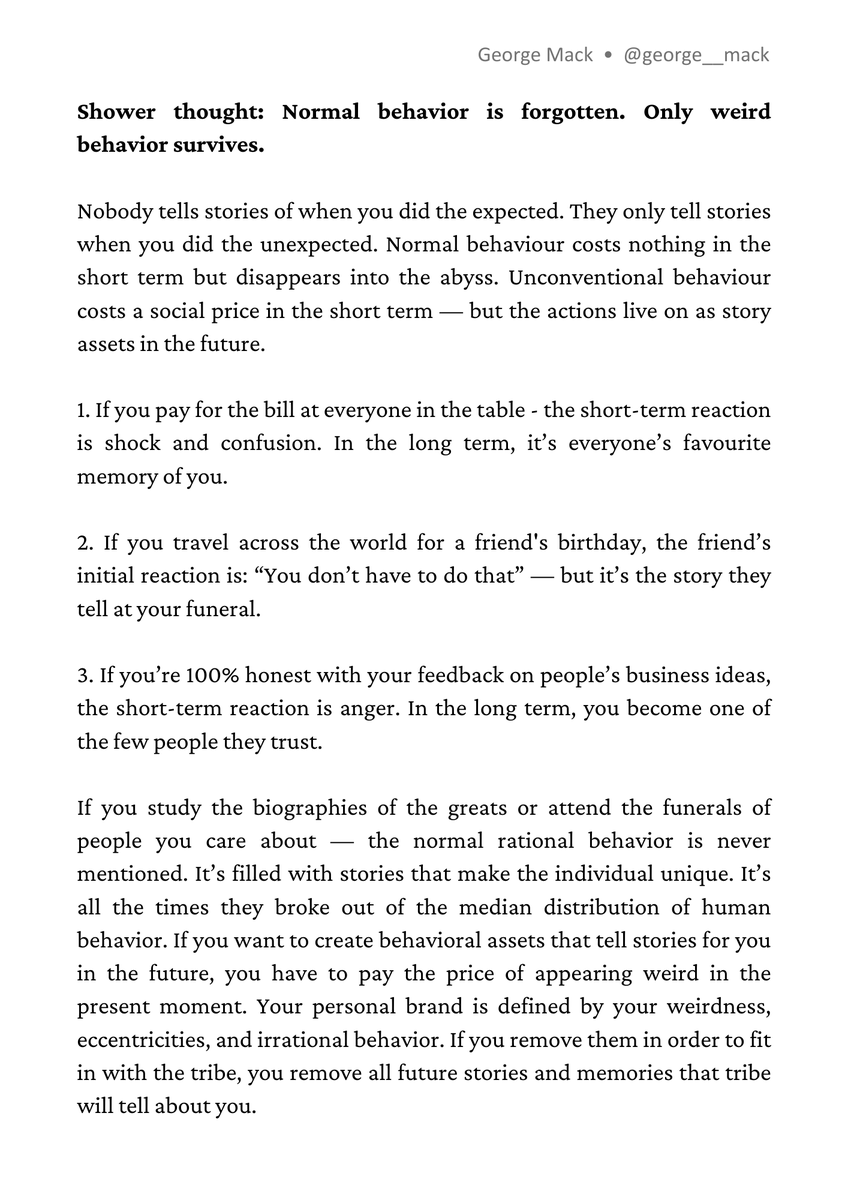

All normal behaviour is forgotten. Only weird behaviour survives.

Jeremy Giffon@jeremygiffon

A pretty much constant paradox is that we expect outlier outcomes from people that we demand act in normal, average ways. We love geniuses after they do the great thing, but we basically loath and harass them if they act in uncouth ways before hand.

English

Clare Capital retweetledi

Why is the United States so much better at creating successful companies than elsewhere? @JeffBezos has a very good answer:

English

Any time someone looks closely at airline economics, there is ALWAYS some crazy insight. Making money flying passengers is a hard business. You gotta be getting creative to turn a dime...

English

Huge congrats @AucklandCity_FC, fantastic result. I (Mark Clare) played at the level @AucklandCity_FC do in the @NZ_Football pyramid back in the 1990s. A lot of proud @NZ_Football players, current and former, out here today.

FIFA Club Football@FIFACF

A draw between @AucklandCity_FC and @BocaJrsOficial to close out Group C. 🤝

English

This is bonkers, but you can see where things are headed...

PJ Ace@PJaccetturo

Kalshi hired me to make the most unhinged NBA Finals commercial possible. Network TV actually approved this GTA-style madness 🤣 High-dopamine Veo 3 videos will be the ad trend of 2025. Here’s how I made it in just TWO DAYS 👇🏼 (Prompt included)

English

Really really good thread. We operate (and negotiate) in a small market (New Zealand and with international parties). There is a reason why our firm strategy is "long-term games with long-term people". We are paid to get outcomes, but we typically will see counterparties again...

Mark Suster@msuster

Some notes on Negotiations 1/ When you finish any complex deal you will feel fatigued and worn out. It sometimes feels hard to celebrate. The best deals feel this way. Complex negotiations require compromises. When both (or all) parties make concessions nobody feels great. Everybody felt like they gave more than they wanted. And all wish the other party would have folded easier. That’s the definition of a good negotiation

English

This observation is right on the money...

Omar@TheOneandOmsy

This NYU paper basically says: retail investors spend 6 minutes researching a trade - mostly just looking at charts What most people actually want is an entertainment platform. Not a finance app The best intimately recognize this and are building entertainment super-apps dressed up as brokerages

English

Clare Capital retweetledi

"They're called collateralized music festival loan obligations... and they're awesome"

unusual_whales@unusual_whales

60% of general admission ticket buyers at Coachella used Buy-Now-Pay-Later to finance their tickets, per Billboard.

English

Clare Capital retweetledi

We are selling pad thai in installments to willing buyers at the current fair market price

More Perfect Union@MorePerfectUS

DoorDash and Klarna have signed a deal where customers can choose to pay for food deliveries in interest-free installments or deferred options aligned with payday schedules.

English

Clare Capital retweetledi

"Alphabet (Google and YouTube) generates more revenue from advertising than New Zealand’s GDP." 🤯

- @ClareCapital

English

Clare Capital retweetledi

When you perform you don’t need a size up narrative and can remain boutique

Arfur Rock@ArfurRock

Weirdly underreported...USV raised a new fund! Here's their net performance data from their latest deck. One of the greatest of all time.

English