Sabitlenmiş Tweet

Whether you are long or short T1 Energy (TE), we think everyone can agree that US taxpayer money should NOT be going to China at all.

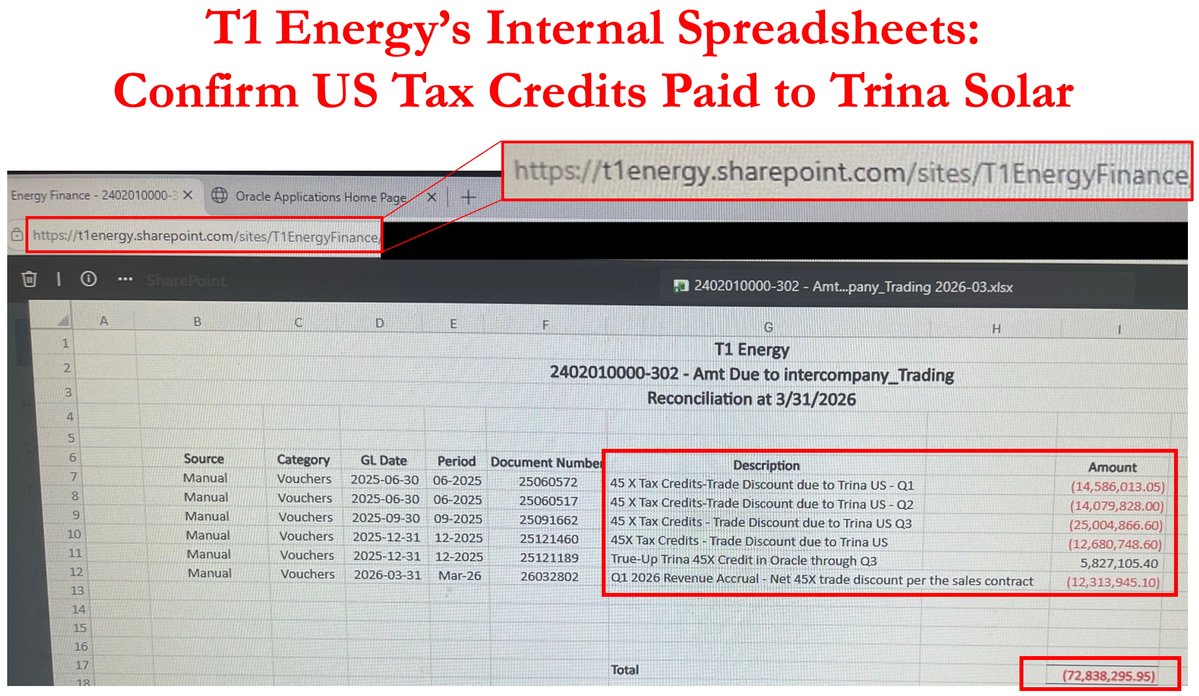

Today we reveal internal documents from T1 Energy which prove that T1 has been funneling US Solar Tax Credits to a Chinese Co, Trina Solar. T1 has been caught red-handed, and a whistleblower provided us the receipts to prove it.

T1 has been busted sending tens of millions of US Tax payer dollars to a company that the US Dept of War has recently labeled a “Chinese Military Company"

See for yourself how many tens of millions of US tax payers hard earned dollars that T1 has funneled to their Chinese business partner quarterly.

T1's internal financials even reveal that they are planning to keep paying out US Tax Credits to China in FY 2026 if they receive the payouts.

We also uncovered that T1 Energy’s has been misleading investors about where they are licensing their IP from. They claim to be paying for IP from a new Singaporean IP partner, Evervolt. BUT internal documents show no sign at all of Evervolt.

However, the books and records do show T1 Energy still accruing IP payments to Chinese partner, Trina Solar. These payments completely invalidate the FEOC lies that T1’s management has been spinning.

We are short T1 Energy and think that funneling US tax dollars to China is unpatriotic and appalling.

English