Karel Mercx@KarelMercx

Three charts explain why the silver rally is not over.

All three charts use a 100-day moving average. The goal is simple: remove noise and focus on the signal.

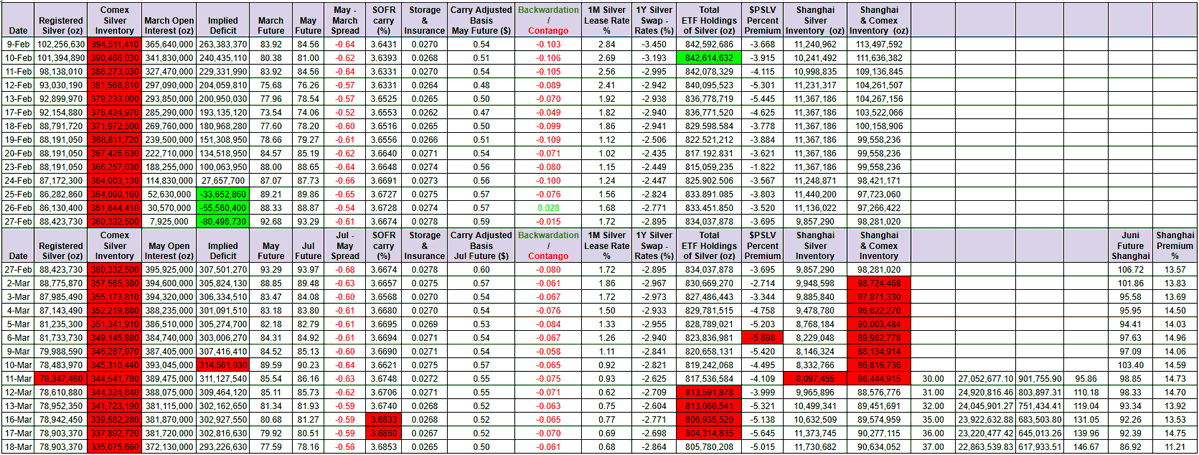

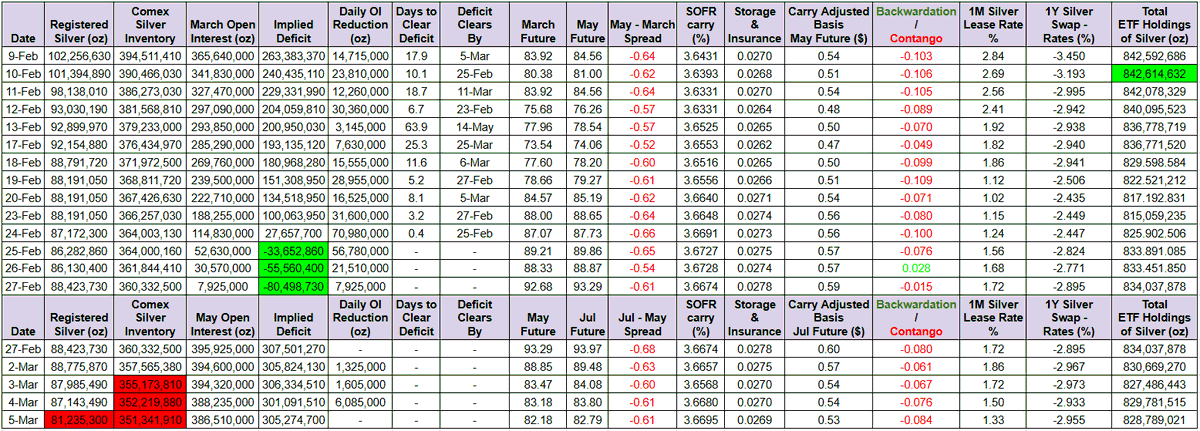

The first chart shows the 1-month silver lease rate. In a balanced market, this should sit around 0%, which is marked by the red line. Instead, the 100-day average is currently 6.28%, already an extreme level. Even more telling, the latest reading is 8.53%, which means the average itself is still rising. This reflects how limited the availability of physical silver has become. High and rising lease rates are a classic signal of physical market stress.

The second chart shows the 1-year silver swap, adjusted for the US interest rate. This adjustment matters because cash is paid today while silver is delivered one year later, allowing the seller to earn interest in the meantime. After adjusting for that, this number should be positive for two reasons. Silver must be stored and insured for a year, which is not free, and if the swap were negative, arbitrage would normally eliminate it by buying physical silver today and selling it forward. The fact that the 100-day average is roughly 4 percentage points below zero, and that the latest reading was about −7.9%, shows how severe the shortage of physical silver really is. The downtrend in the 100-day average confirms that stress is increasing.

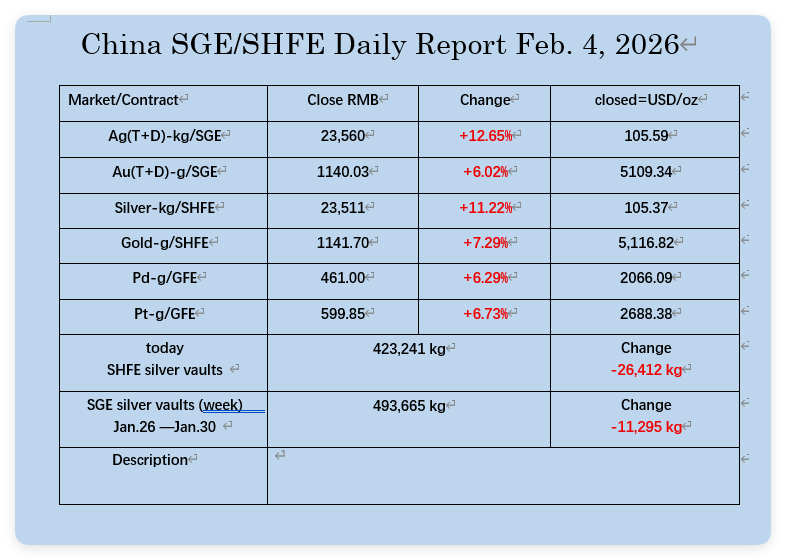

The third chart shows the Shanghai silver premium. In normal conditions, this should hover around 0%. Since 2023 it has been structurally higher, with a peak reached in 2024. The sharp rally in Western silver prices temporarily compressed the premium to just over 1%, but it has since started rising again. Just before Christmas, the premium briefly reached 12%, the highest level on record. While the spot premium has not exceeded that peak since, the 100-day moving average has continued to rise. This highlights persistent physical demand in the East.

If we zoom out, all three indicators are now above their 100-day moving averages. Taken together, they tell the same story. The silver market still requires meaningfully higher prices to bring supply and demand back into balance.