@leduke188 @Taylor_GPT @aleabitoreddit Doing both already. No I'm not getting over it. Doing that is what causes Americans to lose all of their benefits to begin with.

English

Silver Hawks

200 posts

I'm long $TSEM, the $TSM of photonics. My top two picks for CPO are $SOI and Tower Semi. Given the $NVDA GTC catalyst on new photonic related architecture next week: I expect Tower Semi to get a huge catalyst. Nvidia laready directly collaborated with Tower to scale 1.6T silicon photonics last month (hint hint for GTC), likely pushing the downstream players to use it. And now, Tower is the leading supplier of 1.6T SiPh PICs and the primary foundry for scale-up CPO architectures. (the other being global foundries) From my forward est: 2028 Forward P/E: ~16.8x to ~18.1x (Tower set a target $2.84B revenue by 2028, with ~31.7% operating margin, ~$750M in net profit) The thing to note is over 70% of their planned SiPh capacity is already reserved through 2028. And photonics haven't even ramped up yet. So, I expect them to strongly beat earning projections due to extreme photonics scaling + allocations price hikes that's not modeled into projections. Also, $TSEM is heavily de-risked by 70% of capacity already being reserved. MC is likely due to $TSEM being a very obscure upstream player in the photonics supply chain. But I expect the $NVDA GTC conference to be that catalyst that brings it to premium valuations. I'm long $TSEM as an asymmetrical upside for upstream photonics foundry layer.

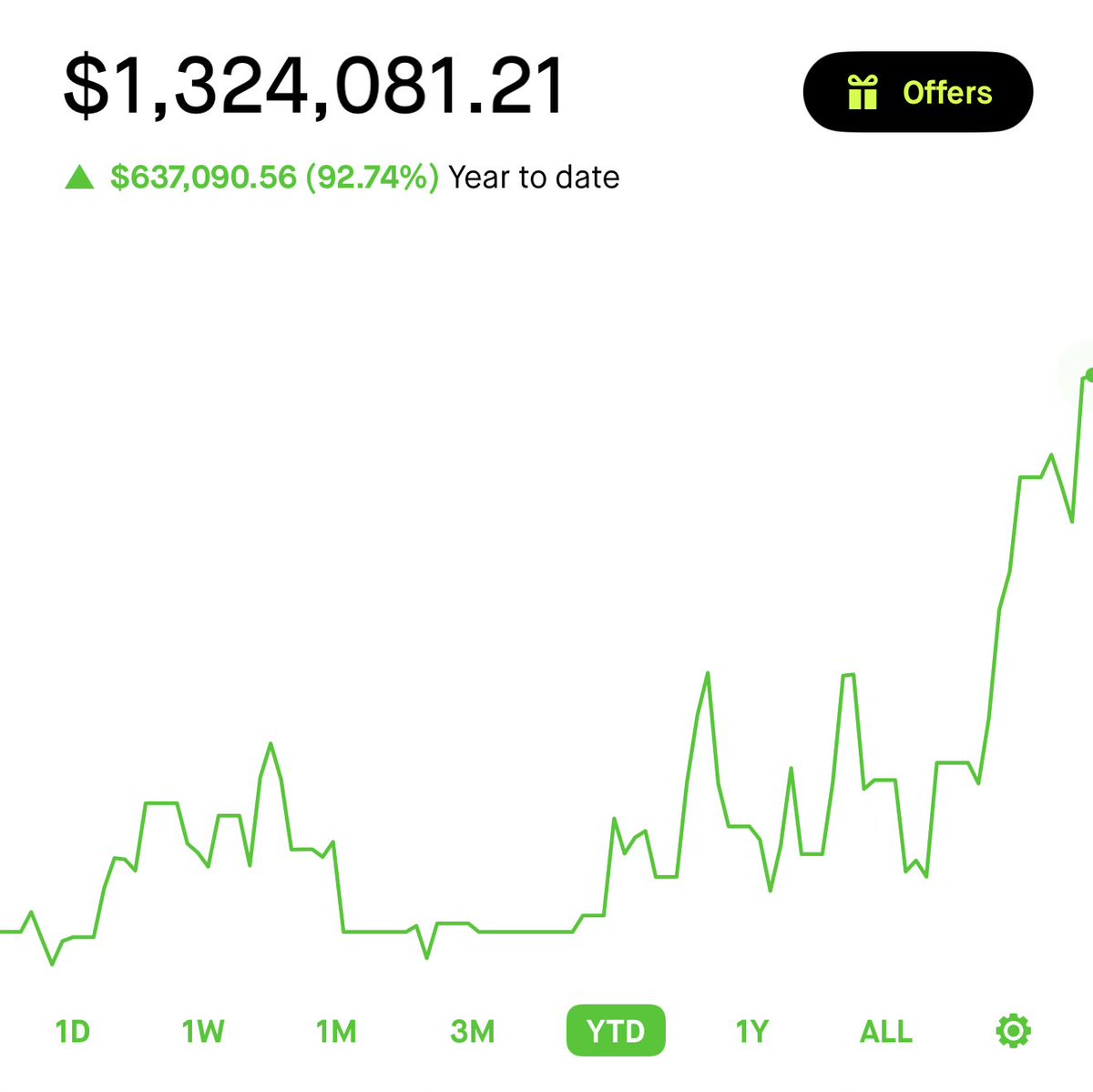

@aleabitoreddit I basically skipped over the March Iran-war market drop while staying heavily exposed to stocks, and still ended up gaining thanks to your picks. Portfolio is up 3x YTD and I’m just some random retail guy from Canada, so I can only imagine how many others you’ve helped. Thank you

@aleabitoreddit I feel like you're one of those heroes in anime leveling up and now you're aura farming 😄

I'm not sure people understand yet: $LITE backlog order fill into 2028 signals extreme demand. And a lack of capacity. Then by second order effect of hyperscaler demand spillover: Guess who is projected to have the largest 800G/1.6T capacity in America? $AAOI. They fab their own inp lasers, design their own transceivers, and assemble it. If $AAOI can execute on capacity ramp, that likely all translates into revenue due to everything being sold out. My $40B MC price target from $5B is starting to look more and more likely?

Was the first to talk about $AXTI in relation to photonics BOM/supply chains: $IQE is very interesting too as one of the only Western suppliers. Basically if you look at photonics flow on $GOOGL TPU/hyperscaler ASICs kinda looks like this (very likely, but undisclosed): Optical Transceivers (highest BOM): Lumentum/Cloud Light: ~ Vital / $AXTI-> $AXTI/Sumitomo/JX -> $IQE (Epi-Wafers) -> $LITE / Cloud Light -> $FN (Contract Manufacturing) -> $GOOGL TPU Merhcant optical supply chain: ~ Vital / $AXTI -> $AXTI / Sumitomo / JX -> → $LITE / $AVGO / $COHR (EML) + $MRVL / $MTSI / Semtech -> Innolight/Eoptolink -> $GOOGL So if you want moonshot-type photonics BOM / price-hikes stocks deeper upstream in the photonics BOM: $AXTI, $IQE and your way to go. $AXTI had terrible fundamentals before but the recent Northland fundraising round cemented its run. $IQE has terrible fundamentals now (Net debt £23.5 million) but is probably one of the most critical parts of the supply chain. If they manage to sell their Taiwan operations, wouldn't be surprised if it went up quite a bit just from their inp business. There's £18m convertible notes (which is basically nothing), then there's 120 to 154m new shares (~12% to 15%), which is also kinda nothing relative to current size. On the other hand, others $LITE and Innolight are probably more established. TLDR: $IQE -> seems critical to Western supply chains, $130MC. Net debt, if they sell Taiwan business -> strong re-rating or they might just dilute you anyway. But if the Taiwan business fails to be sold, probably expect to be diluted to oblivion like Wolfspeed. So huge, huge, risk ad do you own research into risks. But $AXTI and $IQE might are personally interesting to me (I do own $IQE).