David Marr

142 posts

We had an incredibly productive board meeting today at Fannie Mae - our best one yet! The team is energized and laser focused on AI, Operational Efficiency, and ROE with our main goal of restoring the American Dream of Home Ownership!!! Great job to the ENTIRE Fannie Mae Team!!!

English

@DavidEricMarr Here are the next levels I believe we will continue to retrace into this first area on both #FNMA and #FMCC first to this retracement level, and then if it breaks below which I believe it may sweep all the liquidity down to here. Two major sweeps this month 2$-3$ range

English

@PamDanziger @Forbes This is an example of poor research and reporting. You did not even reach out to Marcus.

English

Can Bed Bath & Beyond turn its vision of an "Everything Home" ecosystem into coherent business model? I try to unpack it in my latest Forbes.com article. Inside Bed Bath & Beyond’s Grand Vision For An ‘Everything Home’ Ecosystem via @forbes forbes.com/sites/pamdanzi…

English

@pratjoey @TheKnewHuman Yes it is for all of us. But I think it will be a 1 rather than a 0.

English

@TheKnewHuman @DavidEricMarr For sure man. The OTC shenanigans are the stuff of legend. This is a binary trade for me.

English

@TheKnewHuman @DavidEricMarr Nah

Just broke out of an 8 month channel with volume and now retesting 200 day

NY Fed is in comment period on effects of ownership change for GSEs

English

@DavidEricMarr There was no significant volume above those levels..that low volume today was not enough for continuation it needs to hold above those levels 7.13 is the most critical level on the chart for #FMCC amd #FNMa my thesis is still valid on retracement unless major news. 🗞️ will update

English

$Rily

Another 20million gains just from the increase in BW. It’s like holding a beach ball under water. Some time this will rise.

English

@leevalueroach Congratulations Lee! I almost pulled the trigger on this one.

English

@PerseusBC @ParrotCapital The trend in in industry will not be your friend. Company’s are spending Billions in Capex spending.

English

Is @ParrotCapital still short $BW ?🔥🩳🔥🚀

$rily $mpt 💎💎🍿🍿

Parrot Capital 🦜@ParrotCapital

@77AugustWest72 I'm short $BW. Dan's thesis at @WolfpackReports is solid IMHO, plus the macro economy is still on the brink thanks to the Iran War. Now isn't exactly the environment favorable to sketchy $RILY portfolio companies.

English

English

@ericjackson @EMJCapital $RILY..check it out... $CVNA type move coming!!..."Tuesday" is the "GameDay"

English

Over the last month, my X impressions have exploded talking about $BTQQF $IREN and $CIFR because everyone is looking for the next $CVNA.

We think we just found another.

@EMJCapital has taken a position in $OPEN — and we believe it could be a 100-bagger over the next few years. Here’s why 🧵

English

English

@baltostar @AlderLaneEggs The B Riley $RILY portfolio companies like $BW, $APLD, and others have lots of clueless retail traders (shilling rats) organized on social media to promote their worthless shares.

If the SEC were functioning correctly, they'd look into the ringleaders of these stock promotions.

English

One of my most trusted sources has informed me that this rodent farm equipment supplier is where the $RILY and $BW rats are bred, before they're shipped off to StockTwits, Reddit, and Twitter to shill Bryant Riley's horrific portfolio companies.

English

@JohnDee78791547 The big news about this is not so much the message, as the messenger!

$FNMA, $FMCC, $FNMAS

English

It’s not too late to lock them all up $FNMA $FMCC $FNMAS $FMCKJ

Robert Bowes@Robert_B_Bowes

To compliment the @BillAckman accurate description of the Net Worth Sweep of 100% of Fannie and Freddie profits, one must also look at how the Obama Treasury forced F2 to cook their books. Then Treasury Secretary Tim Geithner continued the Hank Paulson large bailout plan that exacerbated the mortgage market crisis and extended credit losses beyond the sand States. Geithner hired both Blackrock and Blackstone to direct F2 to find as many write downs as they could to justify the $100B each bailout that protected F2 bondholders. When F2 internal models were stressed they each could not come close to $100B in losses. Paulson and Geithner wrongly compared street private label mortgage losses to the relatively safer book of GSE mortgages failing to recognize that GSEs had strong first loss cover in private mortgage insurance and in bank legal obligations to repurchase fraudulent and defectively underwritten mortgages. Obama Treasury forced F2 to cook their books and zero out all PMI ($43B of trapped liquid claims paying ability) and all lender recourse (another $61B of liquid bank assets - $20B alone with BofA) that provided F2 legally obligated claims paying ability. Treasury ignored that first loss liquidity forcing F2 to post large credit provisions in 2008-2010. The policy was extend and pretend for the banks and PMIs but to force F2 into conservatorship. Yet the PMI and recourse funds were being collected while bad loan repurchases mushroomed. F2 also tightened the credit box and doubled GFees during this period. It was a total double standard to target F2 investors. In hindsight F2 never needed the bailouts for cash flow because the credit loss provisions and other valuation allowances were non-cash. The bailouts were optics done for mostly foreign bondholders. American homeowners and F2 shareholders were the victims of that failure. Then with the high non cash credit losses F2 each wrote off $31B and and $21B of Deferred Tax Assets in 2008 respectively. In 2009-2011 another $29B Fannie and $8B Freddie DTA write downs for a total of $89B. Combining the $104B non-cash credit losses with the $89B DTA write downs coincidentally equalled the amount of Treasury F2 bailout in Senior Preferred. Yet in 2010 and 2011 F2 were collecting the PMI, lender recourse, the higher GFees and trends started to look good for home price recovery. Treasury knew ahead of the NWS taking that F2 would be rolling in profits. Nonetheless F2 kept loan loss allowances high and gave no model value to the liquid PMI first loss claim receipts. They all knew ahead of 2012 that the DTAs and loan loss provisions would appear anomalous. Facing obvious valuation allowance reversals, Treasury rushed to implement the 2012 NWS. Smart folks inside witnessed the accounting and loan loss committee gimmickry - with some still working at F2.

English

David Marr retweetledi

A number of press reports have characterized our and other shareholders’ efforts on behalf of Fannie and Freddie (F2) as seeking a ‘gift’ or ‘handout’ from the government. We, the shareholders of F2, seek no such thing.

Hundreds of financial institutions were bailed out during the GFC by the U.S. Treasury. Nearly all of the financial institution bailouts during the GFC involved an injection of capital in the form of senior preferred stock by Treasury at an interest rate of 5%, plus warrants to acquire common stock in an amount equal to 15% of the face amount of the preferred with an exercise price at the then-current stock price of the rescued institution.

For example, Treasury’s preferred stock investment in Goldman Sachs was in an amount of $10 billion and, in addition, Treasury received warrants on $1.5 billion of GS' common stock at its then market price.

The bailout terms for F2 were materially more burdensome and expensive, with a higher interest rate and substantially more warrant coverage, than that of every other financial institution (other than those of AIG whose terms were similar). Despite the F2 bailouts’ massively more burdensome terms, shareholders are not complaining about the original terms.

Treasury invested $193 billion in F2 in the form of senior preferred stock (SPS), including funding for $2 billion of commitment fees, with a 10% coupon (twice that of the banks). Treasury also received warrants on 79.9% of both companies’ outstanding shares.

Fannie and Freddie have since repaid Treasury $301 billion, which includes interest on the SPS at a blended rate of 11.6%, an interest rate which is 160 basis points more per annum, and have returned the entire $193 billion of outstanding principal, $25 billion in excess of what was contractually owed. In summary, the F2 SPS has been fully repaid according to its original contractual terms plus an extra $25 billion.

Despite the fact that the SPS has been more than repaid in full, Fannie and Freddie have not accounted for these payments on their respective balance sheets, and the $193 billion of SPS remains an outstanding liability as if no principal payments had ever been made.

How can it be, you might ask, if indeed F2 have repaid $301 billion to Treasury when only $276 billion was due could there be any remaining balance of the SPS on the F2 balance sheets?

The answer relates to something called the ‘Net Worth Sweep (NWS).’

During the second term of the Obama administration, on August 12, 2012, two quarters after F2 returned to profitability, Treasury announced that it was unilaterally amending the terms of the SPS stock to provide that Treasury would take 100% of the profits of F2 each quarter in lieu of the 10% annual dividend rate. This was not a negotiated resolution with F2. It was a unilateral amendment of the original terms of the SPS that was done in bad faith.

The supposed rationale for the amended terms of the SPS was akin to the IRS garnishing the wages of someone who will never be able to pay the taxes that they owe. That is, the Treasury said F2 will never be able to pay the 10% coupon, let alone the SPS’ $193 billion principal balance, so it decided instead to ‘settle’ for 100% of F2’s profits forever.

In discovery, shareholders learned that the stated justification for the amendment was false. In mid 2012, the Obama administration had come to learn that both companies would soon be reversing tens of billions of reserves on their balance sheets as housing values had increased and the reserves taken during the GFC had been excessive. The NWS was instituted by Obama to forestall F2 from forever being able to recapitalize and be released from conservatorship. The NWS was not a ‘settlement’ for a lesser amount of future payments. It was the outright theft of the forever profits of both companies.

Never before or since has the government ‘swept’ 100% of the profits of any company, let alone a financial institution in conservatorship, a form of government intervention where the goal is rehabilitation of the institution, and where the hierarchy of corporate claims has always been respected.

The accounting for the NWS payments while it was in effect (until Secretary Mnuchin terminated the NWS in Trump’s first term) was also unusual. The NWS was treated by F2 as a quarterly adjustment to the dividend rate on the SPS such that the dividend amount owed was made equal to the after-tax profits of F2 for that quarter with no limitation.

In other words, regardless of the amount of profit F2 generated for the quarter – whether or not it was in excess of the original 10% annual dividend – the dividend payable under the NWS was made equal to the quarterly profit. The absurd terms of the NWS sweep therefore made it impossible for any partial or full repayment of the SPS to take place as every dollar paid to the Treasury on the amended terms of the SPS was considered a dividend payment, even if the amount was massively in excess of the original contractual SPS terms.

The absurdity of the NWS was made clear just two quarters after the NWS went into effect. Fannie Mae generated a profit of $59 billion in the first quarter of 2013, and the SPS dividend rate for that quarter was set at $59 billion so the entire amount was swept to the government, more than 10 times the contractual dividend rate.

I had the opportunity to discuss F2 and the NWS with Warren Buffett about a decade ago and he said that he “couldn’t believe what the government had done.”

In short, the shareholders of F2 are simply asking the government to respect the original and highly burdensome terms of the SPS. There is no dispute that Treasury has received more than the original 10% coupon and full repayment of principal of the SPS, that is, an extra $25 billion.

We and the millions of other shareholders of F2 are simply asking the administration to honor the original SPS terms and properly account for the $301 billion of payments, thereby eliminating the SPS liability from both companies’ balance sheets.

Shareholders have not asked for the extra $25 billion to be returned to the two companies. Treasury can decide whether to keep those funds or return them to the companies.

Accounting for the repayment of the SPS has other important implications. Namely, it is critically important that conservatorships respect the rule of law, in particular, the contractual terms of corporate instruments and the hierarchy of claims. Otherwise, no financial institution that gets into trouble will be able to raise rescue capital in the private markets.

Notably, the treatment of F2 in conservatorship explains why Silicon Valley Bank and other recent large bank failures since the GFC were unable to raise private capital and avoid government intervention or a forced sale to J.P. Morgan. If the government with the stroke of a pen during conservatorship can at a whim wipe out common and preferred shareholders, no one is going to step in to try to save a financial institution that gets into trouble, and only the top few banks will be possible rescuers of big banks that fail.

Furthermore, because of F2’s history, their reputation in the capital markets has been greatly damaged. F2 raised $22 billion of preferred stock in the year or so prior to conservatorship as the government pressed both companies to raise capital. Institutions were willing to invest billions of dollars of capital into both institutions before they failed because, based on all precedent conservatorships, the contractual terms of all financial instruments and the hierarchy of claims had been preserved. Unfortunately, in light of the precedent of the net worth sweep, no investor can be confident that they won’t be wiped out in a future conservatorship so none has been willing to take the risk.

Some have proposed that Treasury simply convert the SPS into junior preferred and common stock and massively dilute shareholders. Putting aside the potential legal challenges to this approach, the result will be that Treasury will at best own something approaching 95% of both companies rather than 79.9%.

While the government’s percentage ownership stake would be larger in the SPS conversion approach, the value of the government’s larger stake would be considerably lower as the companies would become un-investable. Who would invest in F2 alongside the government when they just wiped out the previous owners?

In the SPS conversion scenario, the government’s stake, at best, if it could be sold, would trade at a massively discounted valuation, well below the value of the government's stake if Treasury retained only its contracted for 79.9% stake and respected the original terms of the SPS. In other words, a slightly smaller ownership stake of much more highly valued companies would equate to considerably more value for Treasury and taxpayers.

In a public letter to Rand Paul after his first term in November of 2021, President Trump recognized that the net worth sweep was theft from the shareholders of Fannie and Freddie. He wrote:

“Another Obama/Biden scam in legal trouble was when they allowed the Federal Housing Finance Agency (FHFA) to steal the retirement savings of hardworking Americans who had invested in Fannie Mae and Freddie Mac…The idea that the government can steal money from its citizens is socialism and is a travesty brought to you by the Obama/Biden administration. My Administration was denied the time it needed to fix this problem because of the unconstitutional restriction on firing Mel Watt. It has to come to an end and courts must protect our citizens.”

I couldn’t have said it better than President Trump.

Now that you have the time, Mr. President, let’s Stop the Steal!

English

@realsheepwolf I bought shares of CMBM last week because of their connection to Starlink.

English

"Overhang" refers to the presence of a large block of shares that are potentially waiting to be sold into the market. This creates a "ceiling" or heavy resistance because any time the stock price starts to move up, these shareholders (often institutional or debt-holders) sell their positions, absorbing the buying pressure and killing the momentum.

E.g... warrants, convertible notes, shelf registrations (S-3), SEPA (Standby Equity Purchase Agreement)

English

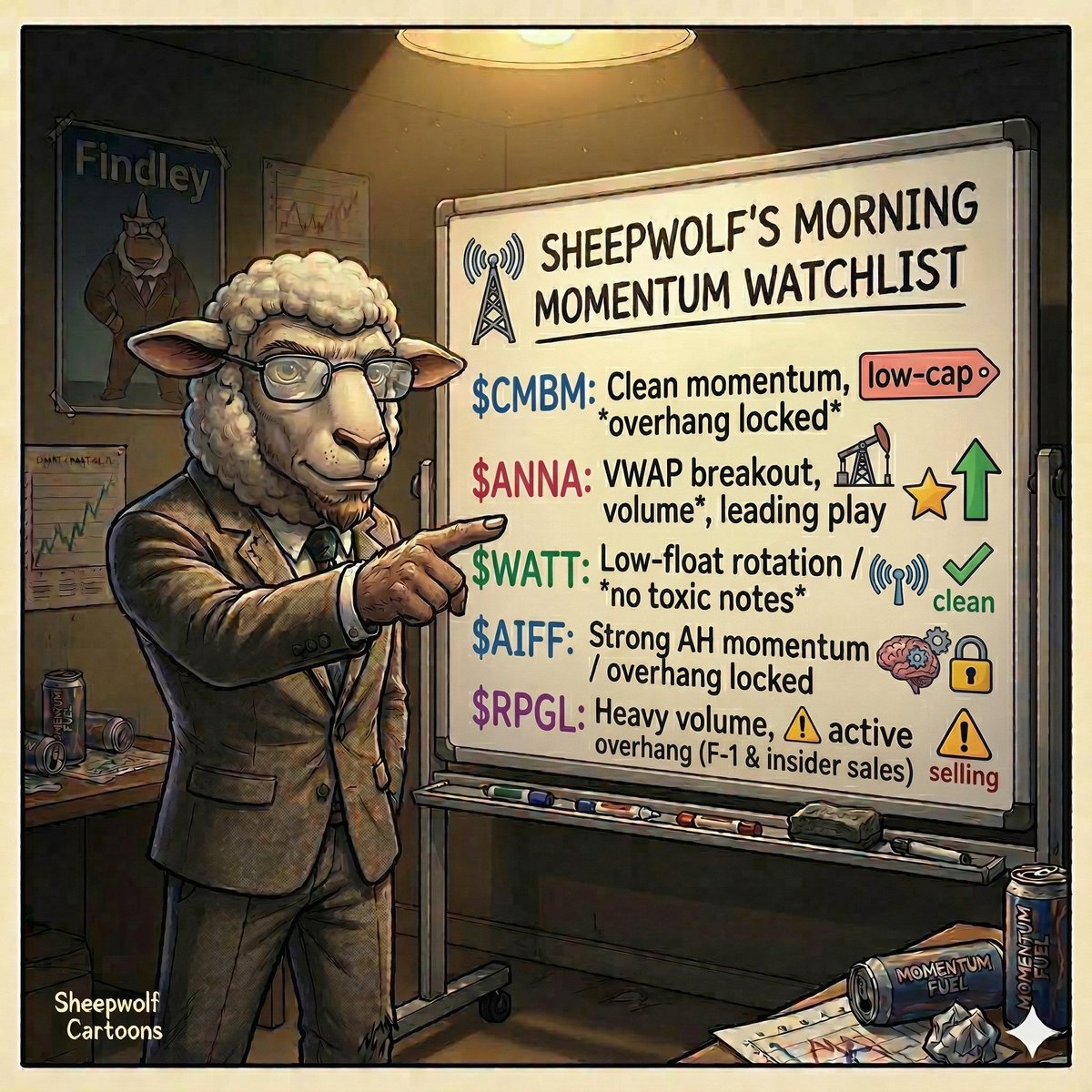

🐺 03/23 Sheepwolf Morning Momentum Watchlist

$CMBM: Clean low-cap momentum, overhang locked 🔒

$ANNA: Leading play, VWAP/Volume breakout ⭐️⬆️

$WATT: Low-float rotation, no toxic notes ✅

$AIFF: Strong AH momentum, overhang locked 🔒

$RPGL: Heavy volume, ⚠️ active overhang 🚨

English