Sabitlenmiş Tweet

JS

386 posts

JS

@DeltaandFlow

Futures, commodities, equities.

Australia. Katılım Eylül 2025

103 Takip Edilen35 Takipçiler

@formerhfpm Dean Pay & the bulldogs. Over achieved with a poor roster untill salary cap issues resolved. Then club doesn't consider him. Clubman first time coach similar Foz. Thanks Gus Gould.

English

Manly has gone with Kieran Foran as head coach because they know they can let him go at the end of the season for either Ballin, Ennis or Arthur. Set up to fail #NRL

English

If the war continues and it turns into the huge crisis some experts are projecting, Australia is going to see a dramatic surge in asylum applications as temporary visa holders look to avoid going home.

And that is to say nothing of people arriving on tourist visas and not going home.

Its time to get tough now and prepare the groundwork to deport people in large numbers, starting with the 50k+ on the list already slated to be removed and exhausted their avenues of appeal.

English

@TastesChicken @MikeBromley15 @tax_oz @goodfoodgal Well if that's the case you will now see demand reduction as demand will have solely been bought forward. In addition some price related demand reduction. I doubt you will see the issue solely as a result of demand as you inuate.

English

@MikeBromley15 @tax_oz @goodfoodgal Well according to the fuel companies and distributors, that is exactly what caused this problem, they have stated that in the early weeks of Trumps war of convenience that demand rose by 200% on the back of panic buying and hoarding. So not all government propaganda as you say

English

CONVERSATION yesterday with a friend:

Me: “this fuel crisis is a worry. It’s going faster than I predicted. It’s unbelievable we are in this predicament”.

Friend: “I don’t think about any of that stuff. I just keep my head down.”

“Oh. Ok.”

“Yeah… I don’t want to worry about any of that. ”

“Well…You may have to soon.”

You see Australia - it’s not just the politicians’ fault.

Many Aussies just don’t care.

As long as mummy & daddy government look after them.

English

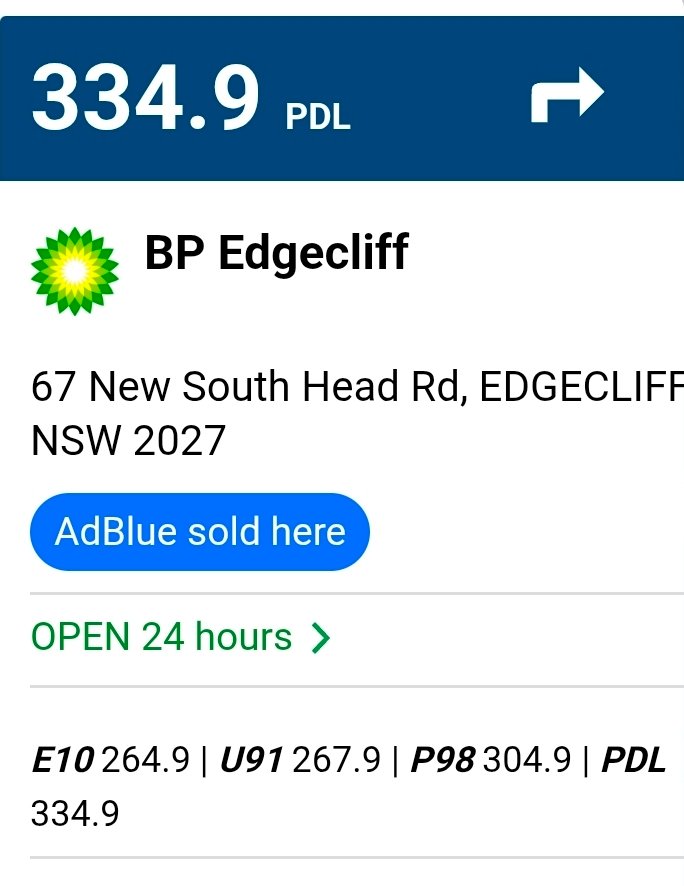

Most expensive fuel in NSW

x.com/toy59496/statu…

This suck in Edgecliff, so much for the ACCC ensuring there is no price gouging. It's a full 38c more than the other fellow below. In fact I'm going to walk down there and tell them off...

In fact I should tell those politicians off as well given the combination of fuel excise tax and GST constitutes about 80 cents of that bill per litre. It's a windfall tax for them... But they won't tax the windfall like they do my coal....

@acccgovau @ChrisMinnsMP @AlboMP

Robin Dods@toy59496

Check your Petrol/Diesel Price Don't forget the official App that lets you check fuel in NSW fuelcheck.nsw.gov.au/app And congratulations to this guy who has the cheapest diesel in Sydney.

English

@Dale96183744121 @DavidPocock Yeh k. Was genuinely asking for figures to exhibit ROI. Even if positive ROI if cannot consider that a better or superior ROI can be obtained with tax payer funds elsewhere - then you are just DUMB. I'm open minded to either but at this point not convinced.

English

@DeltaandFlow @DavidPocock The new Perth stadium pumps huge money into the economy. Sheeran concert. Even the parramatta stadium is producing massive economic benefits with all the restaraunts in eat st near it. Look at Suncorp. Huge amounts of events. If you can’t see that you are being ignorant.

English

Bruce Stadium has served us well but is at the end of its life and needs to be replaced. We've known this for years but only have 7 feasibility studies to show for it.

Let's do it right and set ourselves up to host our much-loved local teams as well as international events for the next 50 years.

Surely a centrally located stadium close to hospitality, public transport and hotels is the best way to set us up for the future and deliver maximum economic benefit?

canberratimes.com.au/story/9207957/…

English

@Dale96183744121 @DavidPocock Could you show me some actual ROI from previous like for likes? (Multiple examples should smooth the sample size).

English

@DeltaandFlow @DavidPocock These things tend to give an ROI. More artists would perform here. More jobs. More hotel room bookings. The flow on effect is real and would have a positive impact.

English

Great farm tour yesterday.Awesome land development and grass production coupled with the latest tech in feeding and finishing. Nice to see our genetics matching into this environment and system well. #paradooprime #autofeeders #remotemonitoring #batchingplant

English

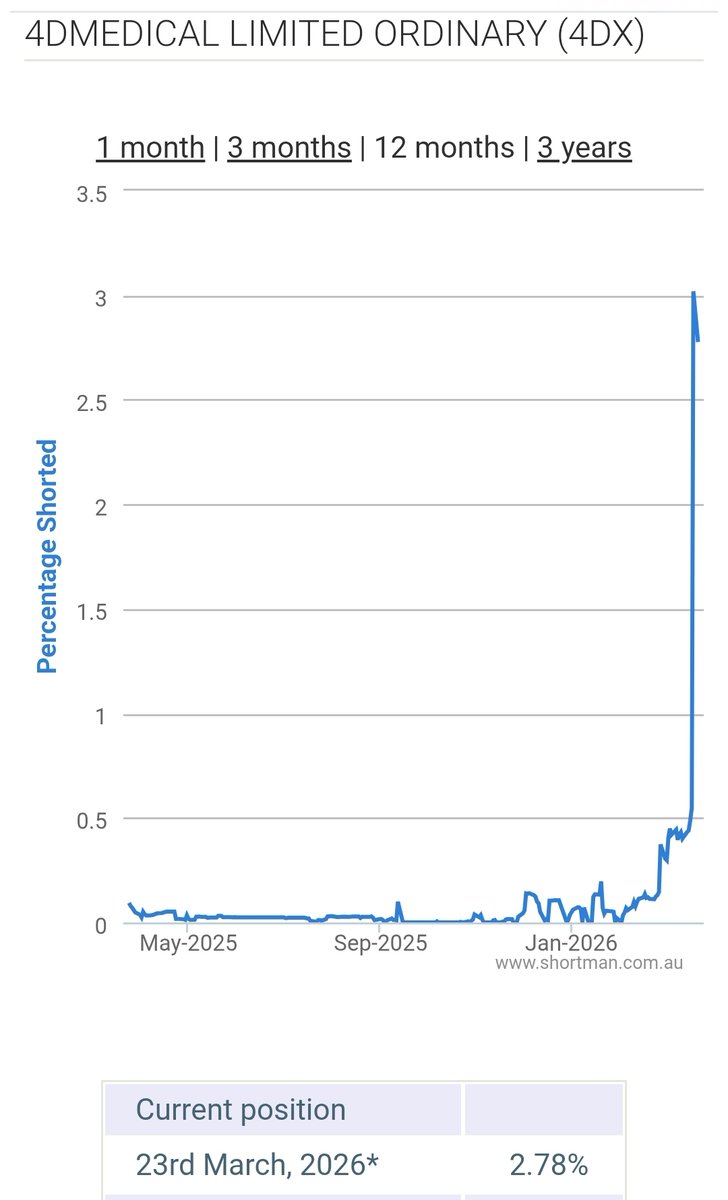

$4DX.AX : Short Candidate

x.com/toy59496/statu…

I am not alone thinking this is a candidate for a short, look at that spike!!

Robin Dods@toy59496

$4DX.AX : Analysis & Valuation x.com/toy59496/statu… I've reviewed this company as I was concerned I got it wrong 6 months ago. Looking at it now I did get it wrong, and I didn't... I misunderstood that it is not intended as a substitute for a CTPA or VQ scan but rather additional interpretation from the millions of CT scans that are done every year in any event. It is the first to market with this technology, which is an advantage. On the other hand I was rightly cynical about the technology in that clinical validation is based on just 16 patients. I view it as grossly overvalued at the moment. But remember I was wrong 6 months ago... Briefly 1. $3.5B market cap on $5.85M revenue. ~600x P/S. 2. The 27x surge from $0.24 to $6.50 due to Philips distribution deal (US10M minimum), and 6 elite US hospitals in 7 months -Stanford, Cleveland Clinic, UCSD, Miami, UChicago, and now Mayo Clinic. 3. The valuation is extreme by any standard: a) Trades at 12x the multiple of Pro Medicus, the most expensive medical imaging SaaS on earth, b) 38% above Bell Potter's A$4.50 target (who ran the $150M capital raise - conflicted) - 150% above Jefferies' $2.50 target, c) Ord Minnett independently downgraded to SELL in Feb 2026 4. Key risks the market is ignoring: a) Reimbursement runs on a temporary Category III CPT code (5yr lifespan), b) Mayo deployment is a 90-day trial, explicitly "not financially material", c) Clinical validation based on just 16 patients, no large independent outcome studies, d) H1 FY26 revenue just $2.9M while net loss widened to $154M, e) FDA 510(k) pathway is "substantial equivalence" - not rigorous efficacy proof. 5. The technology is legitimate. FDA cleared, Medicare reimbursed, adopted by America's best hospitals. The addressable market (1M+ VQ scans/year, US$1.1B) is real. But at ~600x trailing revenue and ~86x FY27 consensus, the stock prices in near-flawless execution for years. 6. Analyst fair value range: A$2.50-$4.50. Current price: A6.23. Not financial advice. DYOR.

English

@Bradmac120970 @markgardn Decimate the middle & aspirational class. K-shaped economy incoming.

English

@markgardn Better off in this country with nothing, Mark. A welfare state paid for by us idiots…

English

Australia is a poster child of political shambles...

48.5c in the dollar, pay for your own healthcare, your own retirement, your own education, 10% GST, 30% fuel tax.....

Houses are the most expensive in the world, we are a net exporter of coal, uranium, LNG and have expensive electricity

Remind me what we get for our 47-48c in the dollar?

@AlboMP

English

@markgardn @vinksta87 We live in hope. It's the can't be any worse option. Idk maybe they just point the bureaucrats & public service in the right direction. IDK

English

@vinksta87 We are going to pull an America and elect Pauline 🤣 then regret it... who knows from there

English

Depends on who you are.... if you are a boomer - killing it, family money -killing it, worked out how to scam NDIS - killing it, foreign owned mining or gas company -killing it, multinational software business - killing it

Average family with 2 parents on good income -F%&cked

Anyone under 30 - F%$ked

English

English

@AusPoll6 @samstrades Amusingly renters back ALP & Greens despite both those parties being all ahead full on migration which is what makes renting so expensive.

English

JS retweetledi

As an engineer working in the energy sector here is how I would solve our energy crisis:

Cancel net zero, what Australia does in this space is pointless.

Given our isolation have one year's storage of petroleum products.

Build an energy sector that utilises all of our bountiful resources, such as gas, coal, nuclear and some renewables (rooftop solar, geothermal, hydro)

Prioritise energy security and cost to consumer.

Build refinery capacity to meet our local needs. The refineries should be flexible to support different oil crudes.

For energy exports follow the Qatar model, local use first then export to drive down costs.

Drill baby drill and consider technology such as Gas to Liquids and biodiesel to shore up our oil reserves.

Produce all of our own fertiliser and adblue locally. The gulf crisis has shown the folly of our current approach.

Whatever the question is Hydrogen is not the answer.

@PaulineHansonOz #auspol

English

@Mistadamage All I know - Is that someone needs get their sh#t together - really don't care what their ilk or what they call themselves. But atm and recent past not good.

English

Before my Lib mates take offence and my ON mates take offence, take a step back and a deep breath and read the real message here:

As long as the right parties attack each other, Labor gets to do a Bradbury.

Divide and conquer is Labors modern manifesto. And the right walks into their trap every time!

There is one thing only we (the centre right) need to learn from Labor: ITS TIME TO GET OUR SH$T TOGETHER!

Mic Fels 🇦🇺@Mistadamage

Paul Kelly has a sobering thought for One Nation voters: a vote for One Nation is effectively a vote for Labor

English

@OldmateW @Mistadamage This city / country divide. It mainly comes from country folk & farmers (I'm country). City people have been getting screwed probs worse & will continue to get so - via inflation, housing costs, rental vacancy, excessive immigration & soon to be higher unemployment.

English

@DeltaandFlow @Mistadamage Absolutely, that is what will occur, I was pointing out the reality that the city/country divide is very evident and real and how things are today does not help due the mechanics of the money flow from Ag, we are not in a good place,🤔👍

English

If you were wondering why directing diesel to regional Australia is in the national interest:

All the operations behind the astounding productivity growth in ag - are the things that have stopped with the parked up tractors right now.

English

@OldmateW @Mistadamage Govt doesn't care for local communities - This will not factor into whether farmers receive support. I think will be more based on votes, actual need v other industries, voter perception, potential economics v other industries, lobbying, requirement - food surplus etc.

English

@DeltaandFlow @Mistadamage Big picture, the regions towns are dying compared to 100 years ago, what is different?? it is where the spent money goes, today it immediately goes offshore, compared to being spent locally or even in the same state historically to cause the 'money velocity' circular economy,🤔👍

English

@OldmateW @Mistadamage What do you mean? As in their input costs are mostly imports ? Or farmers spend selectively locally only - which at times may be a fair comment..

English

@Mistadamage Yes, absolutely, BUT there is a fly in the ointment, the the money velocity circular economy around Ag has collapsed, ie, most of the gross profit money goes off shore immediately, the percentage that remains to foster the local economy is VERY low by proportion,🤔👍

English

@burgess_ag It's a tough gig. Your not alone. There is a change in world dynamic at play. Most across society are likely getting royally fxcked. You have your land & a farm. Batton down as unless sig debt you are better position than most. You can always liquidate if need be.

English

Fuck tell you what.. this is where farming solo and living by yourself sux. Heads pounding with change of things business wise several times daily, and no one to just stop and chew the fat over it with. Think we are in for 1 hell of a ride this time round.

English