DaDao大道 retweetledi

I wasn’t planning to share this, but it’s such a high-quality explanation of CPO that I have to.

Just watch it. You’ll regret it if you don’t.

youtu.be/wiH6d4m9o4o?si…

YouTube

English

DaDao大道

99 posts

@DaDaoCapital

50% vibe trading | 50% research | 1000% memes & shit post Not Financial Advice

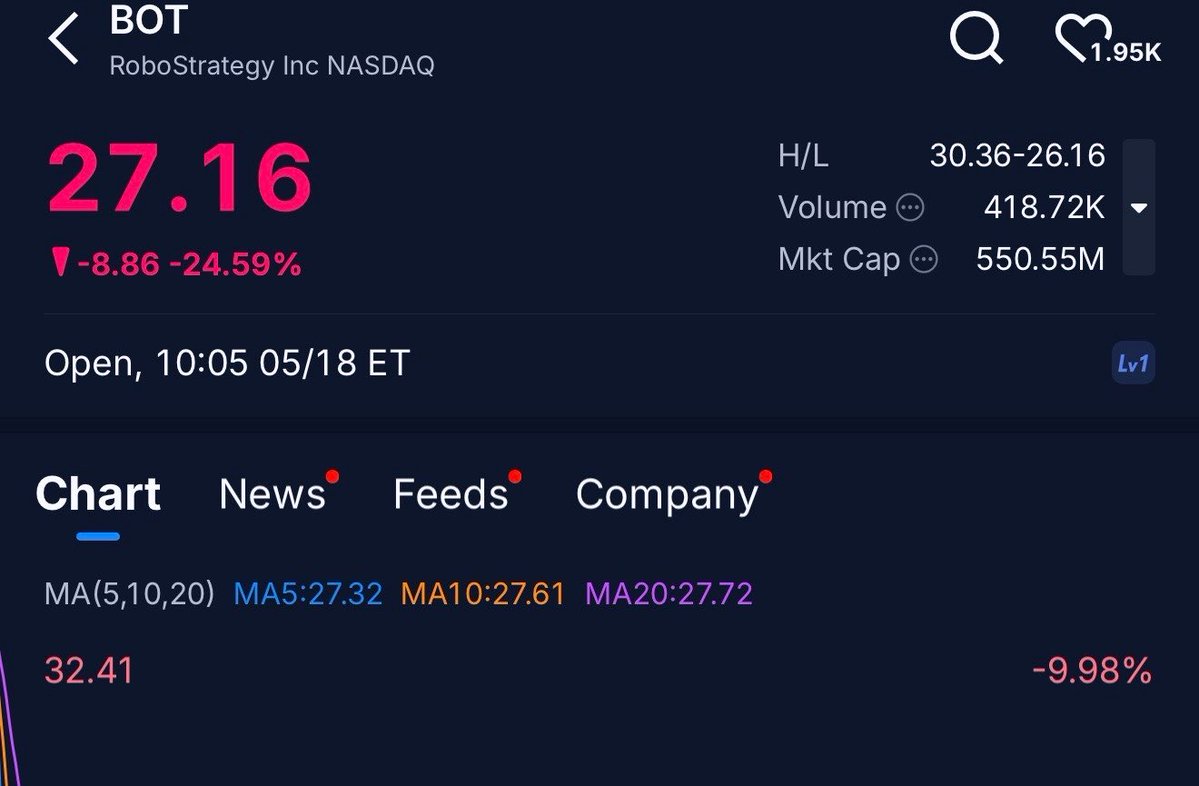

META would be more attractive at $800 with a more diversified revenue model (not just ads) and a demonstrative ROI on their capex. It’s one of those stocks you are better off chasing up 10-15 pct once you feel like both of these are happening. “Cheap” with no catalyst doesn’t seem to be working in this tape. If you have duration and are looking out 5 plus years you are probably fine x.com/dividendology/…

.@danshipper: "I would buy SaaS stocks right now. SaaS stocks will be up majorly in the next couple of years."

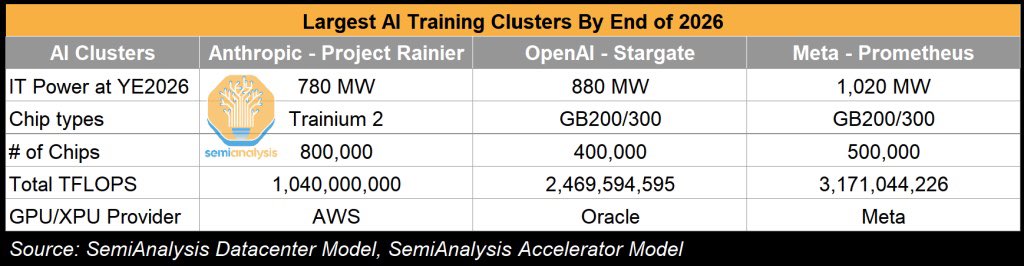

Kevin Xu on ChatGPT this week