DROCK STOCKS

6K posts

DROCK STOCKS

@DRockStocks

Learning everyday and stacking wins. Current portfolio concentration: $MSFT, $RKLB, $NBIS, $UNH, $TE, $NOW (small)

Katılım Mayıs 2021

316 Takip Edilen424 Takipçiler

@birdabo One step closer to the scam of real estate agent fees going away

English

florida man sold his house in 5 days using chatgpt without real estate agents

> asked AI for pricing.

> marketing.

> best listing day

> contract drafting.

bro easily got 5 offers in 72 hours.

- also saved 3% commission.

real estate agents are cooked 😭😭😭

Dexerto@Dexerto

Florida man sold his house in just 5 days after letting ChatGPT handle the entire process instead of a real estate agent The AI handled pricing, marketing, showings, and even helped draft the contract

English

I am tired of being Arizona’s Super Bowl. This is the one game a year they always have circled on the calendar. While we're focused on winning Big 12 championships, they are only focused on beating us. It's time to #nuke the school

English

English

@NotA_Bull Bought mine for $800K in 20’s and sold for $1.2M, 5 years later. Great investment.

English

Buying a house in your 20s is a liability, not an investment.

Argue against me.

English

English

English

Breaking: Caleb Holt, the No. 4 ranked player in the SC Next 100 for the Class of 2026, has committed to Arizona, he announced on @FirstTake.

English

Anyone besides me think this might be a good time to start shorting Oil? ...

English

DROCK STOCKS retweetledi

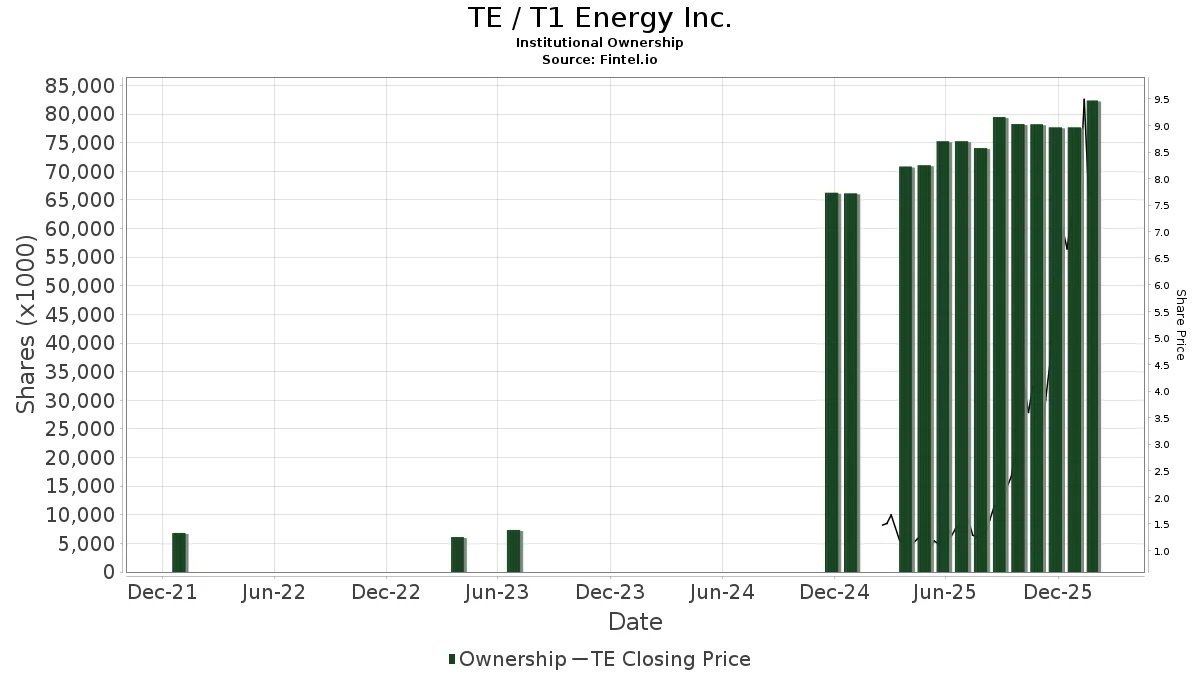

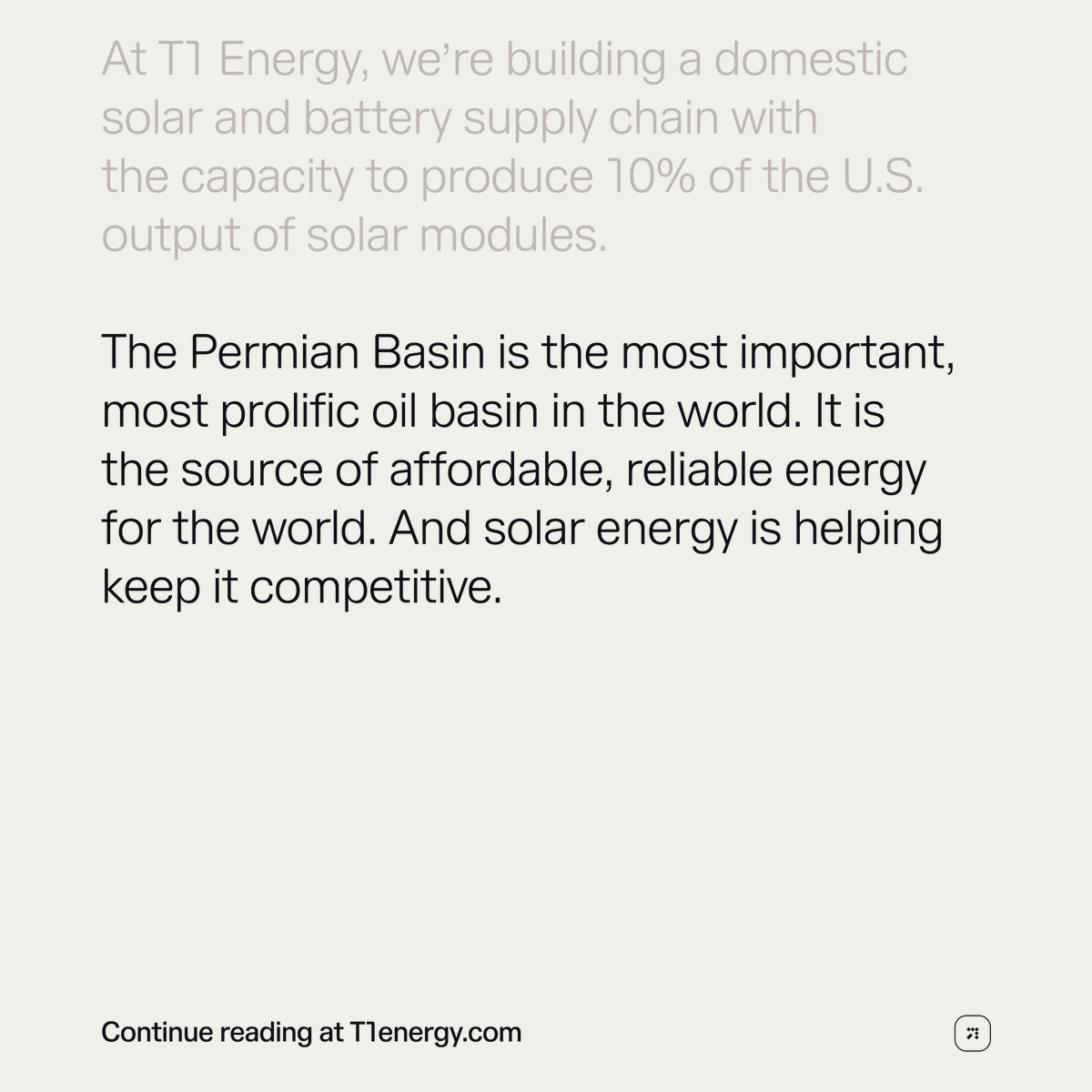

$TE is one of my highest conviction stocks in 2026

WHAT THE MARKET THINKS:

The market is pricing T1 Energy as a cyclical, capital-intensive solar assembler. But this narrative is outdated

TE is building a vertically integrated US solar supply chain at a time when domestic sourcing is a strategic priority

The CORE MOAT:

TE isn’t just making modules, it’s systematically owning manufacturing from cells to finished product in the US

G1 Dallas (solar modules) is scaling production ahead of plan

G2 Austin (solar cell fabrication) is under construction with Phase 1 targeted for Q4 2026 production

This creates a domestic moat rare in solar: control over both cell and module supply in a region prioritizing local energy security

Competitors are either offshore or still vertically fragmented

THIS ISN’T JUST “SOLAR”:

PEERS TRADE AS: commodity panel makers with low pricing power and margin compression

TE IS BECOMING:

• A US strategic supplier amid geopolitical manufacturing reshoring.

• A company capturing higher-value content (cells + modules + batteries) with fewer links in the supply chain to third parties

This transforms valuation logic, not mere watts shipped but earnings from owned capacity with pricing discipline

INFLECTION: GUIDANCE + SCALE:

Recent results showed a meaningful ramp in module output with revenue over $200M in Q3 2025, signaling demand conversion and manufacturing scale

HOWEVER, Q4 revenue is guided to be larger than Q1, Q2 and Q3 together, with a yearly run-rate of 4.5GW

Importantly, G2 Austin is slated to start construction in Q4 2025, with first production Q4 2026, giving TE a major margin inflection in 2027 once cell output feeds into higher-margin finished goods

FEOC COMPLIANCE

According to recent reports by TE, their recent structural changes align with FEOC guidance

Changes:

• Reduced debt exposure to Trina Solar

• Capped foreign ownership

• Removed governance control

• Restructured technology licensing (IP)

• Shifted the supply chain away from FEOC sources (not finished)

This is crucial since it would allow TE to remain eligible for the 45X credits which provide per-unit incentives for US solar components

This would unlock true operating leverage

CURRENT VALUATION:

TE trades at only 4.5 P/S:

If they execute in Q4 → PS < 2.2

If they maintain run-rate in 2026 (without G2 Austin) → PS < 1.1

The market is still behind the expected growth, not to mention the real manufacturing scale or future integrated margins

ASYMMETRY: UPSIDE vs DOWNSIDE

What goes right:

• G2 Austin online → integrated cell + module margins triple worth over commodity modules

• US policy increasingly favors domestic content → pricing power and reduced import competition

• Higher capacity utilization drives operating leverage

What goes wrong:

• Execution timelines slip, but TE has already met targets at G1 Dallas

• Policy shifts reduce subsidy certainty, manageable because global solar adoption continues growing

Downside is survivable: TE has begun revenue scaling, is funded through construction, and already produces modules

Upside is non-linear: integrated domestic capacity is rare and strategic

TIME CATALYSTS:

• Q4 2025: G1 Dallas sharp activation and G2 Austin construction start

• Q4 2026: anticipated production from G2 Austin

• 2027: potential margin inflection as integrated output rises

BOTTOM LINE:

$TE is not a solar panel assembler, it’s building a vertically integrated US solar manufacturing platform, anchored with G1 Dallas and the coming G2 Austin cell fab

Domestic content + integrated output = pricing power, structural growth, and margin leverage

The market is still pricing their revenue inflection, not yet thinking of their vertical integration

NOTE: Not Financial Advice. DYOR

#TE #Stocks

English

DROCK STOCKS retweetledi

What’s one stock you’d be comfortable putting 30% of your portfolio into

English

@SarAEsQMd @jrouldz Yes buy high sell low has always been a good strategy

English

Gonna go ahead and get off the screens my friends 😂😂😂

I’ll check back with yall later will try to find some grass in Manhattan I can touch 😆

English

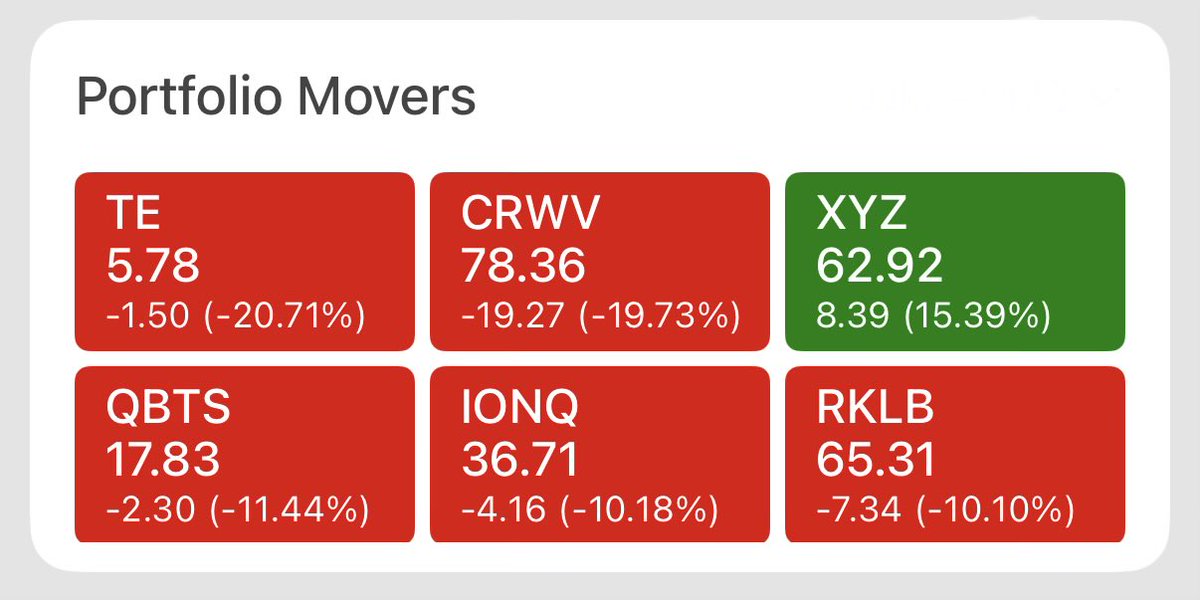

$TE

Morgan Lyons@morgan_tigers

Uhhh... this is quite a tone shift from the Trump admin 👀 "Interior indicated in its statement that it considers solar part of the admin’s ongoing efforts to ramp up domestic energy production, which is needed to power energy-intensive data centers..." subscriber.politicopro.com/article/eenews…

QCT

Adding $TE heavy here, building this into on of the main portfolio positions

English