Commanders!

658 posts

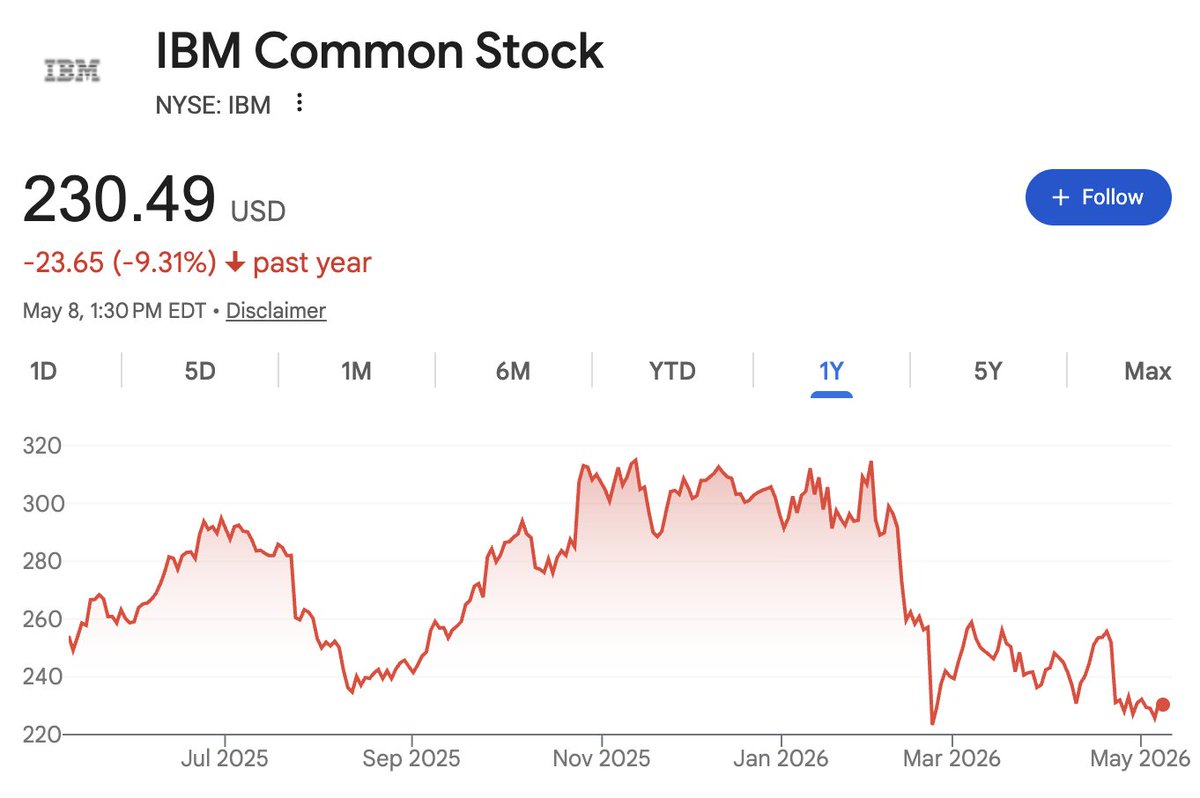

$IBM the next CPU play like $QCOM

Was one of the first to callout $QCOM but $IBM may be an overlooked way to play the CPU and memory shortage because it benefits from the infrastructure problems AI creates, not just from selling more chips.

As AI agents scale across enterprises, they dramatically increase demand for CPU cycles, memory, and constant backend processing (databases, workflows, retrieval, orchestration).

IBM’s advantage is that zSystems and Power Systems are built for consolidation: they run massive workloads with very high memory capacity and utilization on fewer machines. Instead of adding thousands of standard servers, enterprises can compress workloads into fewer IBM systems, reducing server sprawl, power usage, and memory duplication.

zSystems dominate mission-critical transaction environments (banks, governments, payments), while Power Systems handle large-scale enterprise compute and data workloads. watsonx extends this into AI deployment inside those same environments.

So the core idea is AI agents increase infrastructure demand, but $IBM benefits when that demand forces companies to prioritize efficiency especially during shortages

English

@bricked_trades HOLY! Your FSLY CALLS MADE ME BANK! How can I join you bro??

English

Commanders! retweetledi

best value 2026 NFL draft classes

1. Commanders

2. Panthers

3. Colts

4. Bengals

5. Jets

6. Giants

7. Buccaneers

8. Raiders

9. Falcons

10. Chiefs

see pic for 1-32 plus methodology

READ FULL ANALYSIS:

sharpfootballanalysis.com/analysis/2026-…

team-by-team & round-by-round analysis to follow 🧵

English

Commanders! retweetledi

The Commanders were below average in this metric in the 2023 draft and again in 2024, consistently reaching for players.

But last year, Washington finished #11.

This year, they finished No. 1 in the NFL in terms of draft capital over expected.

Washington didn’t have much capital, but it grabbed value early and often.

It started in Round 1, when Sonny Styles slipped from an expected top-five pick to the Commanders at No. 7.

With Friday’s only pick, the Commanders drafted WR Antonio Williams in Round 3 at No. 71 when he was expected to go at No. 66.

But their Saturday picks flashed even more value.

In Round 5, they took EDGE Joshua Josephs at No. 146 when he was expected to go No. 77.

In Round 6, they drafted RB Kaytron Allen at No. 186 when he was expected to go No. 130.

Later that round, they grabbed C Matt Gulbin from Michigan State at No. 208 when he was expected to go No. 168.

This was an exercise in maximizing draft capital and making more out of less by drafting players the vast majority of evaluators expected to go earlier in the draft.

English

Commanders! retweetledi

- Love, Delane, Styles, Downs, or Tate at 7

- JD5 mvp season

- Top 10 defense

- Healthy Scary Terry

- Trey Amos as CB1

- Luvu bounce back season

- Mikey bounce back season

English

@john_keim @Schultz_Report Dear Adam Peters,

I would like to apologize for doubting your legendary skills. Thank you for resigning the greatest guard of all time @BigChrisPaul. Commander nation loves you

English

Washington is re-signing guard Chris Paul to a one-year deal, a source confirmed @Schultz_Report's report. Paul wanted to test the market; Washington gets back someone who started the final 15 games at guard and did a solid job.

English

@john_keim @NickiJhabvala Well he’s here now let’s see what White can do for us 🔥

English

.@NickiJhabvala asked Rachaad White if Wash was his 1st choice (b/c of Jayden Daniels). He said: "Obviously one of my top choices. I thought it would be great to play with my best friend. 1st choice? Probably not, but I'm happy with the decision I made. I'm grateful to be here."

English

English

@john_keim @TomPelissero Cool now resign Washington Commander legend Chris Paul

English

Washington is re-signing veteran OL Trent Scott per @TomPelissero. Scott has been with Washington since 2023. He's started six games in his first three years with the Commanders.

English

Commanders! retweetledi

Commanders! retweetledi

The #Commanders are hiring former NFL QB and rising assistant coach David Blough to be their new offensive coordinator, sources say.

The #Lions showed real interest in Blough, and Washington acted fast to hire one of the NFL’s youngest and brightest offensive minds. Big hire.

English

And this — a change of D.C. in D.C.: Joe Whitt Jr. also is out as the Commanders defensive coordinator, per sources.

English

Just in: The #Commanders are mutually parting ways with OC Kliff Kingsbury after two seasons.

English

Commanders! retweetledi

Commanders! retweetledi

Oracle [ $ORCL ] earning results and its effect on the neocloud sector like $NBIS & $IREN:

Oracle reported earnings with a beat on EPS and a record backlog but, dropped 12% after hours.

Oracle is down 39.8% from September 11th highs and brought down the sector with it.

Here's why:

The sell-off was not merely a reaction to marginal revenue miss, but both an algorithmic short and investor selloff on the sustainability of the AI capex cycle and the creditworthiness of the sector's primary tenant:

OpenAI.

Oracle's announcement of a $15 billion increase in 2026 capital spending to nearly $50 billion was inextricably linked to a reported $300 billion partnership with OpenAI.

Originally, OpenAI was the frontier LLM, with promising capex promises to Oracle, Coreweave and others, contributing to the initial repricing of the sector.

However, with over $1t+ in obligations and increasing competition from Anthropic, Gemini, XAI, and others, the markets have serious doubts on whether Oracle, Coreweave, and others are building for a tenant that cannot currently fund its obligations from operating cash flow.

WE're seeing the market effectively signaling that the market Oracle is creating an unsustainable debt-funded "vendor financing" for OpenAI, which cannot fulfill its promises.

So, the drop was rational: The sell-off was driven by a rational repricing of credit risk and capital intensity.

OpenAI Funding Fear is Valid: The hypothesis that OpenAI lacks the funds to honor its contracts is supported by a glaring mismatch between its revenue ($13B) and its obligations ($60B/year).

Credit Fears are Real: The widening of Oracle's CDS spreads sees a rising probability of a "credit event" downgrade or default.

Furthermore, we're seeing this trigger a contagion effect across the "Neocloud" sector from $NBIS dropping from $140 to $90s, $IREN dropping $80 to $40s, $CIFR dropping from $24s to $17s.

But is this a buying opportunity for Neoclouds like $WULF, $NBIS, $IREN, and others?

Yes.

Is this a good buying opportunity for $ORCL?

No.

Forward Outlook:

$ORCL (large portion) , $CRWV (25% backlog) are the two players largely dependent on OpenAI and this narrative can flip in an instant (+30%+ change) depending on capital raising activity from OpenAI.

If OpenAI files for an oversubscribed IPO in 2026 at high valuations and it's new GPT models beats out Gemini/Claude, we can see this change.

However, many other players are isolated from OpenAI. The original thesis of the Neocloud sector was Mag7 capex funndel from their cash cows segments (Azure, AWS, GCP) down into: $NBIS, $IREN, $CIFR, $WULF, and others.

But as the largest players ( $ORCL, $CRWV) fall, these algorithmically bring down the whole sector.

If you look at the companies individually, companies like $CIFR and $WULF are being backstopped by $GOOGL, and $IREN / $NBIS are funded by $MSFT.

These are locked in contract backlogs from Hyperscalers/Mag7, not OpenAI.

This irrational selloff due to misunderstanding of risks presents an amazing buying opportunity for the Necoloud sector, but not companies tied to OpenAI like $ORCL and $CRWV.

Serenity@aleabitoreddit

Post-Fed Interest Rate 25BPS cut. December 11th ratings: Strong Buy: $CRCL $COIN $AMKR $CRDO $IBIT $MSTR $AMZN $SMCI $TSM $TSSI Sk Hynix $SNAP Samsung Electronics $ALAB $META $NBIS $CIFR Buy: $KRUS $AVGO $NFLX $KRKNF $HIMS $FLY $OSS $TE $FLNC $LITE $COHR $RKLB $TTD $NVDA $CLS $GOOGL $RDDT $WULF $CRWV $IREN $GLXY $WLAC $MPWR Avoid $RGTI $PLTR $WMT $ETH $BMNR $TSLA $IONQ $ORCL $SLNH $OKLO Explanations: Today fed cut interest rates 25BPS as expected. This usually funnel liquidity into growth stocks and benefits small-medium caps that use debt the most (refinance with lower interest rates), such as Neoclouds like $NBIS and $CIFR. However, this coincides with Japan hiking, which might lead to carry trade unwind from last year's reload; but this is short term, fundamentals > volatility short term. Strong Buy Ratings: Circle - Massive drop mainly due to share unlock post IPO. However, rate cuts hurt their business model ~20% revenue cut from interest. That being said, we're seeing a massive growth in the stablecoin market, and I'm personally seeing huge early venture capital funding (a16z, sequioa, etc). being poured into stablecoin related companies such as Neobanks. We should see all of this funnel into more USDC printing, and the printer outweigh rate cuts. Coinbase - Same as Circle, they have 50% revenue sharing in terms of USDC. However, they also have their exchange on top, and rate cuts generally help riskier assets such as crypto (especially post drop Bitcoin sub 90k) Amkor - Benefits from Made in America shift to semis/fab. Credo - Dropped -16% last 5 days, and 8% today. Great recovery buy, don't see connectivity demand dropping from DC buildout. ALAB - Same thesis as CRDO IBIT (Bitcoin) - Always a great long, especially so at $93K Microstrategy (MSTR) - Benefits from Bitcoin recovery and did an analysis whether they would get liquidated or not. TLDR: no, we have another bitcoin halving event before they need to pay off interest, which was around 2029. Amazon - Hasn't moved an inch all year. Fundamentals improving, EOY helps E-commerce division. Custom chips, constellations, robotaxis, they're basically doing everything and market hasn't really rewarded their effort yet. Just a feeling we might see this outperform next 2 months. SMCI - Did a thesis post on this earlier, amazing recovery buy. It dropped on earnings due to shifting revenue backlog to next quarter, but markets aren't pricing in the fact they're growing 60% Y/Y forward revenue but trading at ~11 forward p/e or so. TSM - Backbone of the whole AI/semi buildout. We're seeing arguments about TPU vs. GPU, but TSM doesn't care. TSSI - Same thesis with SMCI, piggybacks off of Dell, just as a proxy we're seeing massive backlog from vendors such as IREN, and other neoclouds building out DCs 2026, and we should see this come into fruition next year. Sk Hynix - Apparently there's been rumors about uplisting to US markets, which should be a boost to liquidity. Also memory markets is just incredibly high demand from AI buildout. Snapchat - Just undervalued. $13B marketcap, ~1B+ quarterly revenue. NA DAU dropped 3% from last quarter but don't buy this for being the next FB. All they need to do is cut GCP costs and monetize memories (which they did) and we should see this re-rate 100%+ next year, especially with $400m+ in added revenue/equity from the Perplixty deal Samsung Electronics - People think of this as memory as well because it makes up a large part of their profit, but i see this as a potential next cash cow foundry play like TSM, as the 2nd largest player to soak up any max capacity overflow. META - One time tax selloff, was oversold. Now we finally see them create a frontier model (Avacado) if i remember correctly. So they can monetize the llama open source llm efforts they've been just blowing money on. They also cut their metaverse efforts, which should be a huge boost in proftiability. Nebius - Short term drag due to 25m share dilution. ATM is likely being offered. That being said once this finishes, insanely undervalued due to forward revenue/growth from both its DC business (7-9B ARR), and its 4 subsidaries that the markets dont price in (growing 100%+ Y/Y) CIFR - Short term drop due to Bitcoin prices (holding a lot on balance sheet), but not really affected by GPU depreciation arguments since they do colo models. Also backstopped by google, and they have contracts with Amazon, so fundamentally disrisked and one of the top buys in neocloud secotr. Buy Ratings: Running out of text space so will give a shorter TLDR Kura Sushi - Swing trade zoom out 5 year chart and you'll see what I mean every time it bottoms (around now). This never fails! Broadcom - Hyperscaler buildout, critical to TPU alongside Mediatek Netflix - 16% drop feels a bit unwarranted for the acquisition KRKNF - Great growing fundamentals and defensible market as an andruil supplier. HIMS - Share buyback program, usually sub $40 great buy/swing trade. Zava acqusition not being priced in and it's still growing. FLY - SpaceX $1.5T valuation should boost up the whole space sector. This was a 2026 play for medium lift. OSS - DD on this earlier potential andruil supplier. Otherwise, kind of undervalued at this MC anyway. TE - One of the few Murican energy infra, Solar. It's likely more commercial than Nuclear. FLNC - Same thesis with AI buildout + energy LITE - Pretty overextended right now, wouldn't chase. But long term benefits from being in the middle of both tpu ironwood + blackwell buildout COHR - Same with Lite, but seems like a secondary player. RKLB - Probably my favorite long. Pretty overvalued right now but can't help it due to SpaceX fomo. TTD - Thesis post earlier, just based on forward revenue numbers, it seems like a great recovery play. NVDA - TPU fears are a bit overblown, just look at backlog. CLS - TPU v7 ecosystem buy GOOGL - They sell TPUs like NVDA, growing robotoaxis market like waymo, gemini succesful. Just firing on all fronts. Reddit - Just a money printer like early day Robinhood. Made some thesis comments about RDDT growing in terms of acquisitions from FCF. Otherwise, they're here to stay and benefits from all gens using it (unlike snap which is earlier) WULF - Similar to CIFR. Rerating might happen depending on more info about the Anthropic buildout. CRWV - Terrible, terrible long. Good short term recovery buy. IREN - I would not put money into this if they kept buying GPUs to do AI cloud just due to dilution. but they might do colo and they have an immense amount of GW capacity so it's still promising. GLXY - Beneficary of DC Buildout. WLAC - Possible that they're SPAC ipoing this month. They did say Q4. MPWR - TPU v7 ecosystem buy Avoid RGTI - Quantum, no fundamentals/revenue to back it up PLTR - 449.01B market cap lol WMT - They're growing like 4% revenue a year, but trading at 40 p/e which is insane. ETH - Ethereum great network. However, there's no token burn and none of the revenue goes to token holders. Terrible investment, great developer tooling/ecosystem. BMNR - Ethereum proxy. TSLA - Kind of detached from fundamentals. But it's a bet on elon musk, robotaxis at scale, robotics. I personally just see this as overpromising, but we'll see. IONQ -Quantum, no fundamentals/revenue to back it up ORCL - Most of forward backlog is dependent on openai, which makes things incredibly uncertain/risky if openai falls to claude/gemini in market share. That being said, it's a good recovery buy right now, but long term it's risky. SLNH - This is the stock to be in if you want diluted to oblivion on their 2.8gw pipeline. OKLO - no fundamentals like quantum to back up mc at this moment, this likely years out to come into fruition.

English

#Commanders DL Daron Payne has been suspended 1 game for an act of unsportsmanlike conduct against the #Lions.

Payne was disqualified for punching Amon-Ra St. Brown.

English