This information is courtesy of my good friend @TheDailyGold who puts out some of the best content for the miners.

English

Collin Kettell

1.2K posts

@CollinKettell

Founder & CEO of Palisades Goldcorp $PALI.V, New Found Gold Corp $NFG.V $NFGC , Nevada King Gold Corp $NKG.V $NKGFF. Gold investor & enthusiast.

Has to be my fave comment of the week 👇👇. Ladies & gents, I give you @CollinKettell and the intellectual capacity of the modern mining CEO. Apparently, being paid by mining cos to write about mining cos is the same as being paid by readers to write on mining cos.

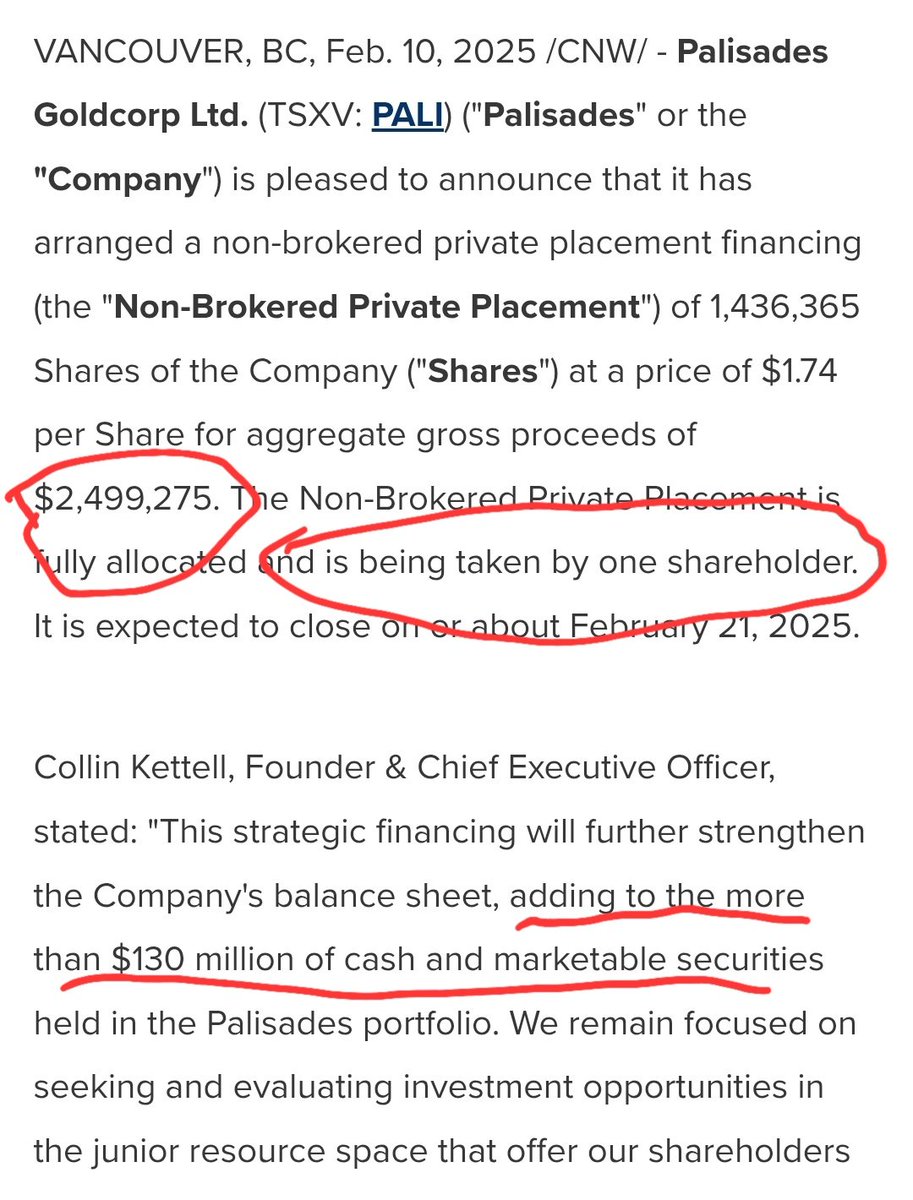

This is my favourite bit of Denis Laviolette's latest pay2play scheme:

I have been surprised how low US long-term rates have remained in light of structural changes that are likely to lead to higher levels of long-term inflation including de-globalization, higher defense costs, the energy transition, growing entitlements, and the greater bargaining power of workers. As a result, I would be very surprised if we don’t find ourselves in a world with persistent ~3% inflation. From a supply/demand perspective, long-term Treasurys (T) also look overbought. With $32 trillion of debt and large deficits as far as the eye can see and higher refi rates, an increasing supply of T is assured. When you couple new issuance with QT, it is hard to imagine how the market absorbs such a large increase in supply without materially higher rates. I have also been puzzled as to why the @USTreasury hasn’t been financing our government in the longer part of the curve in light of materially lower long-term rates. This does not look like prudent term management in my opinion. Then consider China’s (and other countries’) desire to decouple financially from the US, YCC ending in Japan increasing the relative appeal of Yen bonds vs. T for the largest foreign owner of T, and growing concerns about US governance, fiscal responsibility, and political divisiveness recently referenced in Fitch’s downgrade. So if long-term inflation is 3% instead of 2% and history holds, then we could see the 30-year T yield = 3% + 0.5% (the real rate) + 2% (term premium) or 5.5%, and it can happen soon. There are many times in history where the bond market reprices the long end of the curve in a matter of weeks, and this seems like one of those times. That’s why we are short in size the 30-year T — first as a hedge on the impact of higher LT rates on stocks, and second because we believe it is a high probability standalone bet. There are few macro investments that still offer reasonably probable asymmetric payoffs and this is one of them. The best hedges are the ones you would invest in anyway even if you didn’t need the hedge. This fits that bill, and also I think we need the hedge.